Strategist

• インサイト

Warsh's first Fed meeting: A new era for Fed communication?

執筆者

Strategist

Strategist

主なキーワード

まとめ

- Committee split on whether to hike in 2026

- Expect the Fed to hold rates steady

- Labor market stabilizing

At his first FOMC meeting as Chair, the policy decision itself attracted less attention than the changes in how the Fed communicated it. The statement was cut roughly in half, forward guidance was removed, and Warsh chose not to publish his own interest rate projections. Together, the moves suggest a different communication philosophy may be emerging at the Fed.

What became clear at Warsh's debut meeting is that he is not a fan of extensive forward guidance. That philosophy was immediately reflected in a statement that was roughly half the length of previous ones and the removal of explicit guidance on the future path of policy.

The changes appear to be more than a stylistic preference. In our view, Warsh intends to fundamentally change how the Fed communicates. He sees little merit in forward guidance, believing it was one of the main reasons the Fed was slow to raise rates during the 2021-22 inflation shock. The shorter statement is a positive development, reducing the need for markets to scrutinize every word the Fed uses to describe the economy.

Providing less guidance could ultimately lead to more predictable policymaking

Warsh also chose not to publish his own interest rate projections, underlining his reservations about the current Summary of Economic Projections (SEP). We interpret this as another signal that he wants to change the current framework. Rather than relying on individual policymakers' point estimates, the Fed could move toward a more scenario-based approach, similar to that used by the ECB and the Bank of England. While this is still a form of forward guidance, it focuses less on predicting the exact path of rates and more on explaining how policy is likely to respond under different economic outcomes.

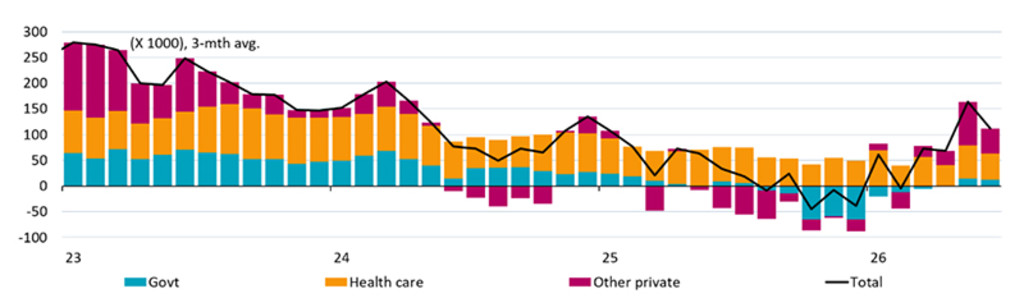

Monthly US Non-Farm Payrolls growth

Source: Bloomberg, Robeco, 6 July 2026

Credibility first

Warsh struck a distinctly hawkish tone throughout the press conference, repeatedly stressing that price stability remains the committee's primary objective. That emphasis appears to have been deliberate. In our view, the hawkish communication helped establish his inflation-fighting credentials while also demonstrating independence from the White House. Markets viewed that message as credible: inflation expectations implied by inflation-linked bonds declined following the press conference.

A Fed driven by data, not promises

Warsh also announced five committees to review aspects of Fed policymaking, ranging from communication to the data used in policy decisions. While these reviews suggest institutional change may lie ahead, they do not necessarily imply a different policy outlook.

Ultimately, the data will continue to drive decisions. We are paying particularly close attention to developments in the labor market, while lower energy prices and a softer June employment report reduce the immediate pressure to tighten policy further.

What it means for investors

For now, we continue to expect the Fed to remain on hold, even though markets have priced in at least one additional rate hike this year.

Removing forward guidance is likely to increase volatility at the front end of the Treasury curve, as every policy meeting effectively becomes live. However, Warsh has also emphasized that the Fed will not react to individual data releases, but instead focus on broader trends in the economy. Paradoxically, providing less guidance today could ultimately lead to a more predictable policy framework over time.

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会