Head of Multi Asset & Equity Solutions, Co-Head Investment Solutions

• 月次アウトルック

Tariffs retaliation – the markets bite back

It’s been the expected explosive start to the second Trump presidency, but he will have been reminded of forces more powerful than presidential authority – the markets. And that could serve to neutralize the impact of tariffs and any trade war, says multi-asset investor Colin Graham.

まとめ

- Tariffs cause US equities, bonds and currency to fall at the same time

- Conversion of dollars held overseas into local assets more likely

- Investors will question the premium now needed to hold US assets

All the major asset classes tanked on the tariffs news, though the biggest shock came with a trillion-dollar sell-off in the US Treasury market – by far the largest bond market in the world. This move by the ‘bond vigilantes’ prompted the White House to water down or postpone much of the tariff plans.

And now the US economy itself is threatened by the self-defeating mantra of trying to correct trade imbalances with taxes on imports that will only dampen consumer demand and import inflation, says Graham, co-head of Robeco Investment Solutions.

The art of the deal?

“From our vantage point, President Trump is not following his own mantra of the art of the deal,” Graham says. “He blinked when the bond vigilantes emerged from hibernation, and is now folding as his bluff was called by friends and foes alike. The climbdown over tariffs will continue, but the negative macro impact on the US will start to emerge.”

“The consumer and manufacturing survey data has been poor, though the actual spending or labor data has yet to be affected. There is evidence that US consumers are pulling spending forward, and that companies have been stockpiling before the tariffs hit.”

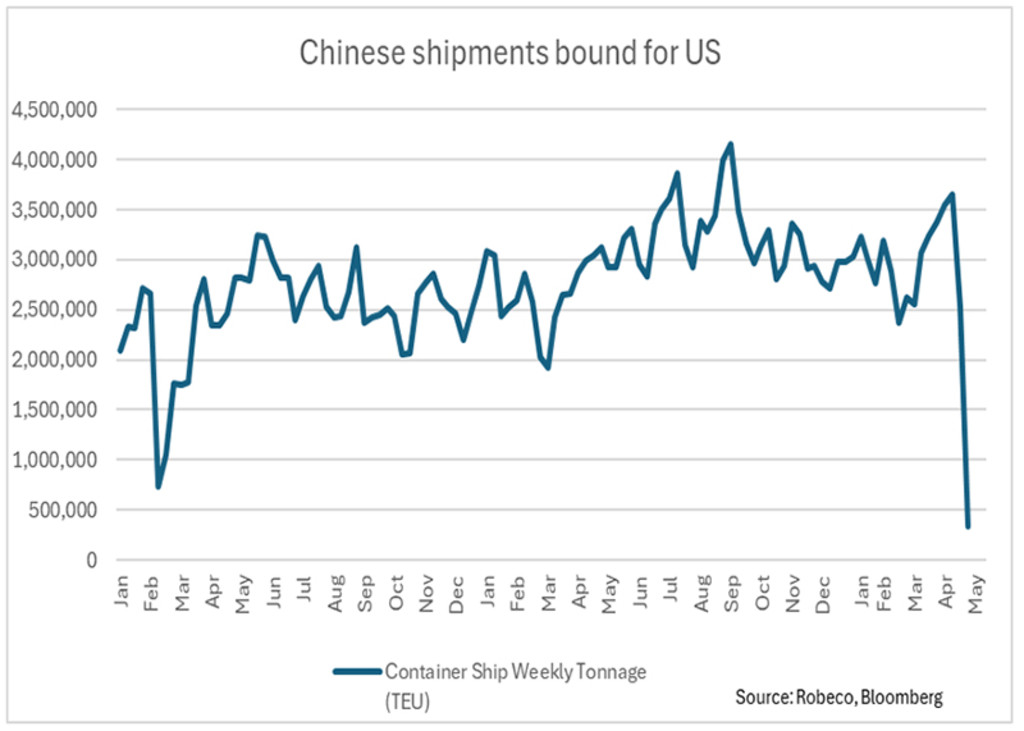

“As a consequence of the tariffs, shipping volumes from China have ground to a halt. The most recent parallels can be drawn with the supply shock of the 2020 pandemic, as goods became scarce and inflation skyrocketed.”

Figure 1: Container ship volumes: shipments bound for the US from China have fallen off a cliff

Source: Robeco, Bloomberg

Upending the world order

The first major casualty of the new regime has been a significant weakening of the US dollar, and its role as the global reserve currency that is normally highly prized by foreigners. Its historic strength has largely allowed the US to fund its huge budget and trade deficits.

“Reversing this system could have dire consequences for the US and global economy,” Graham says. “Since the tariff announcements, the US economic outlook has been universally downgraded, coupled with everyone scrambling to understand the extreme policy uncertainty.”

“Non-US investors are now questioning the required risk premium for holding US assets. This is the USD 32 trillion question (the size of foreign portfolio holdings), which means the retaliation may come from different avenues.”

Reactions of asset classes

This retaliation has major implications for all asset classes, Graham says: “We came into the year with the dollar significantly overvalued compared to history as superior growth, higher interest rates and capital inflows drove it ever higher. Over the longer term, we expect a derating and rebalancing.”

“The downward pressure from a ‘buyer’s strike’ would be extended if investors do not allocate more assets to the US. Meanwhile, the repatriation of export proceeds from the US, allowing local currencies to appreciate against the dollar, means tariff policies are likely to continue to be watered down.”

“We have already seen central banks and individuals increasing dollar diversification through gold and other FX holdings. Going forward, we question whether US interest rate and growth rate dominance over the rest of the world will be enough to retain the attraction of US capital.”

“While the reduction of overweights to US assets by foreigners is a slow burn, this could speed up, as investors and corporates accelerate the de-dollarization process.”

Impact on Treasuries

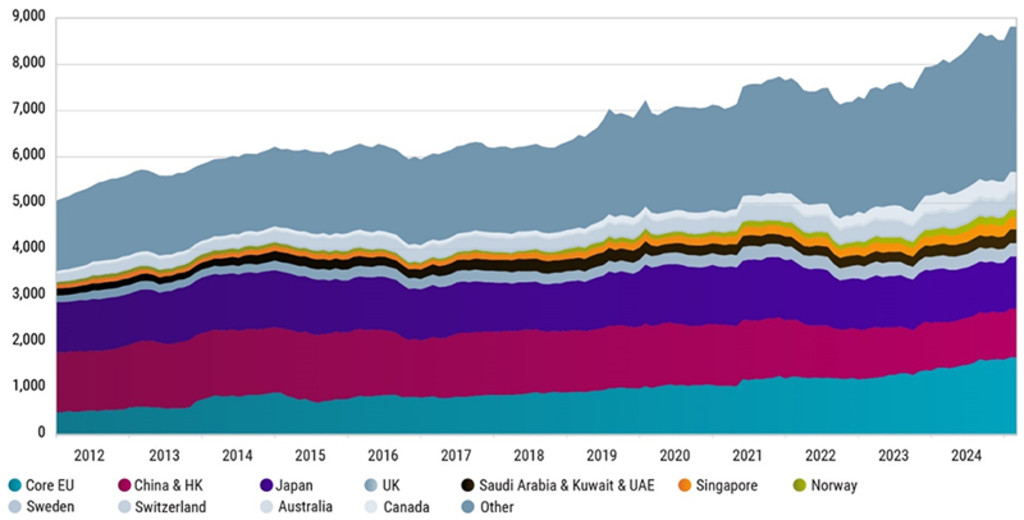

The biggest impact may be seen in US Treasuries, USD 9 trillion of which are owned by overseas actors, including China. The so-called bond vigilantes have been dumping them on the open market, forcing yields up and values down.

Figure 2: Foreign ownership of US Treasuries is huge

Source: US Department of Treasury, Robeco

“A reduction in trade will provide less incentive to hold proceeds in dollars, and the conversion of dollars held overseas into local assets becomes more likely,” Graham says. “China has been increasing its pile of US Treasuries held in the Euroclear system, thereby making it easier to switch to European bonds and avoid driving the renminbi up against the greenback.”

“We remain neutral on the duration of Treasuries as the US economy remains robust, but will be looking to add to holdings if yields rise, because the inflationary impact of the goods shortage is not yet priced in, and the risk (term) premium for holding US Treasuries should be higher.”

Outlook for earnings and equities

There are also implications for equities, not least in how any remaining tariffs cut into company earnings, at a time when many investors believe that the tech-dominated US stock market is overvalued, even after the recent correction.

“Previously, non-US investors had a cushion against any risk-off move lower in equities from a rising US dollar,” Graham says. “In the latest equity sell-off, European investors were hit with the double whammy of declining US equity prices and a falling US dollar.”

“Toward the end of 2025, it will be clearer where the additional costs of tariffs will be borne. We expect to see the cost split between corporate margins and price increases for consumers. This will impact US equity multiples, which are already expensive, and keep consumer inflation sticky.”

Murky guidance

“In this state of the world, the outlook for employment and capital expenditure intentions will significantly impact investors’ expectations. Currently, US employment data is strong, while companies’ earnings guidance has become murky to non-existent.”

“We remain hyper-vigilant on the changing landscape, currently maintaining defensive positions in portfolios.”

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会