Co-Portfolio Manager

• インサイト

Physical AI and the new energy calculus in manufacturing

Manufacturing is still dominated by fossil fuels, which makes it highly polluting but also exposed to costly and unpredictable energy shocks. Meanwhile, physical AI promises to not only improve output, but also advance electrification, energy-efficiency and the broader energy transition.

執筆者

Equity Analyst

主なキーワード

まとめ

- Factories are the single largest untapped lever for decarbonization

- Physical AI can deliver energy savings of 15-75% in industrial settings

- AI will help harness the energy challenge of robotics and factory automation

For most people, the energy transition conjures images of solar panels, wind turbines, and EVs. While those are effective, they overlook the single largest energy-consuming sector on the planet: industry. The industrial sector accounted for nearly 40% of final global energy demand, the largest share of any end-use sector.1 And though industry is electrifying, it’s not fast enough as global electrification rates have stagnated at around 20% (meaning around 80% of demand is still reliant on fossil fuels).2

Moreover, industry also accounts for the lion’s share of all growth in energy demand (around two-thirds) making it a prime target for efforts to improve energy efficiency.3 In this context, a new generation of technologies, notably physical AI, is emerging as a key enabler that should drive further electrification, energy efficiency and energy security (through reduced fossil-fuel reliance), across industries, particularly industrial manufacturing.

Physical AI marks a step-change for industrial technology, moving AI out of digital environments and into factories, buildings, and power grids. By combining sensing, connectivity, and real-time inference, machines now perceive, decide, and act autonomously in the physical world.

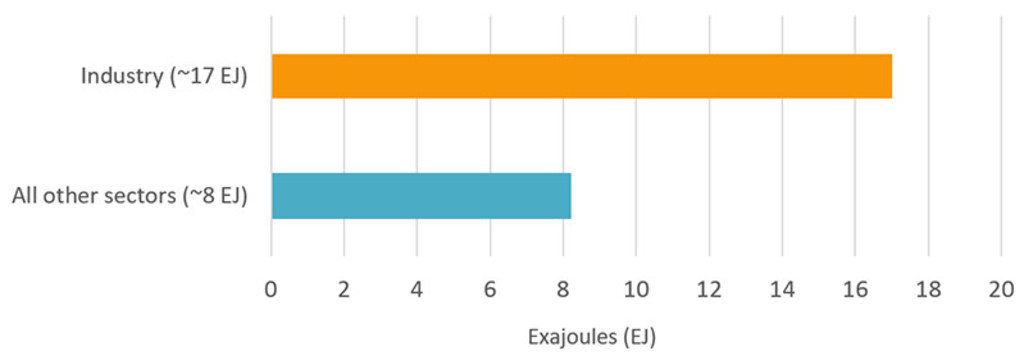

Figure 1 – Industry’s share of growth in new energy demand growth

Source: IEA Energy Efficiency, 2025. Growth in global total final energy demand consumption, 2019-2024 (~25 EJ).

The adoption of physical AI is progressing in three stages. The first, which includes ‘pick-up-and-place' automation, predictive maintenance, and industrial sensing, is already widely deployed. The second, which is being actively piloted, centers on AI-assisted design, advanced process monitoring, and digital twins. The third, at the frontier, involves multi-robot and human collaboration and ‘world-model’ simulations where AI understands physical constraints well enough to manage entire plant environments autonomously (see Figure 2). A mid-single-digit to low-teens share of leading factory automation revenues already includes AI functionality, and AI is embedded in a significant proportion of new product launches.4

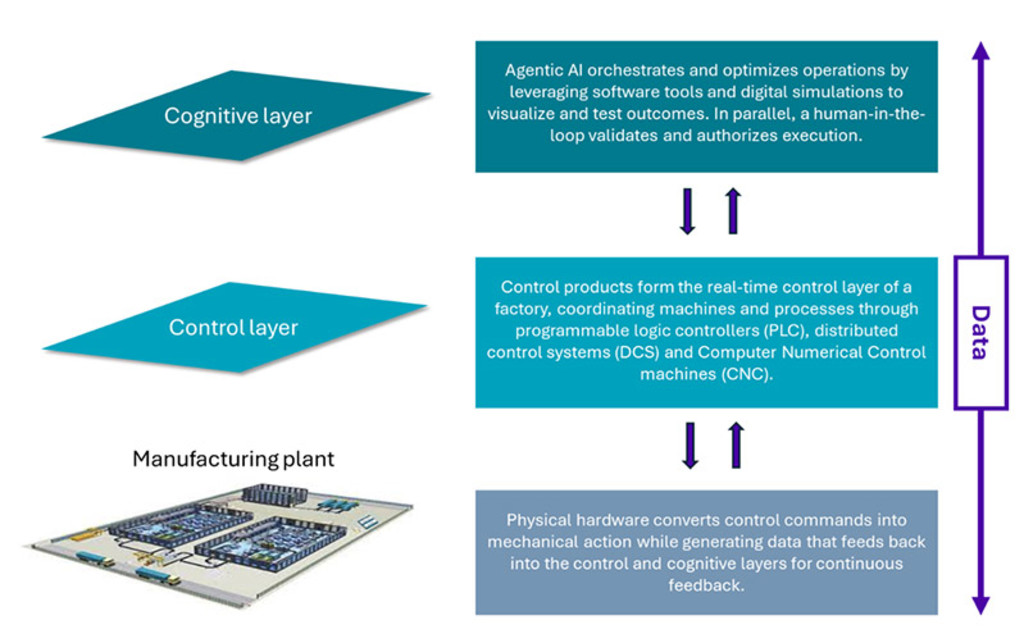

Figure 2 – AI is already being integrated into industrial manufacturing

Source: Siemens, Robeco, 2026. 5

AI use cases – what the industrial leaders are building

Conversations with leading industrial technology companies reveal a race to own the physical AI stack, with energy management as a key priority. For example, Siemens* is positioning itself as the backbone of ‘AI for the real world.’ Its wheeled humanoid robot in a live electronics factory environment achieved high autonomous task success rates in logistics operations such as choosing, transporting, and handling containers.5

The company’s forthcoming ‘Digital Twin Composer’ combines Nvidia’s* Omniverse simulation with real-time engineering data, enabling large-scale industrial metaverse environments where AI agents simulate process changes with physics-level accuracy before any physical modification is made.6 Early pilots have already achieved near-complete design validation and material reductions in capital expenditure.

French industrial giant, Schneider Electric* is also using Nvidia’s GPUs and Omniverse to create digital twins of advanced power systems. These simulated models show the power requirements from the utility grid down to individual chips, enabling precise planning of power distribution and resilience at the facility level.7 Japan’s industrial conglomerate, Hitachi*, already deploys AI agents to diagnose industrial equipment issues with high accuracy and very short response times. In power networks, AI-enabled inspection has significantly improved operational efficiency.8 Nexans*, a French based cable and power transmission specialist, is using AI in a similar way, embedding AI and sensors throughout grid infrastructure to improve failure prediction and real-time power-flow optimization.9

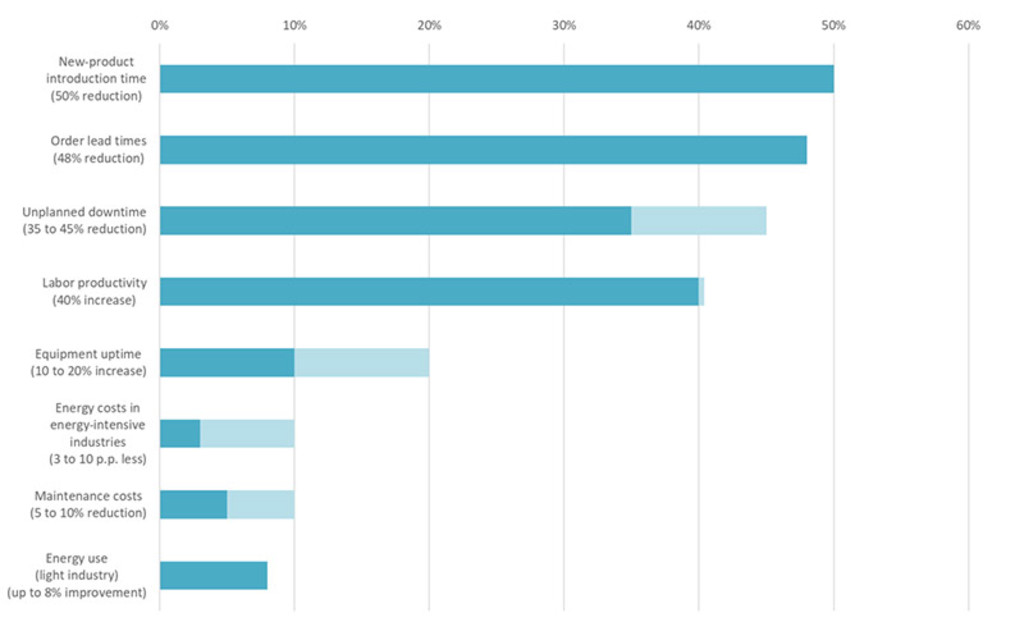

Though these are all different use cases, they all use ‘digital twins’ platforms to generate simulation using real factory data, edge AI embedded into machines and equipment for real-time adaption on the factory floor, and finally, autonomous AI agents that can rapidly synthesize production/processes based on enterprise-wide data. Each AI layer reduces energy and waste and moves manufacturing closer to a net-zero future (see Figure 3).

Figure 3 – The quantified benefits of AI and machine learning in manufacturing

Source: IEA (Energy & AI, 2025), IEA Key Questions on Energy & AI (2026), WEF & McKinsey Global Lighthouse Network (2025-26), US Dept of Energy FEMP, Operational Best Practices, Deloitte Analytics Institute, Predictive Maintenance data (2017).

Energy efficiency in both brains and brawn

If AI enables rapid data processing and inference, the brains, then actuators within robots can be characterized as the brawn. Actuators, which turn energy into movement, are a less discussed but a rapidly emerging dimension of factory energy efficiency. Every industrial robot, every collaborative arm, every humanoid is ultimately an assembly of motion-control systems (e.g., actuators, motors, gearboxes, and drives). The energy performance of those components is rapidly becoming an investment focus.

Electric motors in robotic joints achieve roughly 80% efficiency in isolation, but that figure drops to approximately 40% once gearboxes and transmission systems are factored in.10 Across a global installed base of some 4.3 million industrial robots,11 aggregate energy losses will be substantial. AI-optimized motion planning is a powerful efficiency lever as hardware upgrades. For example, with the help of digital twins linked to Fanuc* industrial robots, engineers reduced energy consumption by 74.8% in pick-and-place operations.12

Humanoids, which can contain dozens of actuators as well as other energy-consuming components, are full-bodied energy challenges. For example, Tesla’s Optimus, Agility Robotics’ Digit, and Apptronik’s Apollo at Mercedes-Benz* – run for only two to four hours per charge, constrained by actuator inefficiencies, heat drain, and batteries with low energy density.13

These reduce the productivity, efficiency and ultimately the economic viability of humanoids in live factory environments. However, the engineering response is accelerating. Next-generation quasi-direct drive (QDD) actuators offer three to five times greater torque-to-weight ratios versus conventional harmonic drives,14 while new magnetic gear technologies and high-efficiency brushless motors are pushing actuator efficiency beyond 90%.15

The companies solving the actuator energy problem – through advanced motor design, power electronics, and AI-driven motion optimization – are building a technology moat at the heart of the next industrial era.

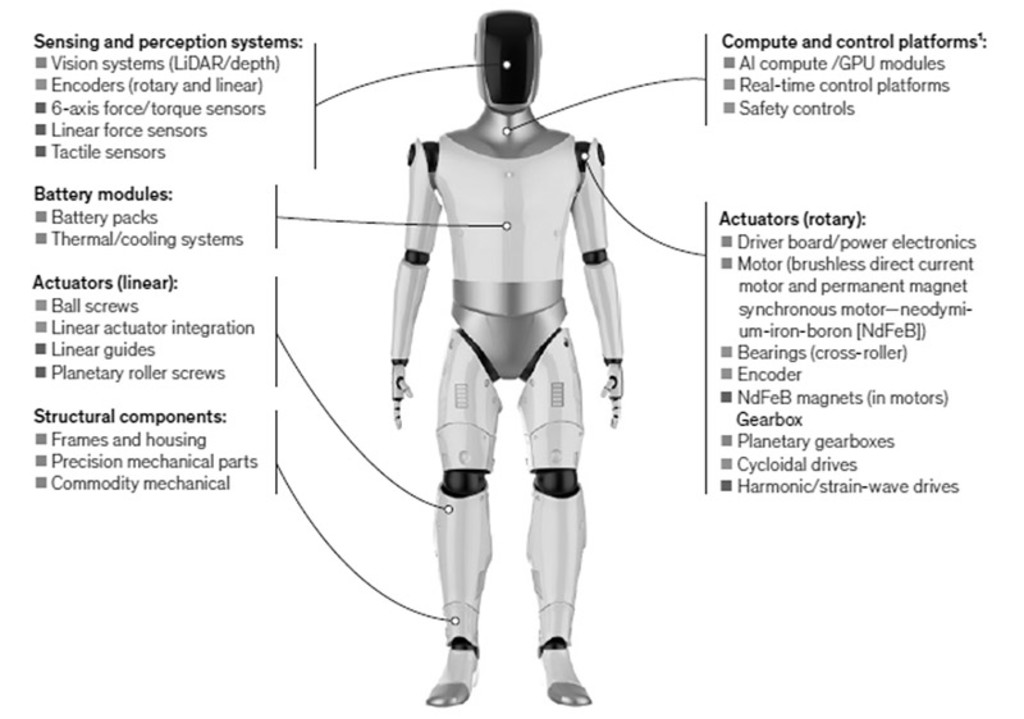

Figure 4 – Actuators form up to 60% of a humanoid’s high-impact components

Source: McKinsey, 2026. Core hardware domains of humanoid robots include actuators (40-60%), sensing and perception systems (10-15%), structural components (5-10%) and battery modules (5-10%).16

The investment imperative

Industry consumes 40% of final energy demand, making it an ideal target for technologies such as physical AI that promise to increase energy efficiency and reduce waste. But it’s not just about adopting AI, the next generation of industrial leaders will be defined by how efficiently they deploy physical AI – combining intelligent ‘brains’ with energy-intensive ‘brawn’.

At the factory level, the ‘brawn’ of physical AI – actuators, motors and robotics systems – are critical drivers of energy demand, reinforcing the need for more efficient industrial processes and motion technologies. As manufacturing electrifies and automation becomes more AI-driven, electricity use is emerging as a core point of competitiveness.

At the same time, the ‘brains’ – semiconductors, AI models and control software – determine how effectively that energy is used, underpinning demand for power-efficient chips, advanced control systems and optimization software. Physical AI systems require high-quality, real-world operational data to optimize performance under real constraints and many incumbents with data and manufacturing platforms are seizing the opportunity, partnering with AI technology leaders to gain a competitive edge.

But AI-driven productivity can also be applied to other areas supporting factory operations including energy distribution and management via smart grids, storage and power electronics that enable reliable, flexible electricity supply. As AI integration broadens, the Smart Energy strategy’s long-standing exposure across the entire energy value chain will help the team identify which companies are best positioned to integrate and deploy AI technologies to optimize energy flows and future growth.

*All companies referenced in this article are for illustrative purposes only in order to demonstrate the investment strategy on the date stated. The companies are not necessarily held by the strategy nor is future inclusion guaranteed. This is not a buy, sell or hold recommendation, nor should any inference be made on the future development of these companies.

Footnotes

1 IEA website, “Industry — Energy Efficiency 2025.

2 IEA, World Energy Outlook 2025

3 IEA, Energy Efficiency Market Report, November 2025. Total final consumption in 2024 was over 450 EJ and has grown by around 25 EJ since 2019. Industry accounts for the largest share of this demand, at nearly 40%. Industry saw the strongest growth since 2019, contributing two-thirds of the total increase in global energy demand.

4 Robeco company research; Hannover Messe 2025 disclosures. AI-embedded products: mid-single-digit to low-teens share of leading factory automation revenues.

5 Robeco company research; Siemens management disclosures, Hannover Messe 2025. Wheeled humanoid performed pick, transport, and handling tasks autonomously in live factory.

6 Robeco company research; Siemens Digital Twin Composer announcement, 2025. Scheduled launch mid-2026 via Siemens Marketplace; built on NVIDIA Omniverse.

7 Robeco company research; Schneider Electric / AVEVA / NVIDIA disclosures. Grid-to-chip digital twin modelled with ETAP software.

8 Robeco company research; Hitachi management disclosures. AI agent diagnostics deployed across industrial equipment and power networks.

9 Robeco company research; Nexans management disclosures. AI-driven analytics for failure prediction and real-time grid optimization.

10 Qviro, technical analysis cited in Articsledge, “AI Humanoid Robots 2026,” 2026.

11 International Federation of Robotics, World Robotics 2024.

12 Springer Nature, “Digital Twin-Based Self-Learning Decision-Making Framework for Industrial Robots,” IJAMT, June 2025. FANUC ER-4iA pick-and-place: 74.79% energy reduction via Bayesian optimization.

13 GlobalSpec, “Humanoid Robots Are Tripping Over Their High Energy Demands,” September 2025. Current runtimes: 2–4 hours per charge.

14 Intel Market Research, “Humanoid Robot Rotary Actuator Market Outlook 2025–2032,” 2025. QDD actuators: 3–5x greater torque-to-weight vs. harmonic drives.

15Intel Market Research, 2025. Brushless motors and magnetic gear tech pushing actuator efficiency beyond 90%.

16 McKinsey & Company, Turning humanoid supply chain constraints into billion-dollar wins, April 2026.

トレンド投資とは?

ニュースレター(英文)に登録して、テーマ型投資の最新動向を入手しましょう。

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会