PhD, Portfolio Manager Sustainable Index Solutions

• インサイト

Robeco’s residual momentum: less risky and more sustainable

Behavioral explanations of momentum suggest that momentum can be caused by overreaction or underreaction. The latter, which turns out to be less risky and more sustainable, is exploited in Robeco’s quantitative models.

執筆者

まとめ

- Momentum: stocks that performed well in the past continue to do well in the following period and vice versa

- Momentum is caused by over- or underreaction to news

- Generic momentum strategies mainly benefit from overreaction, thus aggravating mispricing and being prone to reversals

- The momentum factor in Robeco’s quantitative equity models is driven by underreaction, improving market efficiency and obtaining more consistent return

The momentum effect is the tendency of stocks to show persistence in performance: stocks that performed well in the recent past, on average outperform other stocks in the subsequent period, while the opposite holds for stocks with poor returns.

While there is a vast amount of evidence on the existence of the momentum effect, there is still an ongoing academic debate on the source of the momentum premium. Behavioral explanations attribute momentum to either underreaction or overreaction.

Overreaction can be attributed to investors’ delayed overreaction to stock-specific news, herding behavior and return chasing behavior. Underreaction can be caused by investors’ underreaction to stock-specific news, as they rely too heavily on the first information available (anchoring bias) or diffuse the information slowly. Another explanation is that investors sometimes hold on to losers to avoid admitting mistakes while quickly selling winners to show success.

Momentum from overreaction: risk of price reversals

Identifying the source of a stock’s momentum, i.e. over- or underreaction, matters, because it gives insight into the expected risk and sustainability of a momentum strategy. A momentum strategy that buys a winner stock which suffers from overreaction causes upward price pressure on that stock, makes the price drift even further away from its intrinsic value and hence aggravates the mispricing. Sooner or later, the market will realize this and the price of the stock will revert towards its fundamental value. Hence, a strategy profiting from momentum driven by overreaction runs the risk of stock price reversals.

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

Momentum from underreaction: less risky, more sustainable

A strategy based on momentum from underreaction will lead to price pressure that actually diminishes the mispricing and is therefore not prone to reversals in stock prices. It is therefore less risky and more sustainable, because its return comes from making the market more rather than less efficient. We therefore prefer underreaction as a source of a momentum strategy.

Robeco quant models use momentum from underreaction

Robeco applies a proprietary ‘residualization’ technique that isolates the stock’s momentum that can be attributed to the stock-specific component and eliminates the part of a stock’s momentum that is due to its systematic component. This technique is applied to the momentum factor in all of Robeco’s quantitative stock selection models.

News that results in high total returns on stocks makes these stocks susceptible to overreaction, as investors start to chase returns and institutional investors are often constrained to stay close to their benchmarks. This does not hold for news that results in high stock-specific returns, as this does not necessarily lead to higher returns. That is why we expect overreaction to be the main driver of total return momentum and underreaction the primary source of Robeco’s residual, stock-specific momentum.

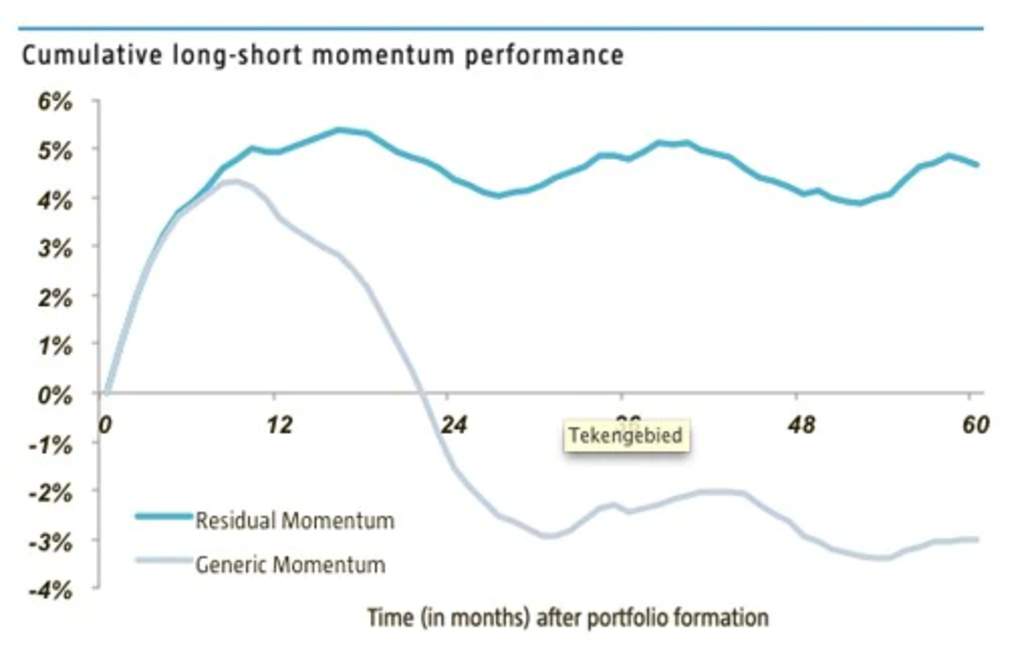

The graph below confirms that residual momentum is not prone to the price reversal associated with overreaction, unlike a generic total return momentum strategy.

Cumulative long-short momentum performance

Average cumulative performance after formation of long-short portfolios that start each month in the period January 1986 to December 2012 and are held for 60 months. The universe consists of the largest 3,000 constituents of the S&P Broad Market Index each month. A residual (generic) momentum portfolio consists of equal long/short positions in the top/bottom decile residual (generic) momentum stocks of the universe.

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会