16:00 CET

Multi-Asset: Una tregua provvisoria

Di Peter van der Welle, Stratega Multi-Asset

Dopo una settimana turbolenta, che ha visto il presidente degli Stati Uniti Trump esercitare una pressione verbale senza precedenti sul regime iraniano, si sta delineando una tregua. Tuttavia, l'Iran mantiene saldamente il controllo della dinamica di escalation. Secondo quanto riportato, solo poche navi hanno attraversato lo Stretto di Hormuz da quando la tregua è entrata in vigore alle 20:00 ora della costa orientale dell'8 aprile. La chiusura effettiva dello Stretto di Hormuz comporta comunque una perdita di approvvigionamento stimata in otto milioni di barili al giorno, creando un divario significativo tra ciò che i rilasci dalle riserve strategiche di petrolio possono realisticamente compensare e ciò che si sta perdendo durante il trasporto. Anche ipotesi ottimistiche sul rilascio delle riserve e sul reindirizzamento saudita via Yanbu (circa sette milioni di barili al giorno) coprono solo una frazione dei normali flussi abituali attraverso Hormuz (circa quindici milioni di barili al giorno, pari a circa il 15% dell'offerta globale).

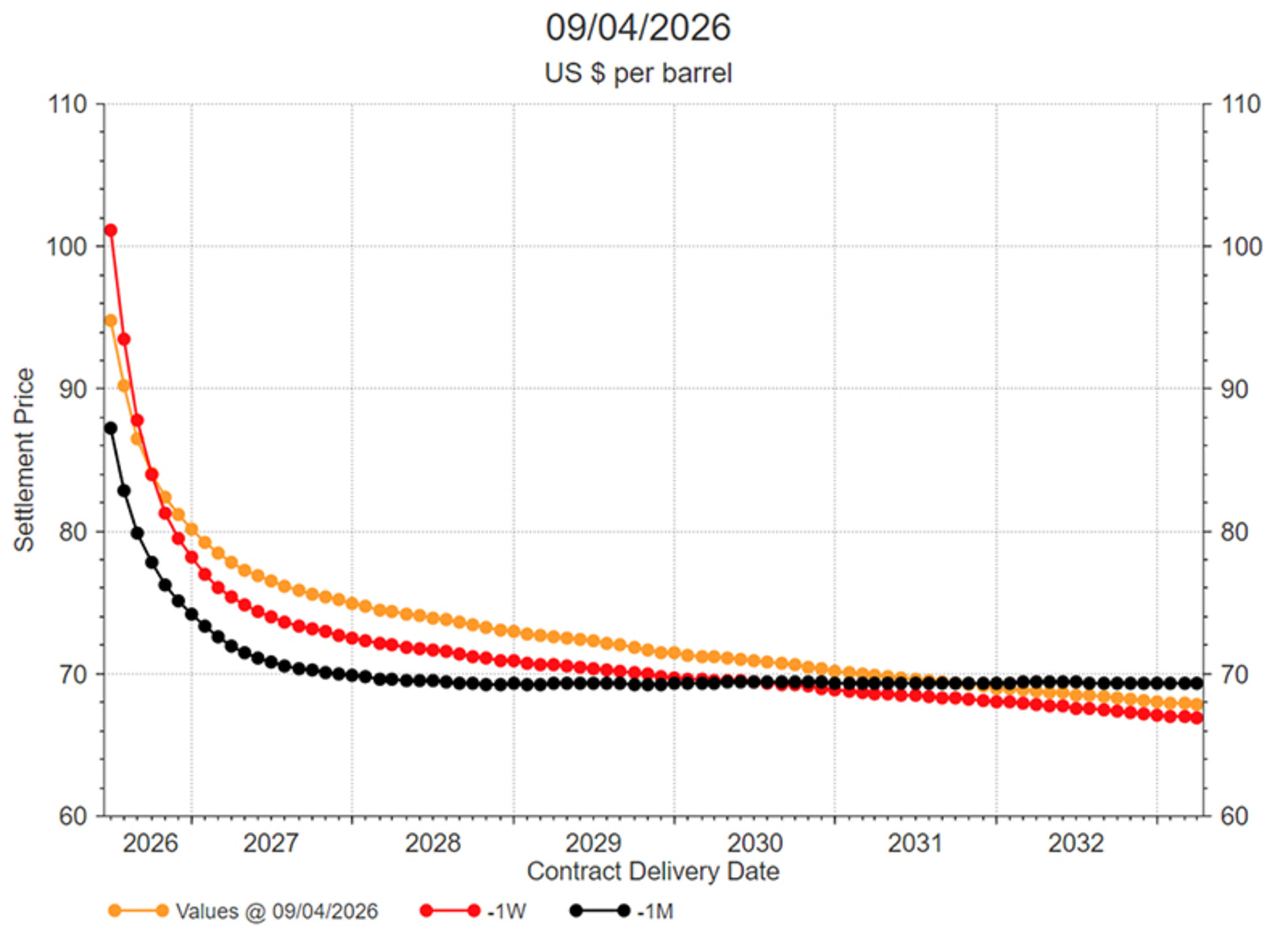

Le curve dei futures sul petrolio sono in forte backwardation, il che implica che il mercato petrolifero si aspetta ancora che la durata di questo conflitto sia breve, con i prezzi spot significativamente superiori ai prezzi dei contratti con scadenze più lontane. Mentre il Brent con consegna immediata viene scambiato a 126 dollari al barile, il contratto con scadenza dicembre 2026 viene scambiato a ottanta dollari al barile.

Fonte: LSEG Datastream, Robeco

Con il cessate il fuoco, abbiamo probabilmente superato il picco di incertezza politica

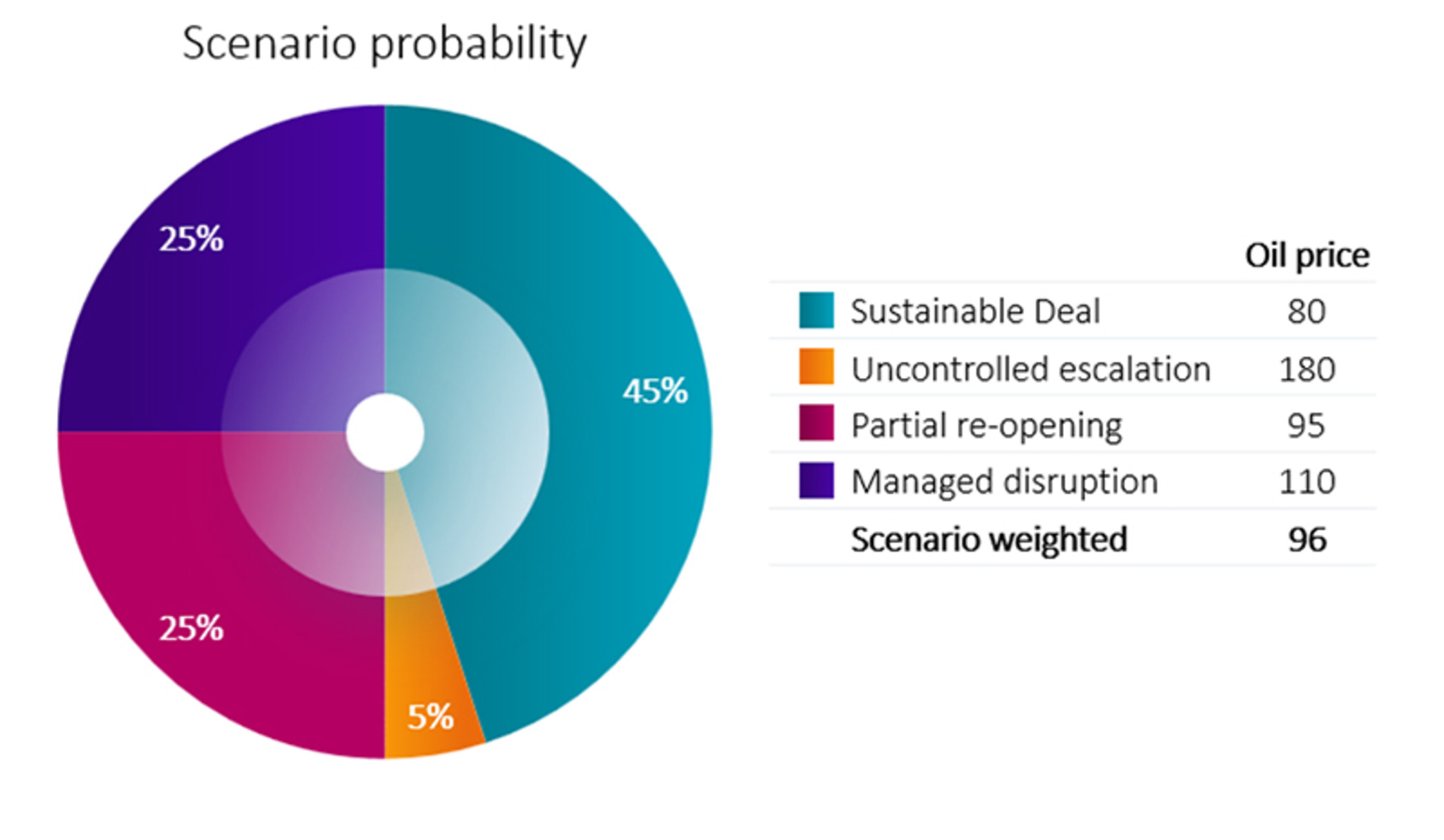

Il fatto che sia stato stabilito un cessate il fuoco per le prossime due settimane ha chiaramente spostato la massa di probabilità da un'escalation incontrollata verso scenari meno ribassisti (vedi il nostro grafico a torta "Scenario probability"). Questa significativa riduzione del rischio al ribasso è il segnale che il mercato stava aspettando. I mercati vogliono davvero lasciarsi alle spalle questo conflitto. Le azioni tendono a registrare un rialzo dopo il picco di incertezza politica e le minacce dal tono apocalittico rivolte dal presidente Trump all’Iran la scorsa settimana hanno probabilmente rappresentato il picco di incertezza politica per questo conflitto.

Fonte: Robeco, aprile 2026.

Sebbene i mercati abbiano reagito sottotono rispetto al livello prevalente di rischio geopolitico, la volatilità implicita dell'S&P 500, un importante barometro del rischio, ha superato quota trenta su base intraday la scorsa settimana. Dal punto di vista dei mercati, la storia suggerisce che i picchi del VIX sopra quota trenta tendono a generare alti rendimenti azionari su un orizzonte di 3-12 mesi.

Ciò crea una tensione tra i rischi al ribasso a breve termine derivanti dalla stagflazione guidata dall’energia e l’elevata percentuale di successo, storicamente, dei rendimenti azionari positivi dopo gli shock di volatilità. Finché l’inflazione rimane al di sotto del 4%, in genere ci troviamo ancora in una fase favorevole per le azioni. Un rialzo duraturo richiede probabilmente un allentamento del rischio geopolitico (una riapertura sostenuta, anche se parziale, dello Stretto di Hormuz) insieme alla conferma che gli effetti secondari dell'inflazione rimangano contenuti, consentendo alle banche centrali di guardare oltre il picco iniziale dell'inflazione complessiva.

Eppure, si naviga ancora nella nebbia di guerra

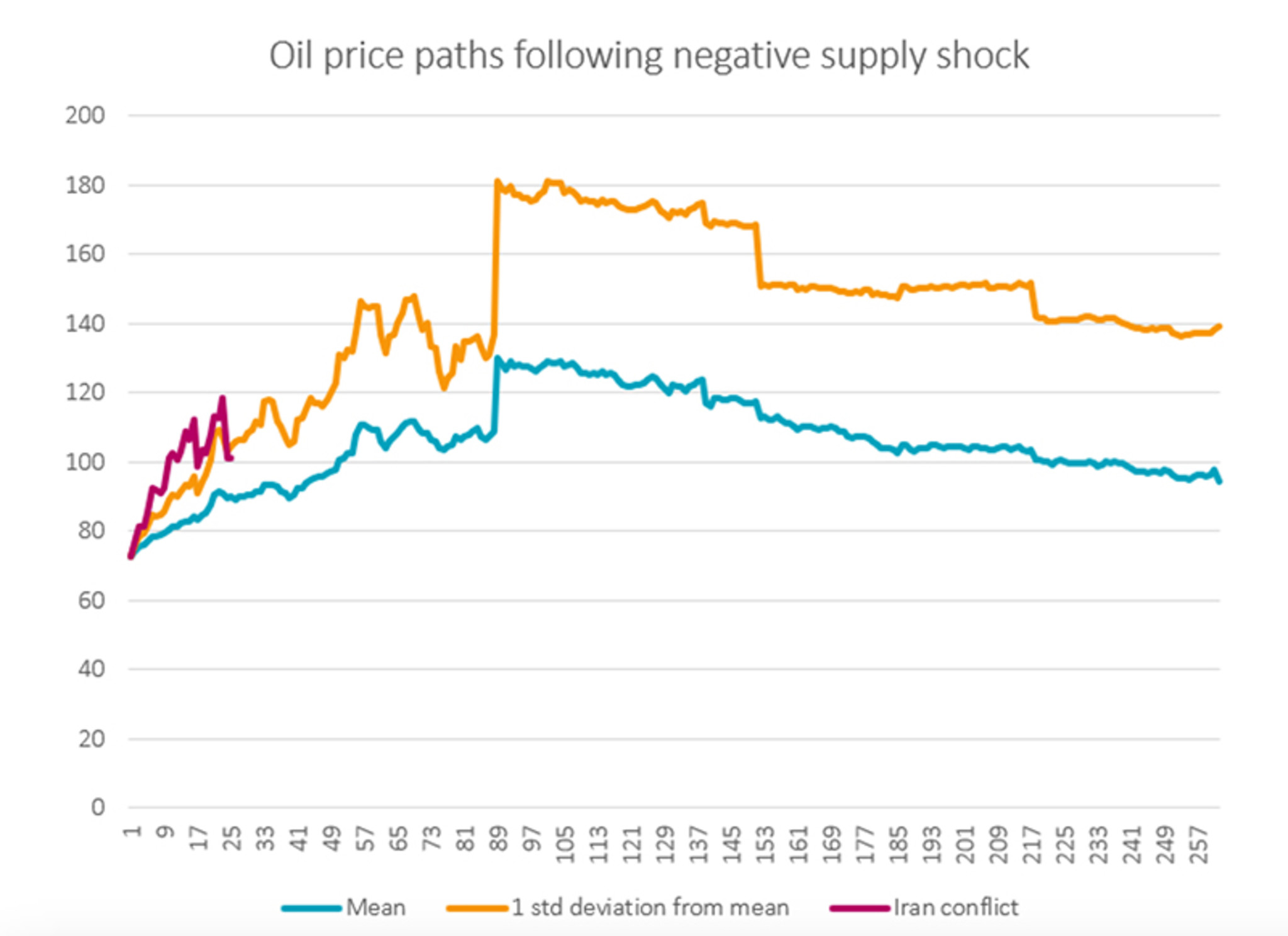

L'ottimismo del mercato riguardo a un previsto calo dei prezzi del petrolio nel corso dei prossimi mesi potrebbe essere messo in discussione. Osservando l'andamento storico dei prezzi a seguito di shock negativi sull'offerta nel mercato petrolifero, si nota che i prezzi tendono a scendere solo dopo un periodo compreso tra i 100 e i 150 giorni dall'inizio di un conflitto. Al momento della stesura di questo articolo, sono trascorsi 41 giorni dall'inizio del conflitto. Dalla letteratura geopolitica sappiamo inoltre che i cessate il fuoco sfociano in accordi solo nel 15-25% dei casi (cfr. Clayton et al. 2022, Journal of Conflict Resolution). Sebbene si tratti di un rischio estremo nel nostro scenario, un’escalation incontrollata rimane una possibilità concreta. L’Iran controlla un importante snodo strategico e il tempo gioca a favore degli iraniani, con un presidente degli Stati Uniti alle prese con le elezioni di medio termine. Massimizzare la propria influenza sullo Stretto di Hormuz consente all'Iran di ottenere il miglior accordo possibile per il piano in 10 punti che ha presentato come modello per i negoziati a Islamabad nelle prossime settimane. Ma si tratta anche di una strategia ad alto rischio, con il numero delle truppe statunitensi in Medio Oriente destinato ad aumentare nelle prossime settimane, dato che è previsto l'arrivo nel Golfo di nuove navi della marina statunitense. Pertanto, una minaccia persistente per il trasporto marittimo lascerebbe spazio a premi per il rischio più elevati nei prezzi del petrolio. Nel nostro scenario di escalation incontrollata prevediamo che i prezzi del Brent raggiungano i 180 dollari al barile. Questo livello corrisponderebbe a una deviazione standard dal picco medio del prezzo del petrolio osservato in precedenti shock negativi dell'offerta. Sia i trasportatori di petrolio che gli investitori devono navigare nella nebbia di guerra.

Fonte: LSEG Datastream, Robeco, aprile 2026. Gli eventi includono la guerra dello Yom Kippur, la rivoluzione iraniana, la prima guerra del Golfo, le restrizioni dell'OPEC sull'offerta, lo sciopero petrolifero in Venezuela, le interruzioni in Iraq/Nigeria/Venezuela, la Primavera araba e l'invasione russa dell'Ucraina.