Equity Analyst

• インサイト

Europe powers up its push for energy security

Europe’s latest energy shock has again exposed its continued fossil import dependence, but will accelerate the structural shift toward electrification with massive grid and infrastructure capex set to drive a decade long investment cycle.

執筆者

主なキーワード

まとめ

- Middle East conflict exposes Europe’s fossil fuel import dependence again

- Urgency boosts giant capex plans to upgrade grids and networks

- Grid equipment suppliers, industrial electrification leaders, regulated networks and gas majors are likely to benefit

The recent Middle East conflict, and the subsequent closure of the Strait of Hormuz, has dramatically underscored Europe's continued vulnerability to fossil fuel import disruptions. While Europe has diversified away from Russian gas since 2022, it remains heavily dependent on global energy corridors, with the current shock leading to price volatility and a renewed energy security push across the continent. To address this, both the EU and national governments are accelerating strategies focusing on electrification and breaking the cycle of dependency. This should lead to higher and faster investments into areas like grid infrastructure, electrifying industrial processes and, as a transition fuel, natural gas. This presents attractive investment opportunities in companies exposed to what is shaping up to be a decade-long investment cycle.

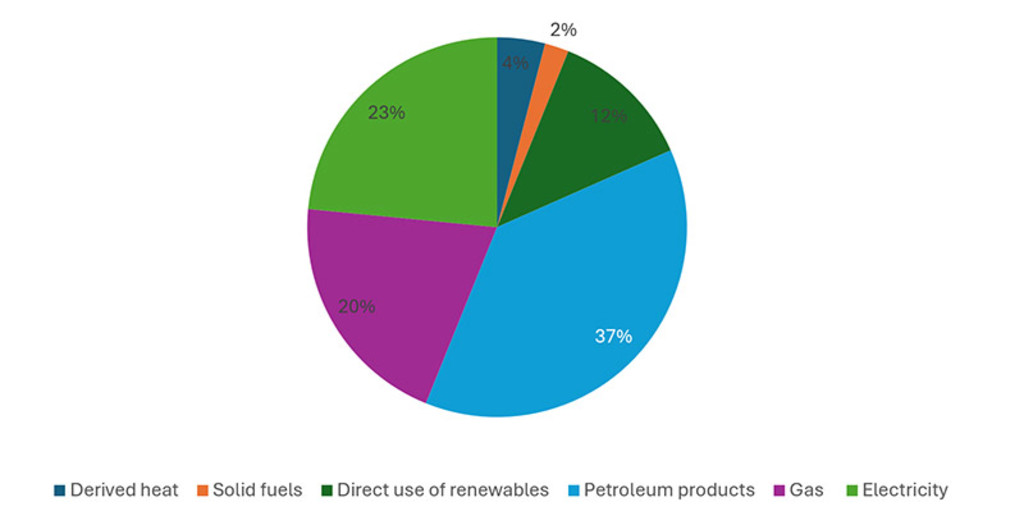

Close to 60% of European energy consumption still comes from fossil fuels (petroleum, gas, coal). Electricity on the other hand, still only accounts for less than a quarter.

Figure 1: Final energy consumption in Europe for 2024

Source: Eurostat - Energy in Europe – 2026 edition

The vast majority (>80%) of fossil fuels are imported from the UK, Norway, US, Middle Eastern and Northern African countries, Russia, Kazakhstan and Azerbaijan.1 As a result, Europe spends between EUR 300-400 bln (approximately 2-3% of GDP) annually on fossil fuel imports. This leaves Europe in a position of significant economic dependence on the countries from which it imports fossil fuels. For example, the Strait of Hormuz crisis is expected to lead to a projected 25% increase in European natural gas prices in 2026, which is likely to weigh on domestic economic output and consumption.2

Network infrastructure requires most investment

To break that dependency, Europe needs to electrify. The European Commission estimates that EUR 660 bln in annual investment will be needed from now to 2030 to reach the continent’s energy transition targets. Roughly half of that needs to go into network expansion. The European Commission estimates that around EUR 584 bln in grid investment is required to accommodate a projected ~60% rise in electricity consumption from 2023 to 2030 and to renew ageing distribution grids (~40% of EU distribution grids are more than 40 years old). The remainder is split between the expansion of renewable power generation (onshore and offshore wind, solar, and battery storage), nuclear (lifetime extensions and new builds), electrified end-use (EV charging, heat pumps, industrial process electrification), and clean fuel infrastructure (hydrogen, biomethane, sustainable aviation fuels). The bottleneck, however, clearly lies in transmission. More than half of the transmission projects required by 2030 are still awaiting permits with roughly 1,700 GW of renewable capacity currently stuck in connection queues across 16 European countries.

Regulatory support is gathering pace

Public funds alone cannot close this gap. EU instruments – the Recovery and Resilience Facility, the Innovation Fund, the European Hydrogen Bank, and member-state budgets – provide an important anchor, but the bulk of the EUR 660 billion will need to come from private investors. To attract private investment, the European Commission has put forward a new action plan ‘AccelerateEU’. The plan’s clear aim is to reduce dependence on fossil fuels and accelerate the transition toward an electric future. For investors, three elements stand out. 3

A binding electrification target to be embedded in the Electrification Action Plan, with the explicit objective of lifting electricity's share of Europe’s final energy consumption from under a quarter today toward levels that displace fossil end-uses in industry, transport and buildings. An ambitious electrification target will set the pace for national policy making and is likely to result in new legislation to accelerate electrification on a local level. Greece, for example, has already passed a law which introduces binding permitting deadlines for renewable energy projects and designates Renewable Energy Acceleration Areas to speed up deployment. 4

Simplifying grid investments: a legislative vehicle to streamline permitting, which currently averages more than five years for cross-border projects, to harmonize cross-border planning, and to mobilize the EUR 584 bln grid investment required.

Concrete deployment commitments: scale battery storage capacity from 55 GW to 200 GW and increase heat pump installations from around 23 mln to 60 mln cumulatively by 2030 (the latter is from the existing REPowerEU framework).

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

We see a decade-long tailwind for electrification

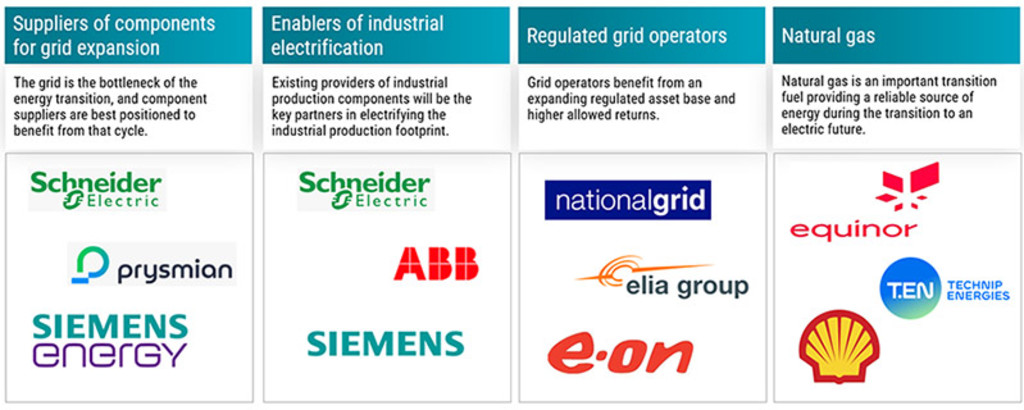

This signals an increasingly favorable regulatory backdrop that we believe represents a decade-long tailwind for electrification. We have identified four key verticals that we think will be the primary beneficiaries of that investment cycle.

Suppliers of components for grid expansion: The most agnostic way to play the theme is to invest in the companies supplying the physical building blocks of the grid, such as transformers, switchgear, cables, protection systems and power electronics. Every incremental gigawatt of solar, offshore wind, nuclear or storage capacity flows through the same hardware, which means equipment suppliers benefit regardless of which generation technology ultimately dominates the mix. With EUR 584 bln of grid investment required by 2030, 40% of European distribution networks close to end-of-life, and electricity consumption set to rise ~60% this decade, it seems safe to assume that demand will remain strong. At the same time capacity remains tight with lead times for large power transformers now exceeding three years. This suggests strong pricing power and full order books at European leaders such as Schneider Electric, Siemens Energy and Prysmian*. The grid is the bottleneck of the energy transition, and its component suppliers seem best positioned to benefit from that cycle.

Enablers of industrial electrification: The electrification of industrial production means swapping gas boilers for industrial heat pumps, combustion processes for electric arc and induction, and standalone factories for microgrid-connected sites. Schneider Electric, Siemens and ABB* are likely beneficiaries. Their portfolios span switchgear, drives, solid-state power electronics, protection systems and the software layer that orchestrates them, and they already serve the installed base they will now be asked to upgrade. The thesis is reinforced by two converging drivers of demand. Reshoring and the EU's industrial competitiveness agenda are driving fresh capex into European manufacturing footprints, while the AI and datacenter build-out pulls the same product catalogue. The result is rare in European industrials: structural top-line growth, pricing discipline supported by tight supply.

Regulated grid operators: As Europe's energy mix shifts structurally toward renewables, capital is migrating from upstream fossil energy to regulated networks. Grid operators like National Grid and E.ON* are therefore a direct beneficiary of the European capex super-cycle. They earn an allowed return on a regulated asset base (RAB) that grows in lockstep with capex, meaning a doubling of investment translates almost mechanically into a doubling of the earnings base. With EUR 584 billion of grid investment required by 2030 and most national regulators having reset allowed returns higher to reflect the new rate environment, unlike renewable developers (which are exposed to power prices, merchant risk and supply chain volatility), regulated grid operators offer contracted, inflation-linked returns underwritten by national regulators.

Natural gas: The transition away from fossil fuels will require natural gas. The latter represents a stable and reliable source of base electricity. Both the Ukraine and Middle East conflicts have however illustrated the need to diversify the sourcing of natural gas. This drives more demand for natural gas globally, which has led to an increase in natural gas supply. As supply of natural gas becomes more fragmented globally, more infrastructure will be needed to distribute that gas globally. Shell and Equinor* are major players in natural gas and both derive roughly half of group earnings from it. Technip Energies* is a leader in energy infrastructure engineering and projects and is positioned to benefit from investments in the space.

Figure 2: An expanding opportunity set

Source: Robeco, June 2026

*These are not buy, sell, or hold recommendations. These companies are shown for illustrative purposes only. Future inclusion of these securities in the strategy is not guaranteed, nor can their future performance be predicted.

Footnotes

1 Where does the EU get its oil from? - The European Council – April 2026

2 Commodity Markets Outlook – World Bank – April 2026

3 AccelerateEU to strengthen EU energy resilience – European Commission – April 2026

4 Law 5299/2026, "Acceleration of the Energy Transition through the Designation of Renewable Energy Acceleration Areas and Other Provisions"

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会