Strategist

• インサイト

Why investors are now diversifying beyond the US

For much of the past 15 years, global investing felt deceptively simple: stay overweight US equities, especially large-cap growth stocks, and you’ll be rewarded handsomely with above historical average returns. The longer the cycle ran, the more that positioning became embedded, not always as a deliberate call, but through benchmark drift and the compounding effect of flows into what kept working.

まとめ

- US reliance risky as valuations and uncertainty rise

- Narrow tech-led gains heighten concentration risk

- Diversification boosts resilience across assets

Today, the question is not whether the US remains a critical market. It does: it is still the world’s deepest capital market, an anchor of global liquidity, and a genuine leader in innovation and the race towards artificial general intelligence. With a market capitalization of 72%, the US equity market is difficult to avoid.

However, with US economic policies losing transparency and AI-related capex surging, the more practical question is whether US exceptionalism is still reliable and whether portfolios have become too dependent on a narrow and increasingly demanding source of returns: US equity performance and its underlying superior earnings delivery.

詳細はこちら

From observation to assumption: Why the regime is being tested

A key risk of long periods of leadership is that a performance observation turns into a portfolio assumption. Therefore, reference bias abounds.

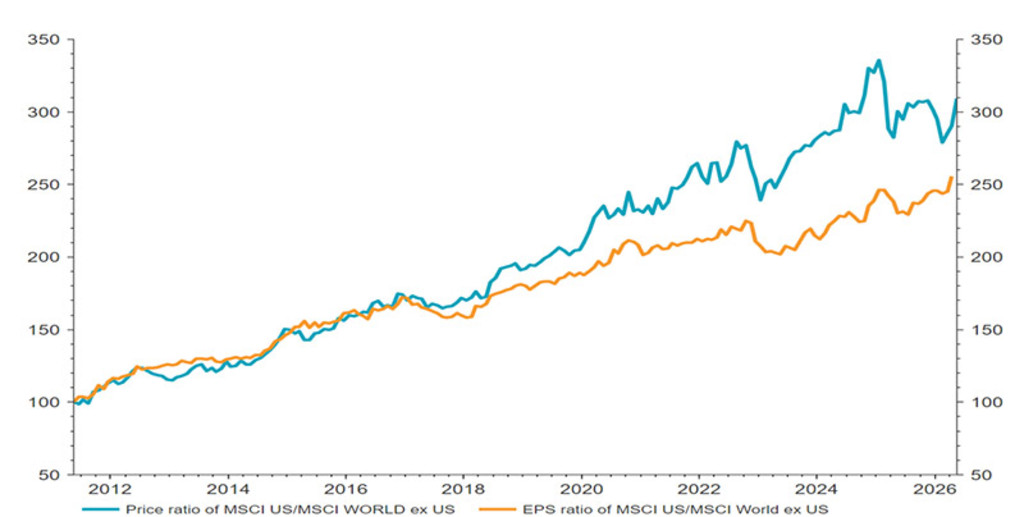

The debate is shifting from ‘can US exceptionalism continue?’ to ‘how much of that is already priced in and how much must still go right to justify it, especially in terms the AI capex boom’s ability to generate an adequate payoff?’ Investors have been increasingly willing to pay up to get access to superior US earnings delivery over the past 15 years, as evidenced by the relative price performance of US stocks outpacing underlying relative EPS growth.

Figure 1: Willing to pay up

Over the past decade, US relative price performance has outpaced its superior earnings delivery

Source: LSEG Datastream, Robeco, May 2026

In our view, the durability of continued US equity outperformance increasingly rests on a narrow set of demanding conditions:

Continued productivity acceleration

Benign disinflation, keeping policy rates low enough to offset elevated fiscal deficits, and

Sustained global capital preference for holding US assets despite rising US policy turbulence (i.e. the ‘exorbitant privilege’ holds).

In our view, the probability that all three conditions will be met is 60-70%, leaving significant tail risk.

Next to these structural macro risks, we pointed out in our Expected Returns 2025-2029 that the strong US equity market performance has increased valuation levels, leaving higher drawdown risk even as we might be in a ‘buzzing’ type of bubble that has further to run. For any calendar year, the statistical average stock market return of 7% is rarely observed, and for the US specifically, significant melt-up as well as downside risk co-exist at this juncture.

With fatter tails in the expected returns distribution for US assets in scope, diversification shifts from a theoretical virtue to a practical portfolio decision.

A structural shift in risk perception (and that matters for relative returns)

Markets are often interpreted through a cyclical lens. Growth, inflation, and rate paths are what matters. Yet, the current backdrop looks increasingly like a structural transition that could change risk premiums. In many countries, starting with the US, security risks (e.g. supply chains, and chokepoints of critical imports and exports) have come into focus, squeezing room for laissez-faire capitalism, with capital flows adjusting at the margin. US trade policy, fiscal sustainability and geopolitical posture have re-entered the conversation in ways they largely hadn’t for years.

Importantly, elevated economic policy uncertainty in the US relative to the rest of world (RoW) does not point to a structurally weak US economy. Still, the resulting higher macro-economic volatility may warrant an adjustment in US risk premiums (we already have seen a rise in the US Treasury term premium since 2021). Investors looking beyond the US starts may see a re-rating of RoW valuations versus a still expensive US market, even as Magnificent Seven stocks have derated recently.

Even if the US stays dominant in the global economic landscape, the question remains whether the market is correctly discounting the cyclical story. We find that the S&P 500 CAPE Ratio is already discounting a 2.9% real GDP growth over the next five years, almost 1% above long-run trend growth and some 50 bps above our five-year growth forecast for the US economy. This suggests that embedded expectations in US stock prices are hard to meet. In this environment diversification becomes less about ‘calling the top’ and more about improving portfolio resilience by recognizing downside risk and broadening the opportunity set.

Concentration risk: US leadership has become narrow

Another feature of this cycle is how narrow leadership has been: a small cluster of mega-cap US tech and AI-linked names drove a disproportionate share of returns, reinforced by index mechanics and passive flows. This creates fragility. If ‘US exceptionalism’ increasingly means ‘narrow exceptionalism,’ portfolios built around that concentration can be more vulnerable than they appear. Investors have been disproportionately willing to pay up for strong US earnings delivery. That premium could collapse if the AI leadership were to be challenged at some point. History offers plenty of reminders that dominant leadership rarely remains uncontested: Standard Oil looked magnificent until antitrust broke it up in 1911, while the dissolution of Northern Securities in 1904 showed even the most powerful industrial-financial combinations could be forced apart. History is consistent: leadership rotates; it’s not a matter of if, but when.

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

The bubble question: Why ‘buzzing’ can differ from ‘bursting’

Any discussion about reallocating away from the US runs straight into a legitimate concern: are we simply replacing a strong momentum trade with another cheaper alternative that lacks momentum to unlock its value?

First, diversification should be a portfolio risk management exercise, not an anti-momentum trade. As we highlighted in our Expected Returns 2025-2029 special topic on the history of bubbles, the US could be in a buzzing bubble where high valuations may be largely justified because investors correctly anticipate extraordinary growth linked to a paradigm shift in the real economy. Historically, around half of bubbles did not burst. The AI bubble could be of the buzzing type as well. Instead of being underweight momentum as a factor, portfolios should avoid being over-dependent on a narrow set of expensive winners.

Second, we see signs of improving momentum in cheap equity segments that were overlooked for much of the past 15 years, notably emerging markets, small caps, defensive equities and value. Crucially, these are not one unified macro bet. They are a collection of distinct opportunities with different return drivers – exactly what diversification should look like. Importantly, collective re-allocations away from the US do not need to be large in order to have a huge positive return effect on smaller markets. Gold, and more recently the Korean equity market, are examples of this phenomenon.

Diversification is not just an equity story

Multi-asset portfolios diversify through rates, credit, and commodities as well. In the weeks following ‘Liberation Day’ on 2 April 2025, the correlation between equity and US long-term Treasury bond returns turned from negative to positive. Meanwhile, the correlation between US long-term Treasury bond returns and gold turned negative. While historically seen as a reliable store of value, recent events have highlighted vulnerabilities, particularly in long-term US Treasuries.

In some cases, yields on US investment grade corporate bonds have dropped below comparable US Treasury yields. Investors who are not able to predict the nature of the next crisis may need to take a diversified approach toward safe-haven assets. Since US Treasuries have gone from safe haven to stormy waters, German Bunds, defensive equities, gold, commodities, fiat currencies and even credit may offer better protection during the next episode of market turbulence. Yet, for a euro investor, hedged US Treasuries still offer attractive value in the medium term. For Japanese government bond investors, the case is more clear cut to stay at home.

Keep US equities, just think harder about FX

In conclusion, the US can remain an important allocation while investors broaden exposures to a wider, attractively valued global opportunity set. Doing so in a disciplined way, rather than trying to time leadership changes, could pay off.

While keeping exposure, a euro-based investor reducing their reliance on the US may need to review the currency decision. From the perspective of a risk-neutral investor without an active view on EUR/USD, we find that the ‘optimal’ equity hedge under current correlations and risk estimates is around 30%. The risk to the dollar is not displacement by rivals or its ability to act as safe haven during international crises but erosion from within through fiscal dominance, reduced hedging properties of Treasuries, and declining scarcity of safe assets.

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会