• 5 年展望

Secular stagnation is a stagnating theory

Is secular stagnation for real? Although a number of arguments for it hold water, their influence has diminished, says Lukas Daalder in Robeco’s new five-year outlook.

概要

- Fears re-emerge of breakdown between savings and investments

- Factors from tech to aging can cause secular stagnation in theory

- Long-term solution would be tighter labor market and higher wages

The phenomenon occurs when a range of factors cause a breakdown in the relationship between savings and investment, and hasn’t been seen since the ‘lost decade’ in Japan in the 1990s. Left unchecked, it leads to economic stagnation.

“If secular stagnation really exists, the current economic rebound will only be a temporary episode; a mere blip, forgotten by next year,” says Daalder in Expected Returns 2018-2022. “If this is the case, bonds will continue to surprise positively, while risky assets will become vulnerable.”

“If, on the other hand, the whole thing is a misconception based on an unfortunate string of cyclical headwinds rather than a structural phenomenon, the opposite will apply. Assessing the case of secular stagnation is therefore worthwhile, especially in a five-year context.”

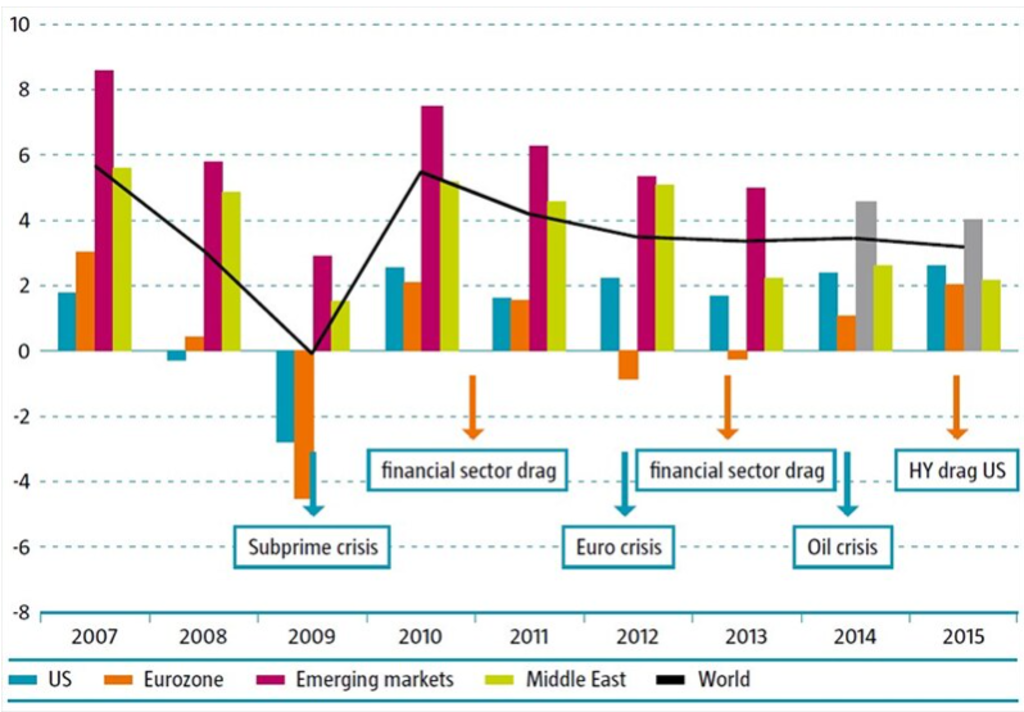

Is secular stagnation just a string of unfortunate mishaps? Source: Robeco, IMF

So what is secular stagnation? The main symptom is that there is a mismatch between investments (too low) and savings (too high), which leads to too-low interest rates and ongoing low growth. The potential causes include a lack of technological progress, aging, inequality, globalization and monetary policy.

“Not all these arguments seem to be very compelling,” Daalder says. “Take technical progress, for example. Sure, a structural decline in profitable investment opportunities can cause lower investment and higher savings. However, given the continued rise in disruptive technological developments such as blockchain, driverless cars and DNA sequencing, it is hard to see that there is a lack of technological progress.”

“Other causes have certainly played a role, but are likely to decline in the years to come. The US and European banking sectors were seriously damaged following the financial crises, when banks were no longer properly relocating savings towards investment. It is clear that banks have been strengthened in the intervening period, meaning that this factor will decline.”

獲取最新市場觀點

訂閱我們的電子報,時刻把握投資資訊和專家分析。

Aging and inequality

“Another issue is central bank policy. As excess saving (high demand for AAA-bonds) prevails, it is counter-logical to find central banks aggravating the shortage of safe assets through large-scale bond-buying programs (QE). But with the Fed raising rates and the ECB leaning towards tapering, this factor should become less important in the years ahead.”

It is not all good news though, as other factors are more structural, Daalder warns. “Take aging. Older people usually save more while companies faced with a dwindling labor force invest less. However, savers eventually enter the ‘decumulation’ phase of dissaving when they retire. Aging is not going away, even though the excess saving is set to decline once more people move to the decumulation phase.”

“Inequality is another factor. Richer people save a bigger chunk of their income than those with lower pay. The more unequal a society is, the lower the propensity to spend will be. Although we are still waiting for concrete policy measures of the US government, it seems fair to assume that it will not be a policy towards a more equal income distribution.”

Wages may be a solution

So, what’s the answer? “In all, secular stagnation is a complex concept which is further amplified by the high level of globalization and interconnectivity of modern-day markets, both financial and otherwise,” says Daalder.

“The most direct ‘natural’ solution seems to be a tighter labor market that pushes wages up, as this would end the decade-long period of disinflation, creating room for more consumption, and prepare the ground for a labor-saving investment boom.”

This article is a summary of one of the five special topics in our new five-year outlook.

Important information

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.