Strategist

• 月次アウトルック

The Achilles’ heel for the everything rally: A dollar comeback

It’s the world’s largest currency that underpins much of the world’s trade, and its recent demise has been great for markets outside the US. The dollar’s recent comeback has had many investors thinking it’s the Achilles’ heel for emerging markets and commodities, and the rally may have legs, says strategist Peter van der Welle.

まとめ

- US dollar has staged a countertrend rally since war broke out with Iran

- A rising greenback bodes badly for emerging markets and commodities

- Five reasons why the rally could continue as its safe-haven status returns

A declining dollar is great for non-US stock markets, as seen in the renaissance of European and Asian equities during 2025. And since commodities are sold in dollars, any nation selling anything from oil to soybeans gets a bigger payday in its local currency if the greenback falls in value.

“Since the start of the US military action against Iran on 28 February, we have seen the dollar stage a comeback, up 1.5% as of 5 March,” says Van der Welle, strategist with Robeco Investment Solutions and its multi-asset portfolios.

“Does this dollar bounce have legs? The answer to this is critical, as correlations show that a sustained reversal in the trajectory of the greenback could challenge continued outperformance of non-US markets and a broad segment of the multi-asset universe.”

The world’s most traded currency is still overvalued by 12% on our favorite valuation metric.

“The world’s most traded currency is still overvalued by 12% on our favorite valuation metric, its deviation from trend in relative purchasing power parity (PPP). While we believe the dollar remains in a secular bear market (which it entered in 2022), countertrend rallies are common.”

Van der Welle says that three such countertrend rallies have occurred in previous dollar bear markets, where the greenback rose at least 5% versus other currencies for an average of three months, returning an average 8.2% each time.

He says the military action against Iran could set the stage for another countertrend rally, which would upend the ‘everywhere rallies’ seen in Europe, Asia and in commodities.

“First, positioning and flow dynamics favor a dollar bounce against the backdrop of elevated tensions in the Middle East,” he says. “Asset managers went into the conflict with a historically large underweight position in the dollar; the flip side of this is that they had historically overweight positions in emerging market equities.”

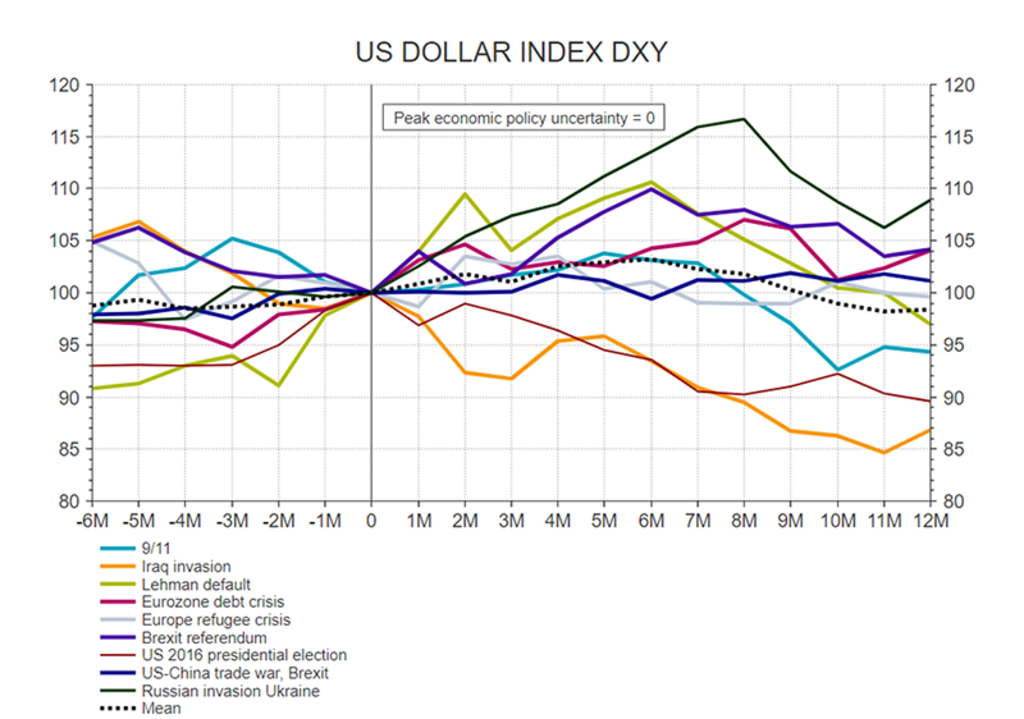

“This makes investors more vulnerable to be on the wrong side of the trade. The longer Middle East tensions last, the larger the scramble for liquidity becomes, favoring the dollar, as it is involved in 89% of global FX transactions. We find that the trade-weighted dollar tends to strengthen in the 3-6-month window after big geopolitical events.”

Figure 1: How the dollar deviates during big events

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: LSEG Datastream, Robeco, March 2026.

“Second, as bombs flew over Iran in a show of US hegemony, the dollar turned positive. Its positive correlation with the VIX volatility index, which was notably absent in the immediate aftermath of President Trump’s so-called ‘Liberation Day’ last year, returned. As such, the dollar is dusting off some of its lost appeal as a safe haven.”

The US versus Europe

The third reason is more technical as it relates to interest rate differentials against the euro, the world’s second-largest traded currency. Currently the US base rate set by the Fed is 3.5%-3.75%, with the likelihood of further rate cuts in 2026, while the ECB rate is 2.15%-2.40%, and is not seen falling further. This favors inflows into the dollar, particularly if the Middle East war raises energy prices, and therefore inflation, making the ECB even less likely to cut rates.

“On our metric, the dollar is around 3 cents too cheap versus the euro when looking at two-year rate differentials between the US and the Eurozone,” Van der Welle says. “Also, risks to an ongoing expansion of the Eurozone (to the former Yugoslav states) have become more skewed to the downside in the wake of the Iran war. A recognition of the ECB’s unwillingness to hike could therefore contribute to dollar strength.”

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

With Europe being more susceptible to an oil price shock, growth differentials could further favor the dollar.

Then there are GDP growth differentials between the US and Eurozone. “The dollar has recently significantly undershot the difference between US and German industrial production data,” Van der Welle says. “With Europe being more susceptible to an oil price shock, as it is a net importer whereas the US is a net energy exporter, growth differentials could further favor the dollar.”

Don’t forget the midterms

And finally, there is good old-fashioned political motivation, with the midterm Congressional elections due in November – polls which are always seen as a referendum on the incumbent president’s popularity.

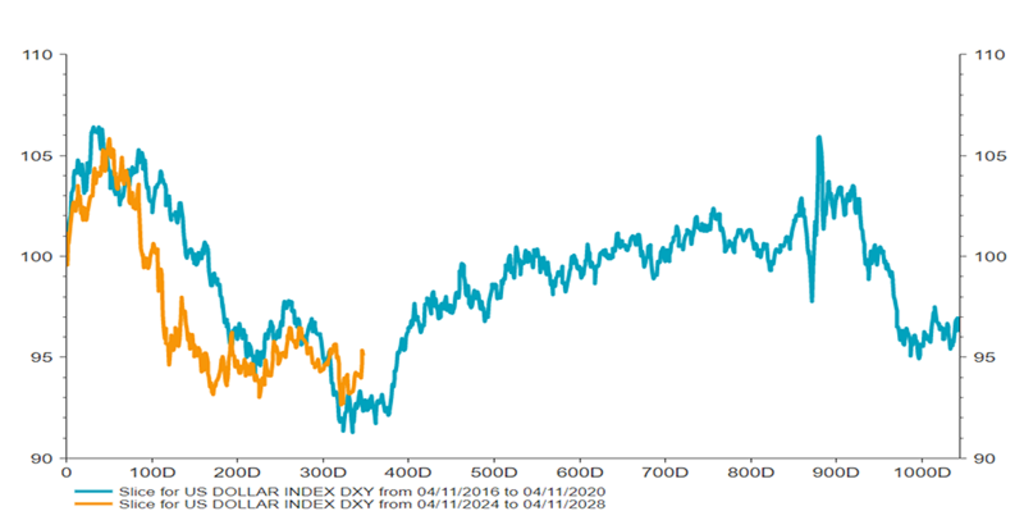

“During the second Trump presidency, we have so far seen a remarkable alignment of the dollar with its evolution during the first from 2017-2021,” Van der Welle says. “If the future were to rhyme again with the playbook of the first Trump administration from here onwards, we could be very close to a strengthening dollar, as seen in the chart below.

Figure 2: The dollar during Trump’s first and second presidencies

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: LSEG Datastream, Robeco, March 2026

“A temporarily stronger dollar could be welcomed as the November midterm elections draw closer. A stronger dollar – while exerting a tightening effect on US export growth – would lower import inflation and therefore potentially mitigate the affordability crisis through real disposable income growth, appeasing part of the Republican electorate.”

So, can it last? “While we think that turmoil in the Middle East as things stand will not derail the prospect of a synchronized global cyclical upswing, the risks to our base case of the Synchronized Shift that we predicted in our 2026 outlook have become more asymmetrical,” Van der Welle says.

“We expect the market to become more perceptive to the asymmetries surrounding the dollar. If the Iran war has indeed kickstarted a temporary revival of the dollar, we have only digested some 20% of a typical countertrend rally. More may be yet to come.”

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会