Researcher

• インサイト

How Value investors can avoid the climate traps

Successful value investing and the decarbonization of portfolios are typically considered difficult to reconcile. This is especially the case after the recent comeback made by stocks from the energy sector, which often fall in the value camp. But we show it would have been possible to achieve both strong exposure to the value factor and a substantially lower carbon footprint than conventional value strategies.

執筆者

Researcher

主なキーワード

まとめ

- Conventional Value investing exposes investors to climate traps

- Value strategies can be ‘decarbonized’ effectively

- Decarbonized Value remains attractively valued

Investors often face a dilemma when trying to both decarbonize their portfolio and get exposure to the value factor. The reason is that conventional value strategies tend to have high environmental footprints, including greenhouse gas (GHG) emissions, and are therefore typically exposed to what we call ‘climate traps’.

Such stocks may look cheap using common valuation metrics, but this is mainly because their environmental footprints are not well reflected in accounting numbers. Also, with the rise of sustainable investing, high-footprint stocks are expected to show structurally lower valuations. These stocks will turn increasingly attractive based on simple value metrics, implying that such metrics may no longer be adequate.

Effective value investing requires adjusting valuation models for future carbon costs

Effective value investing therefore requires adjusting valuation models for these future carbon costs. Considering this, we designed an innovative methodology to derive a ‘decarbonized value’ signal in 2019.1 This methodology adjusts the valuations of high-polluting firms, making them less attractive based on their environmental footprints and works, economically speaking, similarly to a pollution tax. 2

Our research shows that this approach would have effectively reduced the carbon footprint of value strategies over the 1986-2023 period, without giving up exposure to the value factor. Indeed, simulations suggest that the adjustments made do not cause major changes in terms of value exposure at portfolio level. As a result, decarbonized value can have a value exposure comparable to the conventional one.

In fact, we see that while some performance differences did appear over shorter periods of time, the correlation between the two value strategies generally remained very high over the past three and a half decades, and both performances tracked each other closely over the long run. Importantly, decarbonized and conventional value exposures offered comparable historical returns.

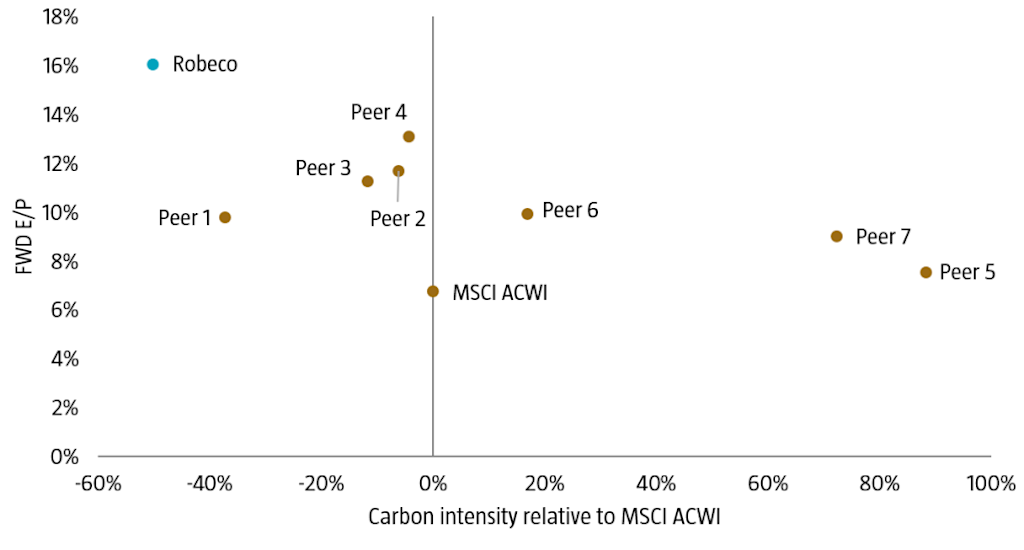

Moreover, we find that this holds true not just for simulated portfolios, but also in practice for real portfolios. Figure 1 plots these two measures for a set of value managers, including our Robeco QI Global Value Equities strategy, that implements our decarbonized value approach. The x-axis shows the relative carbon intensity, while the y-axis shows the forward price-to-earnings ratio.

Figure 1: Value exposure versus carbon footprint of set of Value

Source: Robeco, Morningstar, Refinitiv, I/B/E/S. The chart shows the forward earnings-to-price ratio (FWD E/P) and the carbon intensity relative to MSCI ACWI Index for a sample of global fundamental and quantitative value managers from Morningstar as of December 2022.

As the chart illustrates, most value managers have a larger or similar carbon footprint compared to the index, while two value managers – including Robeco – have a footprint below the index. At the same time, the value metrics of the portfolio remain high on our portfolio, showing that high value exposure is combined with a low carbon footprint, and low exposure to climate traps.

Value remains very attractive from a valuation perspective

Finally, we find that despite the significant market rotation seen since November 2020 and the related value comeback, both conventional and decarbonized value approaches continue to trade at attractive valuation spreads. More specifically, for both strategies, the valuation spread between value and growth stocks is much wider at the end of March 2023 than at the beginning of the value winter in 2018.

Conventional and decarbonized value approaches continue to trade at attractive valuation spreads

In fact, current spreads are still at levels close to those seen at the peak of the dot-com bubble in 2000, meaning that both conventional and decarbonized value continue to trade at very attractive valuation levels, from a historical perspective. Despite the strong rebound of value stocks over the past couple of years, conventional and decarbonized value approaches still have significant upside potential.

Footnotes

1 Swinkels, L., Ūsaitė K., Zhou, W., and Zwanenburg, M., October 2019, “Decarbonizing the Value factor”, Robeco article.

2 Cf., Blitz, D., and Hoogteijling, T., April 2022, “Carbon-Tax-Adjusted Value”, Journal of Portfolio Management.

クオンツ運用の価値を探求

最先端クオンツ戦略の情報やインサイトを定期的にお届けします。

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会