Portfolio Manager

• 月次アウトルック

The strange case of Dr Equity and Mr HY-de

A rare disconnect between the likely performance of equities and high yield bonds means stocks will be greatly preferred going into 2026, says multi-asset investor Mathieu van Roon.

執筆者

主なキーワード

まとめ

- Equities and high yield bonds are normally on the same side of the risk coin

- Stocks are expected to see robust earnings growth in a positive macro backdrop

- HY bonds face rising credit stress, a demand imbalance and super-tight spreads

He says the different sides offered by what is usually the same risk-on or risk-off trade draws a parallel with the gothic horror story ‘The Strange Case of Dr Jekyll and Mr Hyde’. In the 19th century tale, the mild-mannered scientist Dr Jekyll drinks a potion and turns into the monstrous Mr Hyde. Both are the same man, but with very different sides.

“As we near the end of the year and start to look ahead to 2026, we see a clear bifurcation in the downside versus the upside risks between equity and equity-like asset classes,” says Van Roon, Portfolio Manager with Robeco Investment Solutions.

“Whereas normally we expect high yield bonds and equities to be on the same side of the risk on/off coin, and to perform in the same type of circumstances, for 2026 we fear high yield could show its ugly side. You might call it the Strange Case of Dr Equity and Mr HY-de.”

Van Roon says the bifurcation lies in the macroeconomic factors facing each asset class that will turn out positive for Dr Equity and negative for poor Mr HY-de. “On the one hand, US and European equity markets and large investment grade corporates are full of optimism, fueled by robust earnings, aggressive buybacks and the promise of AI-driven productivity gains,” he says.

“On the other hand, the real economy – especially in the US – and leveraged high yield issuers are burdened by deteriorating fundamentals and increasing macro risks.”

“This dichotomy in views on the asset classes is striking, as historically, high yield bond and equity prices have had a strong correlation, with both dependent on positive economic and company growth expectations.”

“But in 2026, the macro and technical environment might worsen for high yield, whereas equity has a bigger chance to continue to ride the wave of earnings strength and technological optimism, similar to the last throes during the tech bubble of the late 1990s.”

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

Growth from spending and AI

The giant economies of both the US and Europe are expected to grow in the coming year, though for different reasons. Europe’s growth is related to fiscal spending, including on defense and infrastructure, and pent-up savings. The growth expectation in the US is driven by AI-related capital expenditure, and potential productivity gains from AI and upper-income consumption. This is further aided by fiscal support from the One Big Beautiful Bill Act and bumper tax refunds.

“This growth is, however, not without tension,” Van Roon warns. “President Trump’s tariffs are expected to impact US growth and/or company earnings, while inflation is expected to remain sticky. The Fed is in a tough position to remain either too restrictive in an already fragile labor market, or to potentially start too soon with easing, which could un-anchor inflation expectations.”

“Add to that political uncertainty with mid-term elections coming up in November 2026, and a potential change at the Fed’s helm when Chairman Jerome Powell’s term ends in May. The aforementioned AI boom is also expected to continue to reshape the labor market, as fewer people are needed to produce the same output.”

“These developments can impact consumer spending negatively. Alternatively, efficiencies will lead to more leisure time; Henry Ford used the efficiency of car assembly lines to allow workers the concept of a ‘weekend’, in the belief that this would boost car usage and adoption.”

Dr Equity

Given this backdrop, Van Roon says US equities are expected to benefit from robust earnings growth, seen at about 14% for the S&P 500, with half of that coming from sectors outside the tech sector. EU companies stand to gain as well, due to fiscal stimulus and the broadening of growth beyond the US. The AI productivity gains are expected to broaden out over the other sectors, such as healthcare and retail, thus supporting the rally.

“Current valuations are high, but thanks to strong company fundamentals (margins, free cash flows, low leverage levels), they are not at extremes,” Van Roon says. “Last but not least, the flows into equities remain robust and diversified, with retail, passive and institutional investors across the spectrum continuing to buy stocks.”

Mr HY-de

This contrasts quite starkly with the high yield bond market. “Whereas the outlook for equities is rather optimistic, the outlook for high yield is much more cautious,” Van Roon says. “Compared to large investment grade companies, the lower-rated, smaller and more highly leveraged companies are struggling with tighter lending standards and rising refinancing rates.”

“The macro landscape with more political/tariff/inflation uncertainty and AI-related job cuts is expected to weaken consumer demand, which these types of companies rely on.”

“Supply-wise, a net increase is expected, driven by AI-related capex, M&A and refinancing, whereas it is expected that inflows are unlikely to keep pace with this supply. Recent worries about rising stress in private credit might spill over into public high yield markets, especially if sector-specific shocks (such as AI disruption in software) trigger a negative feedback loop, where bonds with lower ratings such as B or CCC are more vulnerable.”

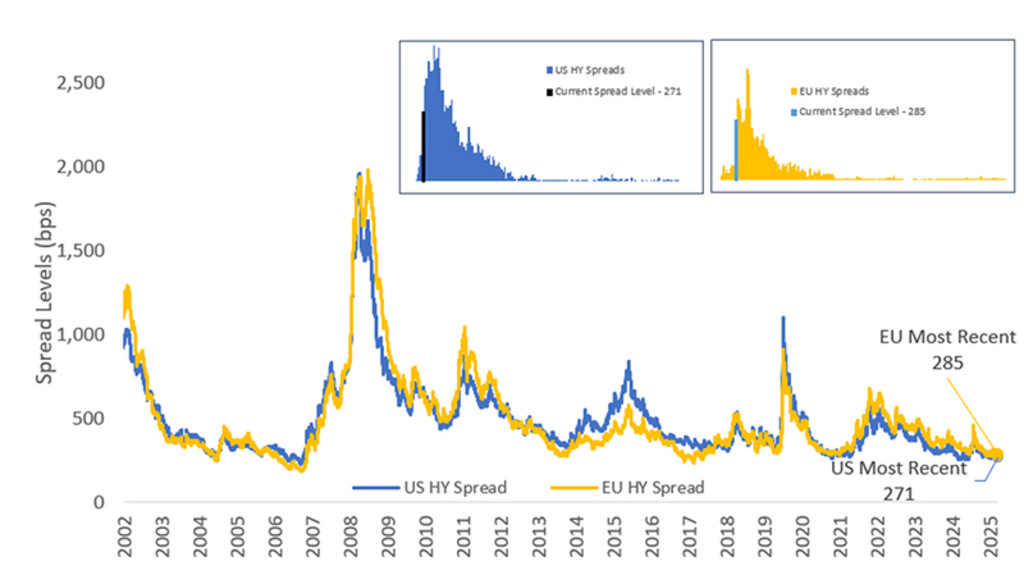

“Just as in equities, current valuations in high yield are rich, as spreads are hovering around historically low levels.” This can be seen in the chart below.

Figure 1 – Historic high yield spread development

Source: Bloomberg, Robeco

Brighter outlook for stocks

“Investors are not asking for much additional compensation to invest in high yield bonds. While further spread tightening is possible, it is relatively limited. The attractiveness of this asset class is thus mostly the sizeable carry returns gained from holding these bonds.”

In all, Van Roon says the trade-off between risk and returns is much more constructive for equities than for high yield. “The tight spreads, rising supply and challenging macro environment make us more cautious for high yield, but the asset class can still deliver attractive carry returns going forward, especially relative to other fixed income sectors,” he says.

“Equities stand to benefit from fiscal support, AI-driven earnings and robust flows, and have more upside. We thus take sides with ‘Dr Equity’.”

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会