Portfolio Manager

• 月次アウトルック

The new scarcity: Diversification

Diversifying portfolios is becoming more difficult as asset classes move in the same direction, and while equities are dominated by Big Tech, Robeco’s multi-asset team says.

執筆者

Client Portfolio Manager

主なキーワード

まとめ

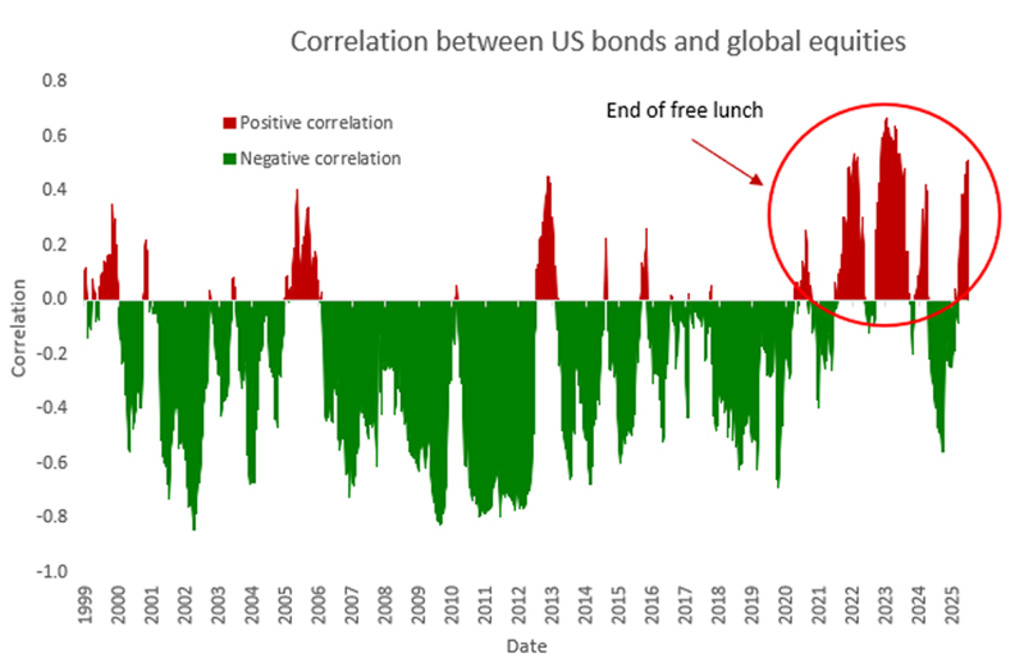

- The negative correlation between equities and bonds has disappeared

- Investors should blend quant and fundamental techniques to find winners

- Consider alternative sectors like commodities, small caps, and EMD

A high correlation between stocks and bonds means switching from one to the other does not offer the risk/return diversification that it once did, says Mathieu van Roon, Portfolio Manager with the Investment Solutions Multi-Asset team.

Meanwhile, the mega-cap concentration within stocks, as only a handful of Magnificent Seven and other tech companies account for the bulk of market returns, presents poor diversification opportunities within the same asset class.

Instead, investors should look at the more unloved parts of the market, including private equity replication strategies, commodities, small-caps, and emerging market debt, Van Roon says.

“For decades, multi-asset investing meant balancing equities and bonds in a traditional 60-40 portfolio,” Van Roon says. “This also proved useful when equities and bonds moved in different directions; when stocks went down, bonds went up, and vice versa. That worked when diversification was abundant and economic regimes were stable.”

“Today, geopolitical uncertainty, inflation and technological disruption mean investors can no longer rely on a simple two-asset portfolio. Even as markets reach new highs, portfolios have become increasingly concentrated around a narrow set of risk drivers.”

“Technology dominates global equity markets. A handful of mega-cap companies drive an ever-larger share of developed market returns, while emerging markets are increasingly exposed through semiconductors, AI infrastructure and digital platforms. As a result, many investors may be less diversified than they realise.”

Moving together in tandem

The negative correlation between equities and bonds has not been present in recent years, particularly since the war in Ukraine began in 2022, remaining a positive correlation until 2025. The negative correlation resumed in 2025 but it has now turned positive again in 2026.

Figure 1: The relationship between global equities and US Treasuries since 2000

Source: Robeco, Bloomberg, July 2026

“Meanwhile, globalization is giving way to geopolitical rivalry, supply-chain reshoring and greater policy fragmentation,” Van Roon says. “Corporate credit spreads also remain close to historic lows, leaving investors with limited compensation for taking additional credit risk.”

“There is no silver bullet, but investors can take steps to reduce portfolio concentration. Core equity and credit allocations can be worked harder to deliver more consistent returns, rather than the traditional method of merely mixing various investment styles.”

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

Combining quant with fundamental

Instead of simply blending equity and credit styles between value and growth, a new paradigm is emerging – combining quantitative and fundamental investing – says Jonathan Arthur, Client Portfolio Manager with the team.

“Quant investing identifies opportunities across large datasets, while fundamental investing provides forward-looking insights and economic judgement,” he says. “Together, they create a more balanced risk/return profile across market cycles with less tail risk. This ‘dual alpha’ approach can strengthen both core equity and core credit portfolios.”

“Next, investors more than ever need to look beyond today’s high-momentum trades and have the conviction and open mindedness to search for longer-term winners. This naturally broadens the investment universe beyond traditional equity and bond allocations to include more outspoken regional tilts, and by adding emerging market debt, small caps, commodities, and alternative return sources.”

Core and satellite allocations

The multi-asset team does this for Robeco portfolios by implementing satellite allocations around a core portfolio structure. The core provides broad market exposure and forms the long-term foundation of the portfolio. Around that foundation, satellite allocations introduce differentiated sources of return that can complement traditional stock and bond holdings.

“Examples of these satellites include listed private equity replication strategies, which seek to capture many of the attractive characteristics of private markets while maintaining the liquidity and transparency of public markets,” Arthur says.

“Commodities have helped during recent periods of inflation surprises or supply disruptions, and we believe they are a main stay of the portfolios during various market cycles. Emerging market debt provides exposure to different growth dynamics and income opportunities, with a risk profile that is much more corporate credit-like, but with returns that are comparable to high yield.”

Targeting long-term themes

“Global small caps trade at historically attractive valuations, and the recent softening in rate-path expectations may act as a catalyst for greater investor interest in this somewhat unloved part of the market.”

Satellite allocations can also target long-term structural themes, Van Roon says. “While AI and digitalization dominate investor attention today, thematic leadership rarely remains constant,” he says.

“Clean technology, for example, has regained momentum as policy support during the recent Iran crisis when oil supply routes were shut off, lower financing costs and rising electricity demand have improved its outlook.”

Seeking multiple return sources

“Other overlooked themes may follow. Water infrastructure benefits from increasing scarcity and aging networks, while healthcare innovation is driven by demographic trends and scientific breakthroughs. The objective is to maintain exposure to multiple long-term trends as leadership evolves over time.”

“The years ahead are unlikely to be defined by one region, asset class or technology theme,” Arthur adds. “Instead, investors face greater uncertainty, wider performance dispersion and more frequent market rotations.”

“Portfolios with multiple sources of return are likely to be better positioned to capture opportunities and manage risk. Looking forward, diversification may become one of the most important drivers of investment success.”

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会