Portfolio Manager

• インサイト

Affordability is steering consumer spending trends

Inflation is easing, but consumer sentiment and purchasing behavior suggest that households remain vigilantly focused on value and affordability. Spending patterns are diverging, with affluent households driving consumption growth, while lower-income cohorts cut back. The battle for consumer hearts (and wallets) is heating up with retailers competing on not just lowest price but on their ability to deliver the greatest value.

Summary

- Affordability is top of mind for consumers and the companies serving them

- Consumers feel gloomy, but spending is resilient

- Scaled-value retailers, off-price and second-hand are benefiting

Boardroom vocabulary now mirrors kitchen-table conversations. Companies across consumer staples and consumer discretionary segments are discussing ‘affordability’ with striking frequency; mentions among executives have tripled over the past five years through Q1 2026 (see Figure 1). Households are watching every dollar, and companies have noticed.

The squeeze in numbers

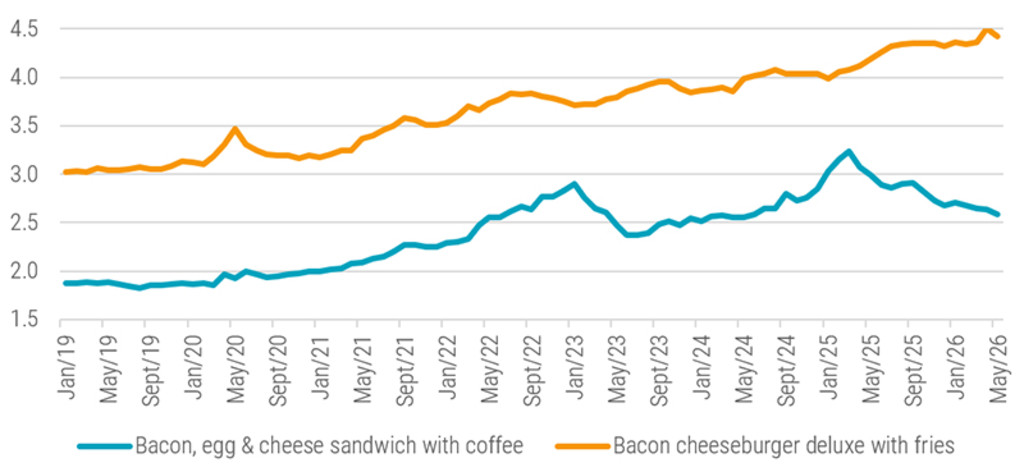

Everyday items are now causing ‘sticker shock’ for many consumers – the unpleasant surprise of an unexpectedly high price. Bloomberg’s price index for an American bacon, egg, and cheese sandwich with coffee has climbed 38% (from USD 1.87 in 2020 to 2.58 in 2026). The cheeseburger-deluxe-with-fries combo rose 42% (from USD 3.12 to 4.43 (see Figure 1). These real-world ‘bites’ explain why so many consumers still feel poorer even as US inflation has cooled from a peak of 9.1% in 2022 to 4.2% in May.

Figure 1 – Price index of widely consumed meals in the US

Source: Bloomberg, 2026.

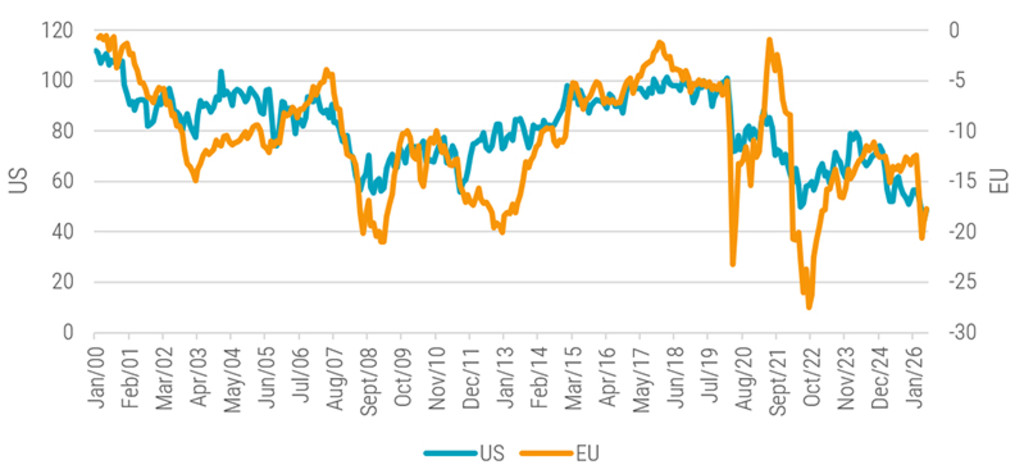

What’s more, households on both sides of the Atlantic feel they are losing ground. The University of Michigan’s Consumer Sentiment Index (US) fell from around 100 in 2020 to a new all-time low of 45 in May; levels typically associated with recessions. European sentiment slipped from -12 in February to -18 in June, its sharpest two-month deterioration in many years (see Figure 2).

Figure 2 – Consumer sentiment index

Source: University of Michigan, Eurostat, 2026.

Watch what they do, not what they say

Fortunately for retailers, the gloom and doom consumers feel has been offset by resilient employment and incomes. US unemployment remains low at 4.3% (as of May 2026), and jobless rates in other major economies are also within a healthy 2.5-6% range. Meanwhile, retail sales continue to grow, suggesting only a weak link between sentiment and actual spending. US payment volume growth confirms this, rising about 9.0% through April, up from 7.5% in Q1. Globally, volumes grew 9.0% in Q1 up from 8.0% in Q4, reinforcing the adage: ‘watch what consumers do, not what they say’ (see Figure 3).

Figure 3 – Retail spending is on the upswing in most major economies

Source: US BLS, Eurostat, Japan Ministry of Internal Affairs, China National Bureau of Statistics, Central Statistics Office India, 2026.

A K-shaped paradox

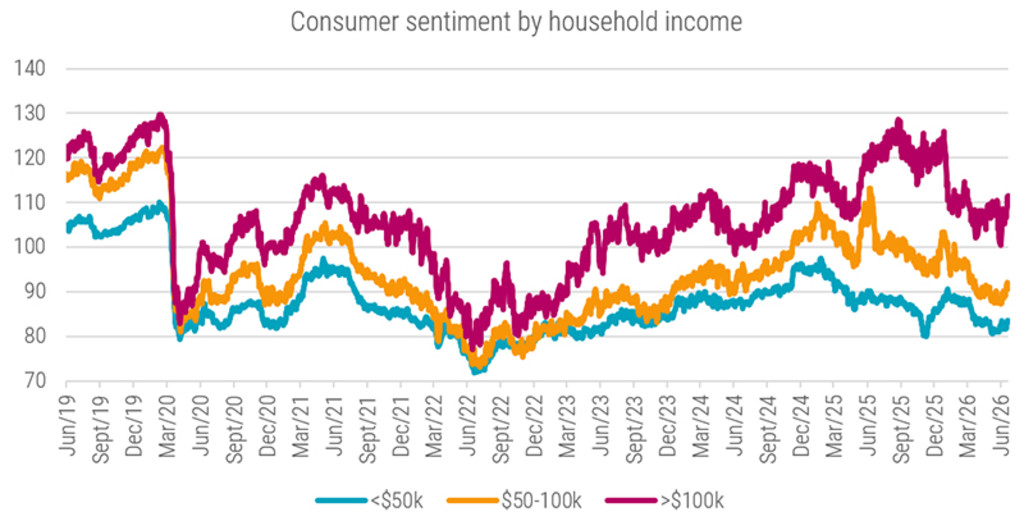

Earnings are growing stronger for lower-income earners relative to higher-income cohorts, but they are still spending less, resulting in a ‘K-shaped’ economy. As a result, companies must speak to two audiences: the wealthier shopper still willing to pay for performance, and the squeezed shopper who needs everyday prices to fall. US labor data show that since early 2019 through present, real wages (after inflation) have actually grown more for low earners than for higher ones. Moreover, all income cohorts outpaced inflation. At the same time, the spending data reveals a starkly two-track economy. Higher-income US households are spending more (5%-10% growth) since the start of 2025, while spending from lower-income households has slowed and in some cases reversed.

Figure 4 – Consumer sentiment is diverging for low- and high-income households

Source: Morning Consult, Bloomberg, May 2026

Similar trends are observed by travel companies which say wealthier consumers are spending freely on travel, dining, and premium experiences. Luxury hotelier Hyatt* said demand from premium customers was exceptionally strong this past quarter, increasing approximately 7% compared to last year. Another perceived luxury item, cruise travel, is also enjoying wind in its sails. The world’s two largest cruise lines Royal Caribbean and Carnival have posted record booking and pricings as bundling accommodation, meals and entertainment into a single fare is perceived as a good value compared to land-based holidays.*

Consumer behavior shifts to value

Consumer behavior is shifting decisively toward value and cost-consciousness. Roughly 75% of US households are trading down to cheaper brands and retailers, while half are delaying discretionary purchases. Consumers are also cutting back on eating and drinking out. But price isn’t the only decision variable – in addition to hunting bargains, consumers are collecting loyalty points from their favorite brands and gravitating toward more perceived value.

Retailers are swiftly adapting and scaled-value retailers are the clearest beneficiaries. Walmart* is leaning into value, so in addition to lower prices, it’s expanding its in-house private label range and offering same-day shipping. Amazon’s everyday essentials and grocery categories are also growing fast and now represents one in three units sold. Like Walmart, Amazon* is increasing value via convenience with its same-day delivery on low-priced items.

Consumer behavior is shifting decisively toward value and cost-consciousness. Roughly 75% of US households are trading down to cheaper brands and retailers

The popularity of private labels is also rising, with US sales hitting a record USD 283 billion in 2025 – almost a quarter of unit volumes. Costco’s* Kirkland Signature generated an estimated USD 80 billion in annual sales last year (larger than most global retailers). By mid-2026, Gen Z is expected to spend a higher share of budgets on in-store brands than any other generation, suggesting the shift is structural rather than cyclical. Consumers are also looking for steeper discounts and flocking to off-price chains such as TJ Maxx, Marshalls, HomeGoods, Ross Stores and Burlington*, all of which report solid growth.

Second-hand has also gone mainstream, as a growing share of value-seeking consumers no longer associate ‘great value’ exclusively with new goods. The online marketplace eBay* has posted double-digit growth as it attracts higher-income shoppers who are economically and sustainably minded. Resale platforms such as Vinted, Depop and Poshmark* have also continued to scale to capture a second-hand apparel market worth USD 350 billion by 2028.

Second-hand has also gone mainstream, as a growing share of value-seeking consumers no longer associate great value exclusively with new goods

Prices and promotions are also on the menu in retail food. McDonald’s* has successfully won back low-income diners with the launch of its McValue menus. These have helped restore momentum across most of its markets. Taco Bell, Wendy's, Chipotle and even fast-casual Panera have followed with their own value menus. While many fast-food chains have improved their value offering, they continue to face headwinds including more people eating at home and adoption of weight loss drugs that reduce calorie intake.

What’s clear is that companies best positioned to capture today and tomorrow’s consumers focus on 1) building trust by delivering consistent value rather than short-term promotional gimmicks; 2) investing in extra product or service features so that ‘low-price’ does not equate with ‘low quality’; and 3) communicating the value proposition early and often.

*The companies referenced are for illustrative purposes only in order to demonstrate the investment strategy on the date stated. The companies are not necessarily held by the strategy nor is future inclusion guaranteed. This is not a buy, sell or hold recommendation, nor should any inference be made on the future development of these companies.

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

Important information

insights.detail.disclaimer.text