Portfolio manager, Boston Partners

• Visión

Por qué los valores industriales europeos merecen más atención

El aumento del gasto en activos reales está provocando que los valores industriales europeos resulten cada vez más atractivos, afirma Chris Hart, inversor en value.

Autores/Autoras

Resumen

- Europa se beneficia de la inversión en infraestructuras y defensa

- Los valores industriales ofrecen valoraciones atractivas y un interesante potencial de crecimiento

- El sector se diversifica eludiendo el riesgo de concentración que conllevan las Big Tech

Esta situación se debe a la inquietud de los inversores por las elevadas valoraciones de la renta variable estadounidense, que ha pasado a estar dominada por las Big Tech, lo cual ha provocado que muchos busquen oportunidades en otros ámbitos. Chris Hart, Portfolio Manager de Robeco BP Global Premium Equities, considera que hay diversos segmentos de mercado fuera de EE.UU. que ofrecen grandes oportunidades, especialmente en Europa.

«Las Big Tech de EE.UU. son caras y tienen grandes necesidades de capital», afirma Hart. «Los gastos de capital, específicamente en inversiones relacionadas con la inteligencia artificial (IA), de las grandes compañías tecnológicas han aumentado de forma espectacular en un periodo relativamente corto».

«Está por ver qué rentabilidad ofrecerán esas considerables inversiones y cuánta paciencia pueden tener los inversores a la hora de esperar dicha rentabilidad. Si los beneficios o el crecimiento resultan ser bajos, esto puede traducirse en una rápida revalorización del segmento, como se puso de manifiesto en abril de 2025».

Boston Partners, uno de los principales inversores en value, aplica un enfoque de inversión de larga trayectoria cuyo objetivo es identificar compañías fundamentalmente sólidas que cotizan a valoraciones atractivas y experimentan un momentum empresarial positivo.

Aunque en muchos segmentos del mercado de renta variable estadounidense las valoraciones están por encima del promedio histórico, el equipo de Boston Partners ha encontrado numerosas compañías de calidad en el extranjero que cumplen sus criterios, especialmente en el ámbito industrial europeo.

«Consideramos que el sector industrial europeo se encuentra hoy en la confluencia de varias tendencias mundiales de gran calado, desde nuevas iniciativas de gasto público hasta cambios estructurales en la tecnología y las cadenas de suministro», afirma Hart.

Hay valor más allá de las Big Tech

Global Premium mantiene un enfoque de inversión resistente al paso del tiempo.

Aumento del gasto en defensa

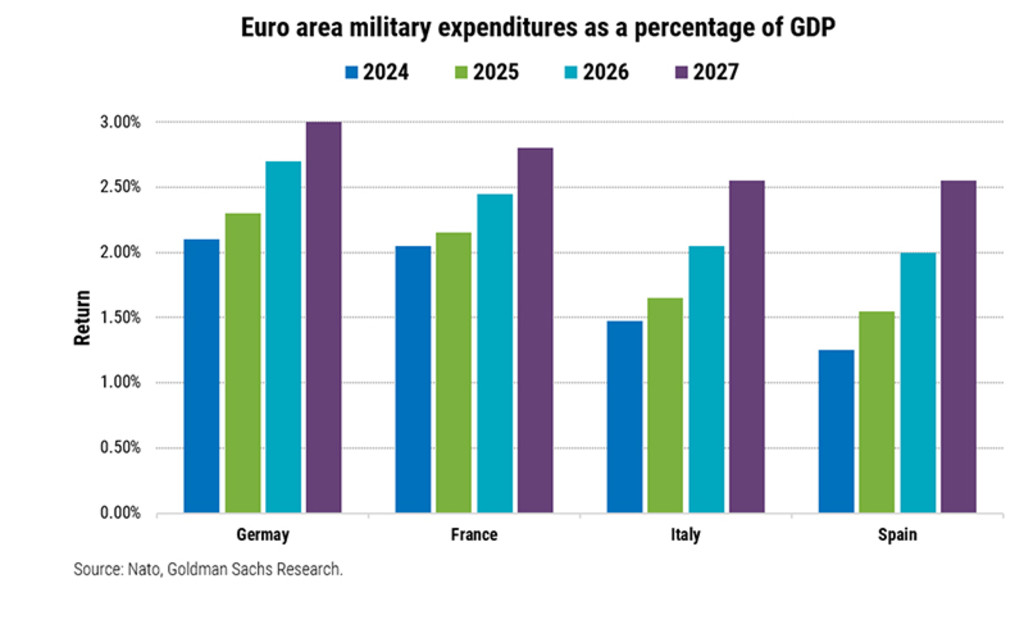

«Esto es especialmente palpable en el segmento aeroespacial y de defensa, pues se espera que experimente un gran impulso debido a la intención de aumentar el gasto militar y a un mayor estímulo a las infraestructuras. El potencial de crecimiento es significativo dada la previsión de que los gastos en "necesidades básicas de defensa" de Europa y Canadá prometidos a la OTAN aumenten del 1,7% del PIB en 2022 y del 2,0% en 2024 a un 3,5% para 2035».

«Además, un mayor gasto en equipos fabricados en Europa debería contribuir a la consolidación de los fabricantes regionales y a la creación de una demanda más duradera a largo plazo en todo el continente».

«El hecho de que Alemania haya anunciado una iniciativa de gasto de 1 billón de EUR supone un distanciamiento histórico de su tradicional conservadurismo fiscal y pone de relieve cómo está cambiando el consenso político. Están surgiendo tendencias similares en el Reino Unido y Francia, donde el apoyo bipartidista se está aglutinando en torno a la inversión en infraestructuras, defensa y tecnologías verdes».

«Este giro en las políticas públicas favorece considerablemente a los valores industriales en general, debido al nuevo respaldo financiero para proyectos que abarcan varios años y requieren bienes de capital, servicios de ingeniería y actividades relacionadas con la construcción».

Gráfico 1: Aumenta el gasto militar en las principales economías europeas

Fuente: OTAN y Goldman Sachs, noviembre de 2025

Beneficios de la IA

La implementación de la IA está impulsando tanto la oferta como la demanda de las compañías industriales. «Más allá del gasto en defensa e infraestructuras, la industria de equipos eléctricos en Europa también se está beneficiando de los motores que transforman la demanda», afirma Hart.

«La construcción de centros de datos de IA en todo el mundo está incrementando la necesidad de adquirir sistemas eléctricos avanzados a pasos agigantados, mientras que la transición a nuevas soluciones energéticas (desde la integración de renovables a la modernización de la red) está aportando una capa adicional de crecimiento duradero».

«Estas tendencias están presentando oportunidades para las compañías capaces de suministrar soluciones energéticas de alta eficiencia, componentes avanzados y tecnologías más modernas. Al mismo tiempo, la automatización y las herramientas de IA están reconfigurando las operaciones de las compañías industriales».

«Las compañías que están implementando herramientas de automatización avanzadas, optimizando procesos gracias a la IA y desplegando soluciones digitales de gestión de la cadena de suministro están mejorando la eficiencia de forma cuantificable. Estas innovaciones agilizan los flujos de trabajo, reducen las cargas administrativas y mejoran tanto los márgenes operativos como la competitividad global».

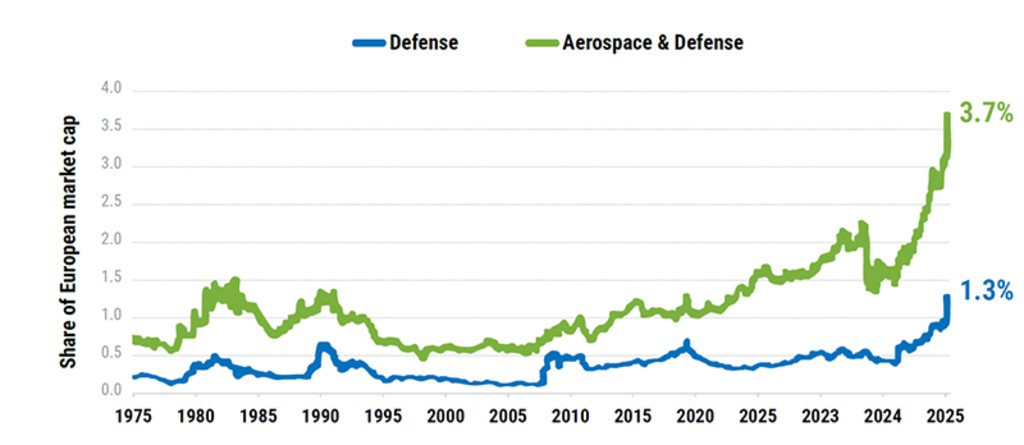

Gráfico 2: El sector aeroespacial y de defensa adquieren importancia en el mercado europeo

Fuente: Goldman Sachs Research, «Defense spending to boost German and European GDP growth», 19 de marzo de 2025

BP Global Premium Equities D USD

- performance ytd (30-6)

- 6,75%

- Performance 3y (30-6)

- 18,00%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Pago de dividendos (30-6)

- No

Rentabilidades pasadas no garantizan resultados futuros. El valor de las inversiones puede fluctuar.Anualizado (para periodos superiores a un año). Las rentabilidades son netas de comisiones, basadas en los precios de transacción.

Más elementos favorables

La resiliencia del comercio mundial, el aumento de la inversión y la buena disciplina de capital son otros elementos que resultan favorables para el sector. «El crecimiento en el ámbito industrial no se produce de forma aislada», recuerda Hart a los inversores. «El sector sigue estando estrechamente vinculado al comercio mundial, la inversión de capital y la actividad de infraestructuras, áreas que tienden a acelerarse durante los periodos de fortaleza macroeconómica».

«Creemos que esta sensibilidad cíclica, unida a elementos favorables seculares a largo plazo, sitúa al sector en una buena posición para experimentar un crecimiento a corto y medio plazo. Las iniciativas de reshoring de la cadena de suministro, la transición energética en curso y un ritmo constante de mejora de la eficiencia están potenciando la fortaleza subyacente del sector».

«Dicho esto, las políticas comerciales y arancelarias de EE.UU. siguen siendo un área que merece la pena seguir de cerca, pero los datos disponibles hasta ahora sugieren que el comercio mundial ha estado mitigando el aumento del coste de hacer negocios con EE.UU.».

En busca de valor real

Al fin y al cabo, todo se reduce a elegir los valores adecuados para una cartera de inversión. «Un importante factor diferenciador en el ámbito de los valores industriales es la eficiencia del capital», afirma Hart.

«Buscamos compañías que ofrezcan una alta rentabilidad del capital invertido (ROIC) de forma sistemática. Esto, junto con balances saneados y una sólida generación de flujo de caja, no solo confiere resiliencia financiera durante las recesiones, sino que también posibilita la inversión orgánica, una rentabilidad atractiva para los accionistas y cada vez más adquisiciones».

Hart considera que esta dinámica plantea un panorama constructivo para el sector industrial europeo, lo cual puede ser tranquilizador para los inversores preocupados por el creciente riesgo de concentración al que se enfrenta la renta variable estadounidense.

«Dadas las oportunidades de crecimiento estructural en infraestructuras defensivas y energéticas (unidas a una asignación disciplinada del capital y a posibles mejoras de la eficiencia derivadas de la automatización), creemos que los valores industriales europeos ofrecen un potencial alcista infravalorado y valoraciones absolutas atractivas».

Acceda a las perspectivas más recientes

Suscríbase a nuestro newsletter para recibir información actualizada sobre inversiones y análisis de expertos.