Portfolio Manager

• Visión

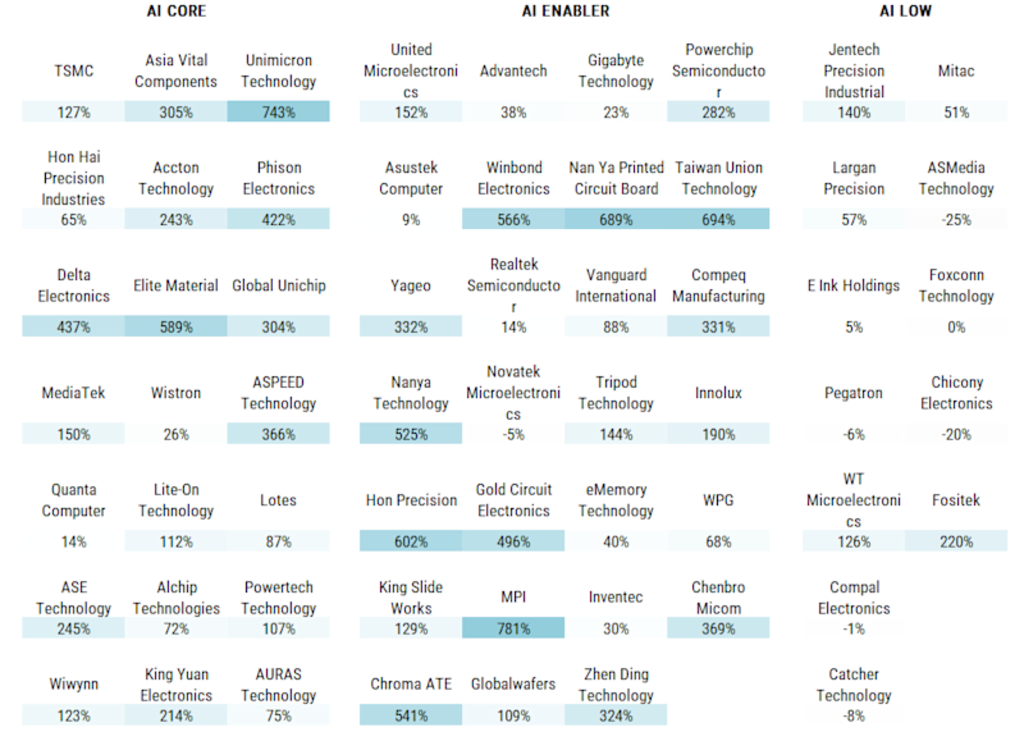

Quant chart: Beyond TSMC – Mapping Taiwan’s AI technology ecosystem

TSMC* may dominate emerging market technology exposure, but Taiwan’s AI value chain extends far beyond a single company. This edition of the quant chart explores how and where.

Summary

For emerging market investors, Taiwan Semiconductor Manufacturing Company, or TSMC, has become impossible to ignore. As the world’s leading advanced semiconductor foundry and a critical supplier to companies such as Nvidia, Apple and AMD, it sits at the center of the global AI value chain. Its market capitalization has surged to USD 1.66 trillion, giving it a 14.2% weight in the MSCI Emerging Markets Index. 1

That creates an interesting challenge. For many active UCITS strategies, single-stock exposure is constrained by diversification rules, meaning investors often need to look beyond TSMC for additional exposure to the AI theme. But while TSMC is a unique company with no obvious one-to-one substitute, Taiwan’s broader technology ecosystem offers a surprisingly deep bench of companies linked to the same structural trends.

* TSMC and all other companies named in this article are for illustrative purposes only. No inference can be made on the future development of the company. This is not a buy, sell or hold recommendation.

Taiwan’s technology sector includes a wide range of highly specialized companies operating across the AI supply chain. Some are directly involved in semiconductors and advanced chip design. Others provide the servers, power systems, cooling infrastructure, substrates, printed circuit boards, assembly, testing and networking equipment needed to scale AI deployment.

For this edition of the quant chart, we focused on 60 Taiwanese technology stocks2 and classified them according to their relevance to the AI value chain. The three categories are deliberately simple: AI Core companies are those with products or services that are central to AI infrastructure or represent a potential bottleneck in the value chain. AI Enablers support the wider AI build-out, even if they are not themselves the most performance-critical layer. Finally, companies with more limited or indirect exposure are classified as AI Low.

As with any framework of this kind, there is room for debate. The aim is not to create a definitive taxonomy but to show that AI exposure is not binary. Taiwan’s technology ecosystem includes both obvious beneficiaries and less obvious supporting players.3

Descubra el valor de la inversión cuantitativa

Suscríbase para conocer las últimas novedades y estrategias sobre inversión cuantitativa.

What the chart shows

The results are striking. Figure 1 shows the 12-month returns of the selected companies across the three categories. While TSMC’s rise has been remarkable (its market capitalization is still roughly 40% larger than the combined value of the other 59 names), much of the real excitement has actually happened beyond TSMC itself.

This is not necessarily surprising. Markets reward not only absolute importance but also the rate of change in expectations. Some AI enablers have delivered very strong returns because their role in the AI infrastructure build-out has become more visible. At the same time, some of the more obvious AI core names have already experienced a strong bull market in previous years.4

Examples can be found across the value chain. Delta Electronics supplies critical power and cooling systems for data centers. Quanta, Hon Hai Precision, Wiwynn and Wistron are major AI server manufacturers. Accton plays a crucial role in connecting GPUs across AI clusters and data centers. Nanya Tech produces memory chips, while ASPEED is the main player in server management chips. ASE, Powertech and King Yuan are key players in assembly and testing. Companies such as Unimicron, Elite Material and Zhen Ding produce (elements of) substrates and printed circuit boards, while Alchip, Global Unichip and increasingly MediaTek are active in customized chip design.5

Figure 1 | The Taiwanese Tech Landscape: 12-month returns

Source: Robeco analysis; Bloomberg. 12-month returns as of 19 May 2026. The companies shown in this graph are for illustrative purposes only. No inference can be made on the future development of the company. This is not a buy, sell or hold recommendation.

Why breadth still matters

The broader lesson is that Taiwan’s AI opportunity is not limited to one dominant company. It is a layered, fast-moving ecosystem in which different firms benefit from different parts of the AI infrastructure cycle.

For us quantitative investors, that breadth is important. A large universe of specialized companies creates scope to compare opportunities systematically across valuation, momentum, quality, analyst revisions and short-term signals. It also reinforces the importance of diversification. As exciting as the AI boom may be, not every AI-linked company will benefit equally, and strong recent performance does not remove the need for discipline.

This is why our EM quant strategies aim to maintain a diversified view of the opportunity set, with active overweights and underweights across the categories shown in Figure 1. The point is not to find ‘the next TSMC’, but to understand the wider ecosystem, and to assess where expectations, fundamentals and valuations still leave room for opportunity.

Footnotes

1All data as at 19 May 2026.

2Selecting the current largest 60 names on (investable) market cap creates a large hindsight bias, as well-performing stocks will enter the list because of a recent rise in the stock price. Hence, we took the investable market cap mid-period, six months ago, to establish the largest 60 names. In our EM Active strategies, as mentioned, our investment universe is much larger, typically leading to active overweights in smaller companies as well; however, these smaller companies are not part of our analysis of the top 60 Taiwanese tech stocks.

3Several AI enablers could be seen as AI Core, and several AI Low names could be classified as AI Enablers. Simply put, the Taiwanese tech ecosystem is at the heart of the AI boom.

4 For instance, some important AI names, particularly AI server builders such as Quanta, Hon Hai Precision, Wiwynn and Wistron, delivered somewhat less spectacular returns over the past 12 months, but mainly because these stocks had already enjoyed massive rallies during 2023 and 2024.

5We excluded Korean AI core names from this analysis, but adding companies such as SK Hynix (+773% over the past 12 months), Samsung (+397%), Leeno Industrial (+210%), Hanmi Semiconductors (+401%) and Wonik IPS (+480%) would of course tell a very similar story.