The Investment Engineers

• インサイト

新興国市場における投資機会

過去1年の間に、大手機関投資家の間では資産配分見直しの動きが見られ始め、長期投資家にとって新興国資産の魅力が一段と高まっています。

執筆者

Robeco

まとめ

- 新興国市場は、世界の経済成長の要

- 新興国株式は、依然としてグローバル市場に対して割安

- 新興国債券は、堅調なマクロ環境を背景に魅力的な利回りを提供

10年以上に渡り米国株式がアウトパフォームし続けましたが、投資資金は、より広範な投資機会へ向かいつつあります。これは米国への信認が失われたためではなく、他地域における投資機会の魅力度が高まっていることが背景です。バリュエーション格差の拡大や集中リスクの高まり、市場を現在けん引している銘柄の持続性に対する不透明感を背景に、投資家は一部の主力銘柄以外の投資機会へ目を向け始めています。

グローバル市場ではリターンの源泉が一段と多様化しており、政策、経済構造、セクター構成の違いにより、パフォーマンス格差が拡大しています。このような環境下では、市場のけん引役を予測することは難しくばらつきが拡大します。また、AI投資の資金調達や産業構造に対する影響の不確実性も高まる中、広範な投資ユニバースへのアクセスが一層重要になっています。

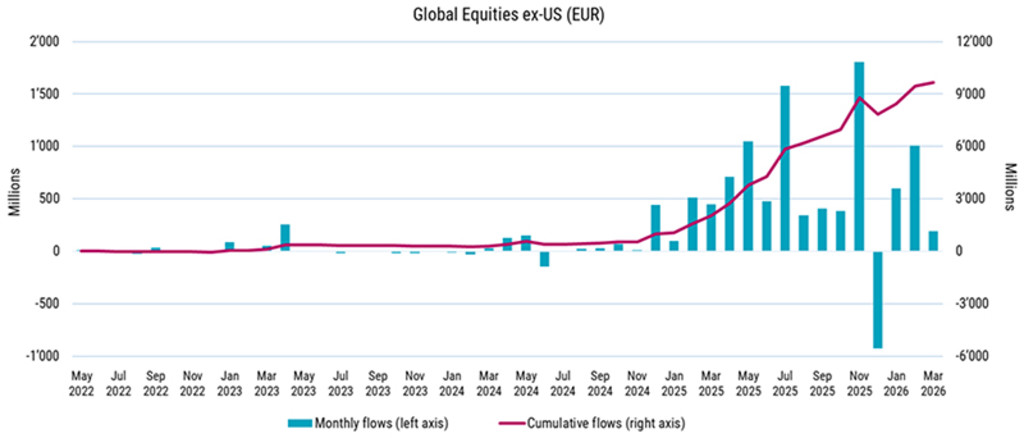

図1:株式資金は米国から世界全域へ

出所:Broadridge、ロベコ、2026年5月

さらに、米国系資産運用会社の存在感が高まることで、グローバルな資本配分の大部分が米国を拠点とする機関投資家の影響を受ける状況となってきています。これにより、自国(米国)偏重や資金の集中が助長され、他地域の投資機会が見過ごされる可能性が高まっています。1 同時に、新興国市場はグローバルな成長、イノベーション、富の創出の中心的な役割を担うようになり、世界経済の構造も変化しつつあります。本稿では、こうしたグローバル環境の大きな変化を捉えるロベコの新興国市場戦略をご紹介します。

ロベコ・エマージング・マーケット株式戦略

米国以外への分散投資を検討する投資家にとって、新興国市場は割安なバリュエーションと多様な成長要因を提供します。多くの場合、新興国企業のバランスシートやキャッシュフロー特性は先進国市場に近づいているにもかかわらず、依然として新興国特有の株式リスクプレミアムを享受できます。ロベコの新興国株式チームは、新興国は先進国と比較して長期的に優れた投資機会を提供すると考えます。

図2:新興国株式には長期的にアウトパフォームする局面が存在

過去の運用実績は将来の成果を保証するものではありません。投資の価値は変動する可能性があります。

出所:MSCI。数値はすべてユーロ建て。データは2025年12月末時点。比率は、MSCIエマージング・マーケット指数をMSCIワールド指数(米ドル建て)で除して算出。比率の上昇は新興国市場、低下は先進国市場のアウトパフォーマンスを示す。表示通貨と投資家の居住国通貨が異なる場合、居住国通貨に換算したパフォーマンスは為替変動による影響を受ける可能性があります。1年未満の期間は年率換算していません。運用報酬控除前、GAVベースのリターン。パフォーマンスデータには、投資口の発行・解約に際して発生する手数料やコストは考慮されていません。これらは、記載のリターンにマイナスの影響を与えます。

ロベコは、確信度の高いエマージング・スターズ株式戦略に加え、単一国戦略や中国を除く戦略など、幅広い新興国株式ソリューションを提供しています。

ロベコの新興国ファンダメンタル運用チームは、厳選した銘柄選択と地域に根差した知見を駆使し、この複雑な投資ユニバースの中から長期的な投資機会を発掘します。ロベコの規律ある投資プロセスはトップダウンによる国別選択から始まり、「将来性を伴うバリュー」にフォーカスします。これにより、「投資家はクオリティの高いグロースとみなされる銘柄を過大評価しやすい」という、新興国市場特有の市場バイアスから生じる非効率性を捉えます。ファンダメンタルズに基づく銘柄選択分析では、収益見通しが十分に織り込まれていない、バリュエーションが魅力的な企業に注目します。また、過信や群集行動といった市場参加者の行動バイアスを捉えるツールとして、定量モデルをファンダメンタル分析に組み合わせています。

ロベコ新興国クオンツ株式戦略

クオンツ運用の観点では、新興国市場のファクター・プレミアムは強く、持続的である傾向があります。こうした特性がロベコの新興国クオンツ戦略における長期投資の基盤となっています。特にロベコ独自の定義を用いることでこの特徴は一層顕著となり、新興国市場は、規律あるリスク管理に基づくクオンツ戦略にとっては有望な投資対象となります。ロベコでは、QI 新興国3Dアクティブ株式戦略、QI新興国コンサバティブ株式戦略、および新たに運用開始した3D新興国株式ETFなどの戦略があります。

新興国市場は市場間の相関が比較的低く、地域間の自然な分散効果をもたらします。先進国市場が同調的な動きとなる傾向があるのに対し、インド、ブラジル、台湾などの新興国はそれぞれ固有の要因に基づいて異なる動きを示します。ロベコのクオンツ戦略はこの多様性を活かし、大きなマクロ判断に依存するのではなく、小さなティルトを戦略的に積み重ねることで超過収益の機会を創出し、同時にボラティリティの抑制も図ります。

新興国市場は市場間の相関が比較的低く、ロベコのクオンツ戦略はこうした市場のばらつきを活かします。

すべてのポートフォリオは厳格なリスク管理の下、地域分散を図り、機械学習や自然言語処理などデータを駆使した知見を活用しています。これにより、機動的かつコスト効率の高い形で新興国市場のアルファへのエクスポージャーを実現します。

また、ロベコの3D戦略では、独自のフレームワークを用いて、リスクとリターンに加え、サステナビリティを統合しています。ポートフォリオは、市場環境や設定された目標に応じて、これらの要素間の最適なバランスを機動的に追求します。これにより、ESGリスクを管理しつつ、サステナブルな未来への移行をけん引する企業への投資機会を捉え、長期的な投資価値の向上を図ります。一方で、予め特定のサステナビリティ成果を固定するものではありません。

ロベコ新興国債券戦略

新興国市場は、金融包摂の進展、国内の富の拡大、新興国間の域内貿易の深化を背景に、より強靭で競争力のある経済へと進化しています。トレンドとして高い経済成長を背景に、多くの新興国2の信用力は先進国に近づきつつある一方、利回りは依然として相対的に高水準にあることから、分散投資を志向する投資家にとって魅力的な投資機会をもたらしています。

多くの新興国の信用力は先進国に近づきつつあります。

ロベコは、高い確信度に基づくアクティブ運用と独自の綿密なリサーチを組み合わせ、トップダウンのマクロ分析とボトムアップによる国別および通貨別の選択をバランスよく統合しています。ハードカレンシーおよび現地通貨建て双方の商品を提供しています。サステナビリティや移行リスクもフレームワークに完全に組み込まれ、下落リスクの抑制とポートフォリオの強靭性向上に寄与しています。

トップダウンで市場サイクル全体を通じたリスク配分を決定します。また、グローバルな金融環境やリスク環境に加え、新興国ハードカレンシー債券および現地通貨建て債券に固有のバリュエーションやテクニカル要因を分析します。

これに加えて、ボトムアップの発行体・国別選択では、独自のソブリン・レーティング・モデルを用いて信用力を評価します。このモデルは流動性や支払能力といった主要指標を評価し、信用力の改善・悪化を予測するとともに、極端なケースでは深刻な信用不安やデフォルトの兆候を把握するのに役立ちます。

結論

資産配分の一部を米国から新興国市場へ振り向けることは、グローバルな投資機会の変化を認識することにほかなりません。新興国市場は、高い構造的成長、政策的枠組みの改善、魅力的なバリュエーション、投資家による保有比率の低さという特徴を併せ持ち、他地域では得難い投資機会を提供しています。同時に、リスクに対する理解は進み、過去のサイクルと比較したうえで適切な価格が市場に織り込まれるようになっており、分散とリサーチに基づくアプローチをもってすれば管理可能です。直近の市場動向にとらわれない長期的視野を持つ投資家にとって、米国から新興国市場への資産配分の見直しは、将来を見据えたポートフォリオ構築の現実的な一歩といえるでしょう。

脚注

1 Schoenmaker, D.(2026年) “Risks for Europe of US dominance of global asset management”, ポリシー・ブリーフ 2026年7月, ブリューゲル

2 Emerging markets face Iran shocks with more debt, and less danger - フィナンシャル・タイムズ - 2026年5月15日

今、米国以外へ分散投資すべきでしょうか。

当記事は、米国中心の成長に代わる投資機会を地域別に探る全3回シリーズの1本です。

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会