Chief Researcher

• インサイト

Rethinking US exceptionalism: A case for diversification

For years, one dominant theme has been rewarded: back the US, and tune out the rest. For some investors, that positioning was not even a deliberate choice. It crept in gradually, driven by relative returns, benchmark evolution and the quiet compounding effect of flows toward whatever was working. Today, that assumption deserves a closer look.

執筆者

Strategist

まとめ

- US exceptionalism is no longer a given

- Broad, attractively valued opportunity set is hiding in plain sight

- Combining diversification with alpha generation can aid portfolio resilience

This is not a case against the US, which remains the world’s deepest capital market, the anchor of global liquidity and a genuine leader in innovation. But it is a case for asking a more nuanced question: is the persistence of US exceptionalism still something investors can rely on?

Markets are often interpreted through a cyclical lens: inflation, rates, growth. But today’s shift looks less like a normal cyclical turn and more like a structural transition. For decades, global markets operated around one reserve currency, one primary innovation hub and one main destination for global capital. The US occupied that role exceptionally well. That system is not collapsing, but it is evolving.

The objective is not to reduce US exposure. It is to reduce reliance on a single source of returns

Economic activity, innovation capacity and human capital are gradually dispersing across geographies. Capital flows are adjusting at the margin. At the same time, US-specific risks around trade policy, fiscal sustainability and geopolitical posture have re-entered the conversation in a way they largely had not for years. For much of the past 15 years, political and macro risk were associated mainly with Europe and emerging markets. Increasingly, that assumption is being tested.

Non-US assets may only need a less dominant US

This does not mean the US needs to weaken structurally for non-US assets to perform better. They may only need a less dominant US. Real disposable income growth has slowed in a sticky inflation environment, while elevated fiscal deficits, a rising Treasury interest burden and historically high US profit margins imply a less forgiving backdrop for valuations.

The risk of narrow leadership

Another defining feature of recent years has been how narrow equity market leadership has become. A small group of US mega-cap companies, concentrated largely in technology and AI, has driven a disproportionate share of global returns. Strong earnings, rising valuations and index reweighting created a self-reinforcing cycle: performance attracted flows, flows supported market caps, and rising market caps increased concentration.

On closer inspection, then, US exceptionalism has increasingly become narrow exceptionalism. That matters because portfolios built around this concentration may be more fragile than they appear. History is consistent on one point: equity leadership rotates.

The opportunity hiding in plain sight

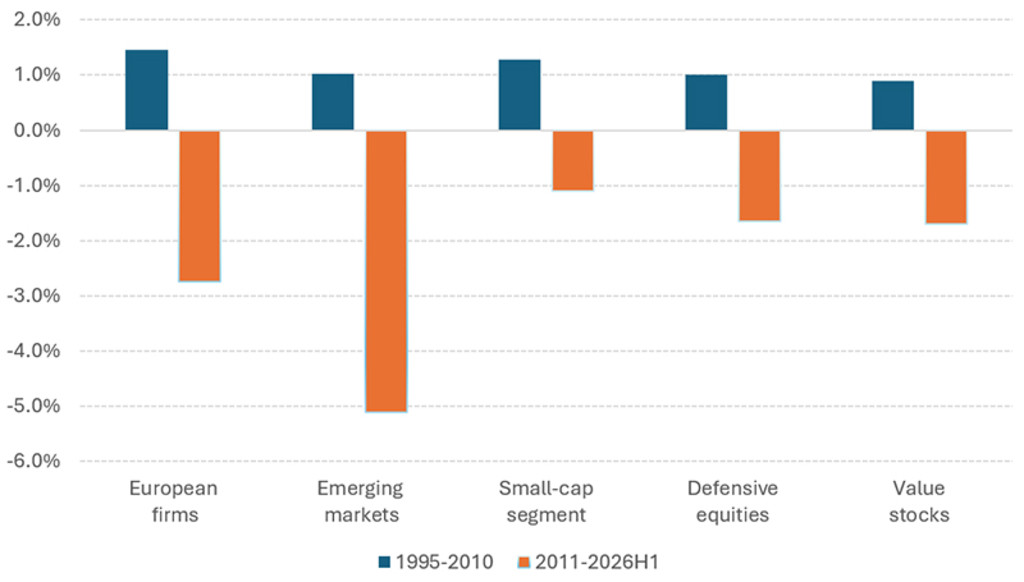

Beyond US large-cap growth lies a wide set of equity segments that have been overlooked, and in some cases actively avoided, for much of the past 15 years. These include European equities, emerging markets, small caps, defensive equities and value stocks. Each has materially underperformed global markets over the recent period. But that underperformance is precisely why allocations have declined, and why the opportunity may now be hiding in plain sight.

A longer history shows a different picture. In the 16 years before the recent US-led stretch, these segments generated significant outperformance, not simultaneously, but at different times and in different market environments.

Figure 1 – Relative performance versus MSCI ACWI, from January 1995 to June 2026

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: LSEG, MSCI, Robeco. For the global market we use the MSCI All Country World Investable Market Index (ACWI IMI), while for the contrarian alternatives we consider the MSCI Europe Index for European firms, MSCI Emerging Markets Index for emerging markets, MSCI All Country Small Cap Index for the small-cap segment, MSCI World Minimum Volatility Index for defensive equities, and MSCI All Country World Investable Value Index for value stocks. Data is available from January 1995 to June 2026. All returns are based on total returns and denominated in US dollars.

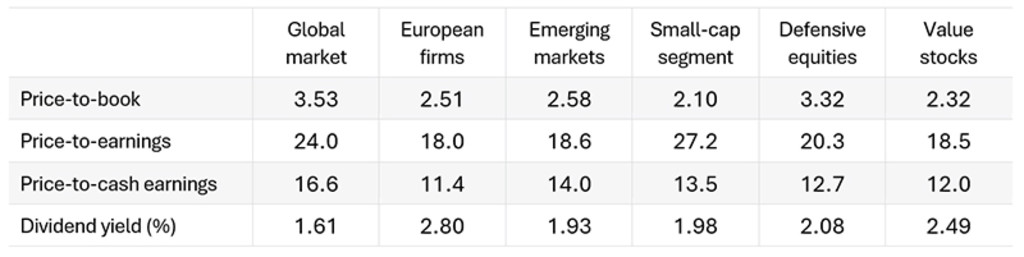

Today, they also share another feature: each trades at a meaningful valuation discount to the broader market across measures such as price-to-book, price-to-earnings, price-to-cash earnings and dividend yield.

Table 1 – Valuations as at 30 June 2026

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: LSEG, MSCI, Robeco. For the global market we use the MSCI All Country World Investable Market Index (ACWI IMI), while for the contrarian alternatives we consider the MSCI Europe Index for European firms, MSCI Emerging Markets Index for emerging markets, MSCI All Country Small Cap Index for the small-cap segment, MSCI World Minimum Volatility Index for defensive equities, and MSCI All Country World Investable Value Index for value stocks. Data is available from January 1995 to June 2026.

Five segments, five different return drivers

Crucially, this is not a single trade or one unified macro bet. Recent performance illustrates the point: emerging markets have delivered strong returns, while several of the other segments have not, showing that they do not move together or depend on the same conditions. Europe, emerging markets, small caps, defensive equities and value stocks each have different return drivers:

Europe may benefit from fiscal-driven recovery and risk-premium compression.

Emerging markets may benefit from global manufacturing strength and weaker-dollar tailwinds.

Small caps tend to respond to falling financing costs and domestic demand.

Defensive equities can provide resilience in risk-off environments.

Value stocks may benefit when higher rates put pressure on growth-stock multiples.

That is the essence of diversification. The question is not which segment will outperform next. In practice, that is extremely difficult to forecast. The point is that different market regimes reward different parts of the market, and the timing of those transitions is inherently uncertain. The real risk is being unexposed when leadership changes.

Diversification needs discipline

Diversification alone, however, is necessary but not sufficient. It expands the opportunity set, but it does not guarantee better outcomes. Implementation matters. In uncertain environments, investors often become pro-cyclical: chasing recent winners, exiting underperformers and rotating too late. The segments that offer the greatest diversification benefit are often the hardest to hold through periods of underperformance.

This is where quantitative investing can help. A disciplined, rules-based process can reduce the behavioral biases that undermine long-term returns. Rather than relying on market timing or short-term conviction, a systematic approach applies the same investment discipline across regions, styles and market segments. It helps investors stay exposed to a broader opportunity set, even when recent performance makes that uncomfortable.

Robeco’s quant approach is built around decades of research into empirically proven return drivers, such as value, quality, momentum, analyst revisions and short-term signals. These factors have been enhanced over time and are combined within a consistent portfolio construction framework that seeks to balance return potential, risk control and diversification.

Robeco’s range of quantitative strategies

Enhanced indexing strategies are designed as smart alternatives to passive, seeking consistent excess returns while staying relatively close to the benchmark. Active quant strategies target higher alpha within a controlled risk framework, making them suitable for investors looking to augment portfolio returns. Defensive, or conservative, strategies focus on lower-risk equity exposure and aim to improve the return path by reducing drawdowns. Value strategies provide more targeted access to a specific long-term return premium, while next-gen small-cap strategies use advanced data, refined signals and machine learning techniques to capture alpha in a broad, less efficiently researched part of the market.

Building portfolios for a less certain world

If markets are transitioning from a concentrated regime toward a more dispersed one, portfolios need to reflect that shift. The objective is not to reduce US exposure. It is to reduce reliance on a single source of returns. In a world where exceptionalism is no longer a given, resilience becomes the defining edge. And resilience is built not by predicting where leadership will emerge next, but by diversifying thoughtfully and implementing with discipline.

Investing beyond the US

Opportunities in global equities, emerging markets and Europe

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会