Co-Portfolio Manager

• インサイト

Autonomous vehicles and the rise of physical AI in mobility

Electrification was the first phase of the mobility revolution. Physical AI is the next. Together, they illustrate why the Smart Mobility theme has never been solely about vehicles, but about investing in the technologies, supply chains and value chains at the intersection of some of the most powerful structural trends reshaping the global economy.

執筆者

主なキーワード

まとめ

- Mobility is at the forefront of electrification and broader technological change

- AVs are visible and viable demonstrations of physical AI in action

- Smart Mobility provides exposure to diverse AI enablers and structural growth

Transportation is undergoing one of the most significant transformations in its history. Just a decade ago, electric vehicles (EV) were slowly ramping up production and emerging as a viable challenger to gas-powered cars. Now, EVs are a formidable force, embedded not only in commercial transport but also in the daily lives of consumers globally. In just a few short years, by 2030, electrically powered motors are expected to surpass the internal combustion engine (ICE) as a share of all passenger vehicles sold (see Figure 1). But the rise in EVs goes beyond the vehicle.

It is one of the clearest and most visible expressions of a broader electrification trend that is reshaping industries, infrastructure and supply chains across the global economy. And as mobility once served as the proving ground for electrification, it is now becoming the proving ground for the next major technological shift: physical AI. This is why the Smart Mobility strategy extends far beyond the automotive sector. It sits at the intersection of several structural forces shaping the next economy, including electrification, physical AI, automation, and the energy transition.

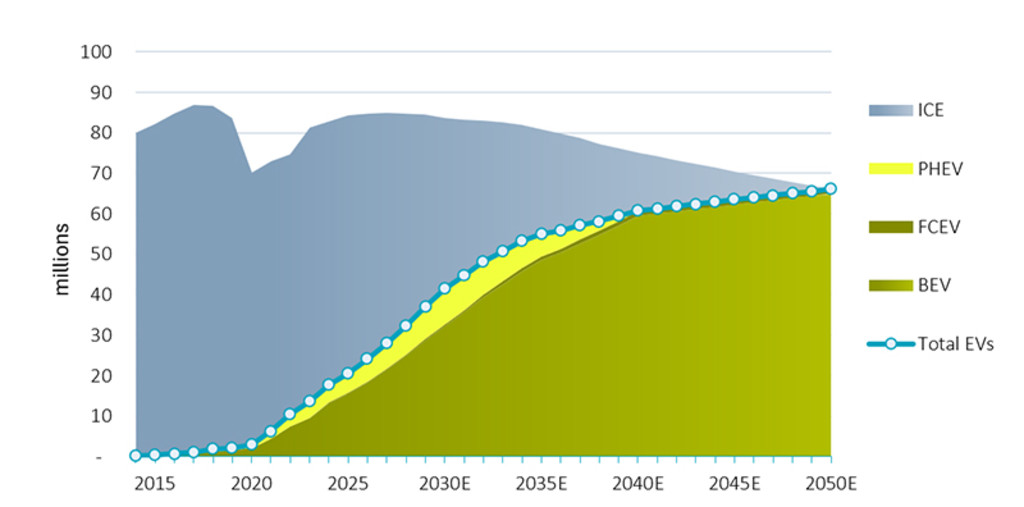

Figure 1 – EV uptake continues to grow globally

The graphic indicates the global market for light vehicles by powertrain type (ICE = Internal combustion engine; PHEV = Plug-in hybrid electric vehicle; FCEV = Fuel cell electric vehicle; BEV = Pure battery electric). By 2030, half of all light vehicle sales globally will be powered by electric powertrains versus conventional combustion engines. By 2040, this share is expected to rise to 80%.

Source: BNEF, Robeco. 2025

EVs helped transform a complex industrial trend into something consumers could see, experience and adopt. Just as EVs brought electrification onto the road and into view, autonomous vehicles (AVs) are bringing AI into the physical world. They represent one of the first and certainly the most visible end-use applications of physical AI. In contrast to the relatively invisible world of high-speed data processing, with AVs, consumers can see how AI interacts with the real world, with systems capable of perceiving their surroundings, making decisions and acting in real time.

Autonomous driving – physical AI in action

Autonomous driving (AD) is no longer an uncertain or untested technology hovering in the pilot stage. With robotaxis currently operating in major cities across the United States, China and the Middle East, AVs are a commercial reality. Waymo and Zoox are expanding aggressively in major cities across the US and have now joined Tesla as household names.* Waymo has a fleet of more than 3,000 vehicles that provide more than 500,000 paid rides each week, a figure it expects to push to one million by the end of 2026.12 At such speed, analysts expect roughly half of Americans will have access to robotaxi services by 2029. 3 Near-term rollouts in Tokyo and London are also anticipated. 4

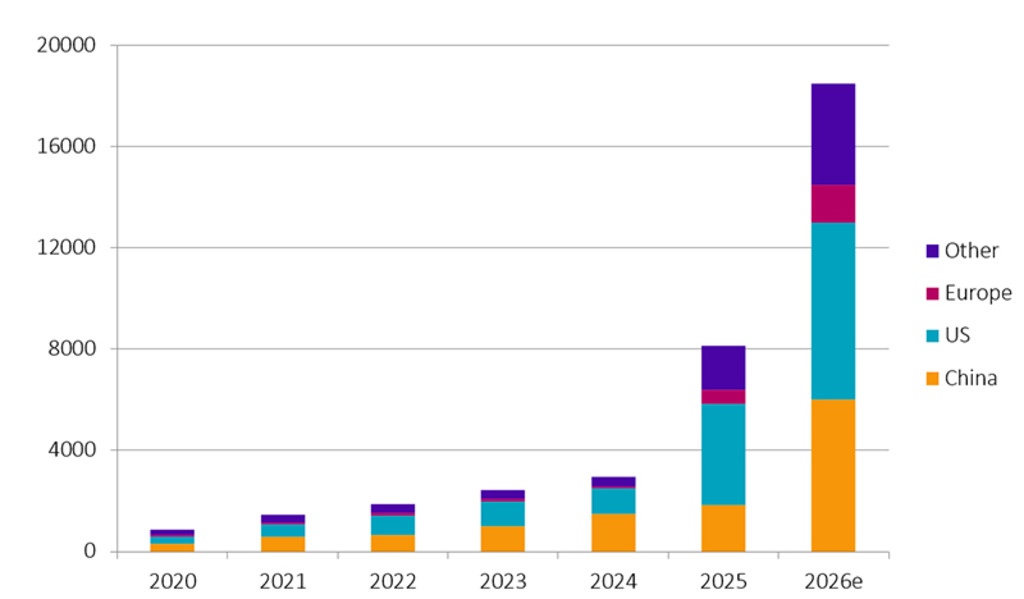

Figure 2 – Robotaxis fleets are growing rapidly

Source: BloombergNEF, Robeco, 2026.

Commercial operations at such scale demonstrate that autonomous mobility has moved beyond pilot projects into real-world deployment. More importantly, autonomous driving is not simply another automotive technology. It is one of the clearest examples of physical AI in action. Unlike generative AI, which operates primarily in largely invisible digital environments, autonomous systems must perceive, reason and act within the physical world.

AVs – ready to take on roads and loads

The opportunities to improve road safety are immense. Data from upwards of 220 million driverless miles confirms Waymo’s robotaxis are 10x safer than humans.5 BYD, China’s EV giant, is proudly putting its prowess to the test. Its confidence in the absolute safety and security of its new autopilot system, dubbed ‘God’s Eye’, is so certain that it is offering unprecedented full damage coverage in case of accidents.6

Achieving this requires extraordinary computing power combined with advanced sensing technologies, connectivity systems, software architectures and AI training models.

While robotaxis remain an important opportunity, freight and logistics may offer an equally compelling pathway toward AV adoption. AVs would be a welcome solution to chronic driver shortages, high turnover, and human hours of service limitations faced by freight operators, even as e-commerce demand and deliveries rise.7 Autonomous and semi-autonomous vehicles are already being used in controlled environments such as warehouses, ports, mines and industrial sites. These are providing vast amounts of real-world performance data that can be leveraged to deploy AV systems in more complex and dynamic roadway environments.

Under the hood

Every EV depends on a sophisticated technology ecosystem. Power semiconductors regulate electric flows. Battery management systems optimize performance and safety. Analog chips convert real-world signals into usable information. Software coordinates thousands of decisions every second. Radar, lidar, cameras support advanced driver assistance and autonomy. Connectivity systems link vehicles to drivers, infrastructure and cloud-based services. That makes an autonomous vehicle a mobile AI platform on wheels. AVs accelerate the technological shift. As autonomy advances, the value contribution from software, sensors, computing and electronics continues to grow (see Figure 3).

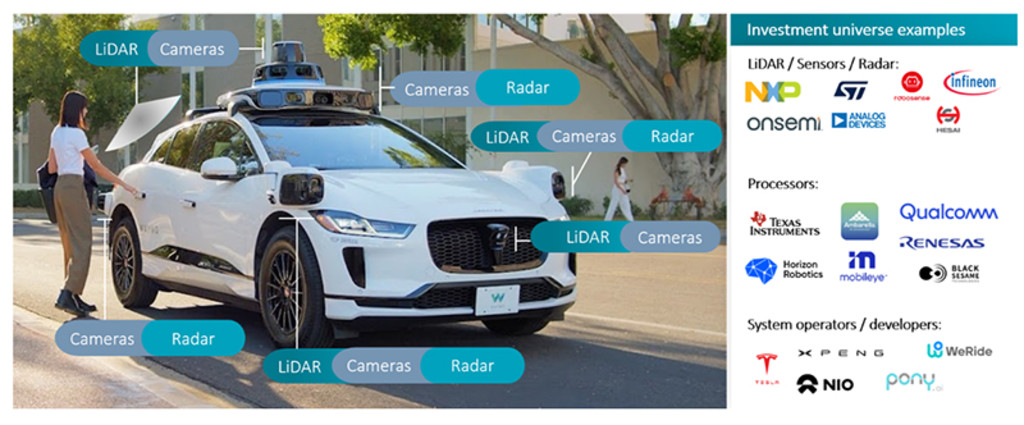

Figure 3 – Vehicles of change built with next-gen technologies

The image illustrates of sensors and compute in a Level-4 autonomy, Waymo (Jaguar i-Pace) Robotaxi. EVs and AVs are hyper-processing AI platforms on wheels, combining AI chips, sensors, software, connectivity and batteries. LiDAR (Light Detection and Ranging) is a sensing technology which emits laser beams and builds 3D images of the surroundings based on how the light reflects back.

Source: Waymo, Morgan Stanley Research, 2026.

What’s important for investors is that these technologies are not limited to transportation. The same AI processors powering autonomous driving also support data centers and AI infrastructure. The same machine-vision capabilities used by vehicles increasingly power industrial automation and robotics. The same sensors enabling autonomy are finding applications across manufacturing, logistics and smart infrastructure. The same batteries and power-management technologies supporting EVs also underpin energy-storage systems and grid modernization.

Physical AI, in other words, is not solely a mobility story; it’s about structural growth across major sectors encompassing significant swaths of the broader economy – growth in which investors in the Smart Mobility can participate via exposure to increasing vehicle intelligence.

Diversified structural tailwinds supporting long-term growth

While physical AI and autonomous mobility may represent the next phase of growth, the original pillars of the investment case remain firmly intact. Electrification continues to advance globally, supported by improvements in affordability, technology and infrastructure. Moreover, decarbonization objectives remain central to government and corporate planning. Energy security concerns continue to encourage investment in domestic supply chains, power systems and energy-storage capabilities.

This makes the Smart Mobility strategy far more than a transportation theme. Sitting at the intersection of many of the most transformative shifts of our time, it enjoys access to an impressively long, robust and dynamic opportunity set. The investment team seeks to benefit from this unique position as these trends converge and scale across the broader economy.

As long as economies continue to electrify, automate and digitize, Smart Mobility companies should experience persistent forward momentum as these long-term trends unfold.

The Smart Mobility strategy is not simply an investment in vehicles and the future of transport. It is itself a vehicle for gaining exposure to the technologies, infrastructure and innovation driving the next phase of economic growth.

* All companies referenced in this article are for illustrative purposes only in order to demonstrate the investment strategy on the date stated. The companies are not necessarily held by the strategy nor is future inclusion guaranteed. This is not a buy, sell or hold recommendation, nor should any inference be made on the future development of these companies.

Footnotes

1 Alphabet Investor Presentation, June 2026.

2 Waymo goes driverless in Las Vegas, with Denver, San Diego, Tampa next, Electrek, July 2026.

3 ‘See how the robotaxi industry is taking off across the US’, Wall Street Journal, May 2026.

4 Ibid, footnote 2.

5 Waymo, Safety Impact report, December 2025.

6 Liability coverage is conditionally limited. See BYD website for more details. BYD, May 2026.

7 Aurora Investor Presentation, 2026.

トレンド投資とは?

ニュースレター(英文)に登録して、テーマ型投資の最新動向を入手しましょう。

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会