クオンツ債券共同責任者、リード・ポートフォリオ・マネジャー

• インサイト

Ten years of successful factor investing in credit markets

A decade of live track-records shows that our factor-based credit investing approach delivers improved risk-adjusted returns compared to the market. Here’s our story.

まとめ

- Ten-year live track record shows strength of factor credits strategies

- Systematic approach enables style diversification and more sustainability

- Multi-factor credit selection performed well across market environments

Evidence from our ten years of live factor-based credit investing, combined with more than twenty years of research and innovation in this field, shows that our approach provides improved risk-adjusted returns relative to the market, performance resilience, style diversification and greater levels of sustainability compared to passive and fundamentally managed credit portfolios.

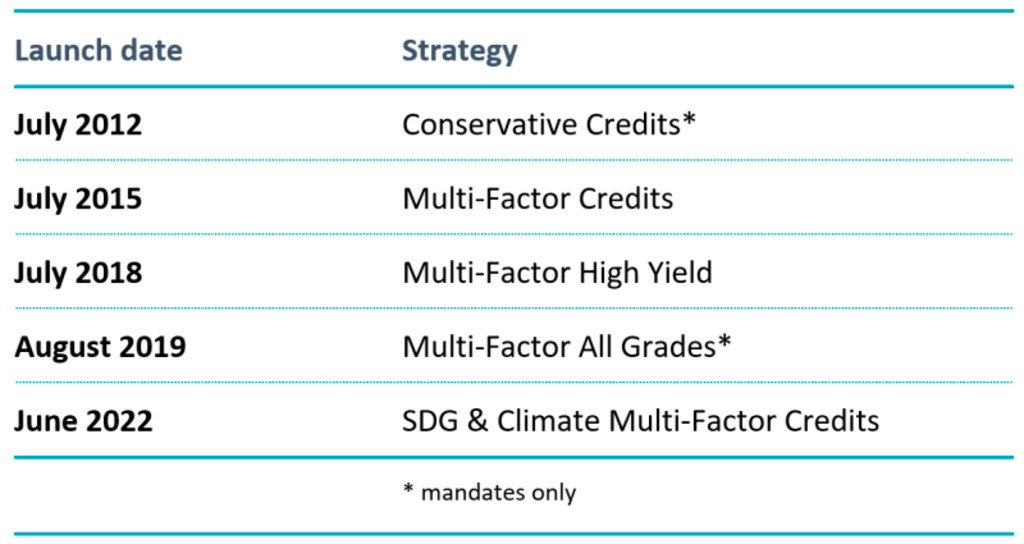

Our first standalone factor credit portfolio was launched a decade ago, in 2012. Today, Robeco’s factor credits capability oversees nearly EUR 5 billion in assets under management, across 15 live portfolios.

Robeco has been actively researching the existence of factors in credit markets since the late 1990s. With the growth in European credit markets at the time, it was a natural step to investigate the efficacy of equity factors like value and momentum in credits, too. The research resulted in an academic publication in The Journal of Portfolio Management in 2001 titled “Successful Factors to Select Outperforming Corporate Bonds”.

A number of academic contributions followed in the subsequent period and then, in 2017, we published a ground-breaking paper which was the first to document how portfolio managers can successfully implement a multi-factor approach in their credit portfolios.1

Initially, factor-based credit selection models were used as idea generator for Robeco’s fundamental credit mandates. This changed in 2012, when we won the first external mandate for factor credits. The mandate was from an insurer, to build a conservative multi-factor portfolio that reduces the credit volatility while maintaining market-like returns.

The introduction of our first multi-factor credits fund in 2015 and our first high yield-focused multi-factor fund in 2018 were further milestones, followed in 2019 by a mandate to apply factor credits to both investment grade and high yield in one portfolio. This year we launched a sustainable version of the multi-factor credits flagship fund, which contributes to the Sustainable Development Goals (SDGs) and is aligned with the Paris Agreement.

Table 1 | Launches of factor credits strategies

Tracking the live performances of our factor credit strategies

Our factor-based credit portfolios have provided superior risk-adjusted returns compared to the market. Importantly, our live portfolios have achieved results similar to those in the original empirical research, pointing to the robustness of our research as well the execution in live portfolios.

The Robeco Conservative Credits strategy, which is tilted to safer bonds from safer issuers, has realized 48 bps annual outperformance relative to its risk-adjusted benchmark,2 with a Sharpe ratio of 0.76 compared to 0.50 for the benchmark.

Robeco Global Multi-Factor Credits realized 45 bps annual outperformance, with a Sharpe ratio of 0.36 compared to 0.25 for the benchmark, and an information ratio of 0.70. In 2022 to date, which marks yet another volatile period, the strategy has outperformed by 51 bps.

Robeco Global Multi-Factor High Yield has lagged by 31 bps annually, with a lower Sharpe relative to the benchmark, at 0.20 vs. 0.25. The strategy lagged in 2020, but has been recovering ground since. The strategy performed in line with its benchmark over the current year to date.

Robeco Global Multi-Factor All Grades has outperformed by 82 bps per annum with a Sharpe ratio of 0.19 versus 0.06 for the benchmark. In 2022 to date, the strategy has outperformed by 49 bps.

Performances until the end of April 2022. The currency in which the past performance is displayed may differ from the currency of your country of residence. Due to exchange rate fluctuations the performance shown may increase or decrease if converted into your local currency. The value of your investments may fluctuate. Past performance is no guarantee of future results. Returns are gross of fees, based on gross asset value. All figures in EUR. In reality, costs (such as management fees and other costs) are charged. These have a negative effect on the returns shown. Robeco Conservative Credits is based on a Robeco Euro Conservative Representative Mandate and benchmarked against the risk-adjusted Bloomberg Euro Aggregate Corporates index. Robeco Global Multi-Factor Credits is based on Robeco QI Global Multi-Factor Credits IH EUR share and benchmarked against the Bloomberg Global Aggregate Corporates index (hedged to EUR). Robeco Global Multi-Factor High Yield is based on Robeco QI Global Multi-Factor High Yield IH EUR share and benchmarked against the Bloomberg Global High Yield Corporates ex Financials index (hedged to EUR). Robeco Global Multi-Factor All Grades is based on a representative mandate and benchmarked against a Custom Bloomberg Global Credit incl HY benchmark (hedged to EUR). The inception dates for each strategy are shown in Table 1.

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

Demonstrated style diversification

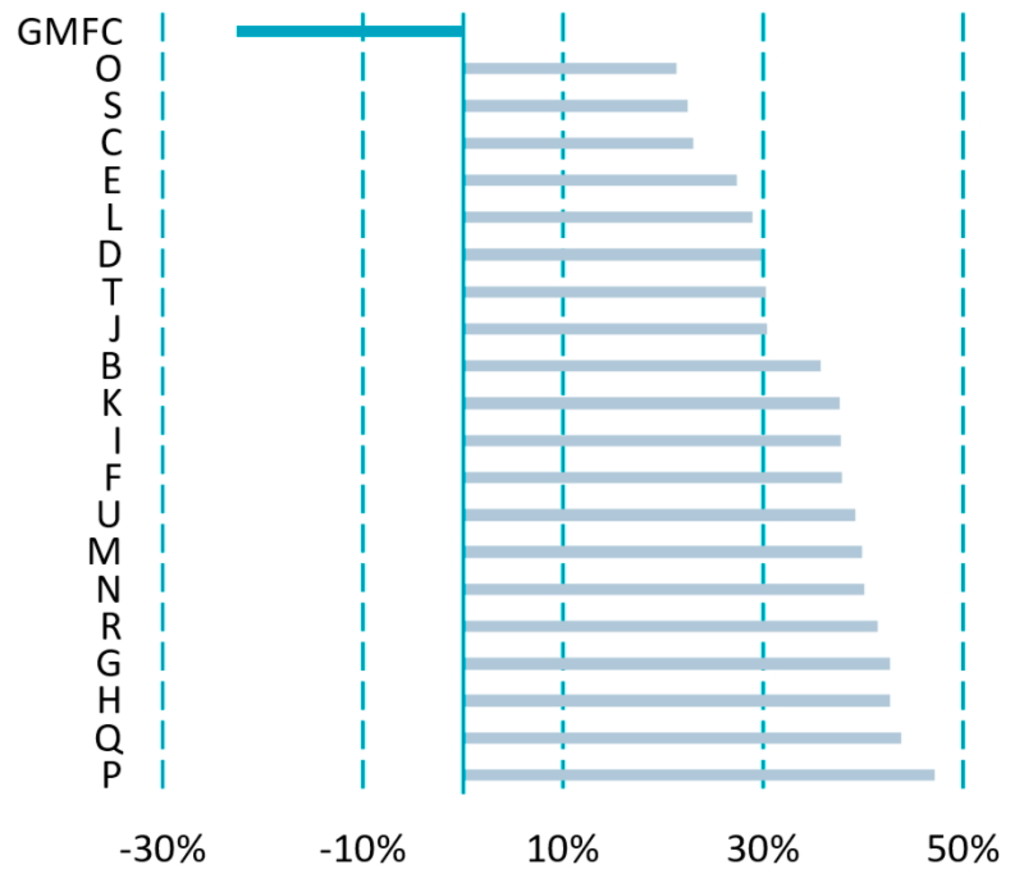

The live track-records of the various factor-based credit strategies show a further important benefit: low correlations with traditional actively managed credit portfolios. A peer group study (conducted in 2021) that analyzed the live period of Robeco QI Global Multi-Factor Credits found that its relative returns have a -23% correlation, on average, with the relative returns of fundamental global credit managers.

Figure 1 | Average outperformance correlation among global credit funds

Source: Morningstar Direct, Bloomberg, Robeco. Period: July 2015-June 2021. GMFC = Robeco QI Global Multi-Factor Credits (EUR-hedged) live track-record. B to U are 20 anonymized global credit funds (all euro hedged). Outperformance is calculated vs. Bloomberg Global Aggregate Corporates (euro hedged). The currency in which the past performance is displayed may differ from the currency of your country of residence. Due to exchange rate fluctuations the performance shown may increase or decrease if converted into your local currency. The value of your investments may fluctuate. Past performance is no guarantee of future results. Performance gross of fees, based on gross asset value. In reality, costs (such as management fees and other costs) are charged.

This means that incorporating a factor-based credit strategy into a multi-manager pool of fundamentally managed portfolios adds valuable diversification benefits. See our article “Multi-Factor Credits: Continued style diversification after Covid-19 crisis” for more information.

Innovating in the realm of sustainable investing

The systematic nature of factor credit portfolios means they lend themselves well to sustainability integration. And, indeed, sustainability has been a key consideration in our factor credit strategies since inception, and our approach has continued to evolve over time.

Credit analysts have assessed ESG risks in our factor-based credit portfolios since these strategies were launched in 2012, as part of human oversight of the systematic investment process. In 2013, we started supporting client-based exclusion lists, and have been applying Robeco’s Sustainability Inside exclusion list since 2015.

A further step was taken in 2016, with the decision to ensure that the average ESG scores of our funds are better than those of the benchmarks. Carbon emission constraints were introduced to the portfolios in 2020. Similar constraints on water use and waste generation have been applied since 2021.

Outlook

There is a growing body of research on factor investing in credit markets, from academia, brokers and index providers, while new competitors are entering the market. These developments are similar to what we saw in equity markets several years ago and augur well for a proliferation of factor investing in credit markets.

We believe the ability of factor-based credit portfolios to integrate multiple sustainability dimensions at the same time will further accelerate the adoption of systematic, factor-based portfolios.

Our aim is to maintain our leading position with a continued focus on research, innovation and sustainability. We will continuously look for ways to improve existing factors and explore new types of data sources and techniques, including natural language processing and machine learning. The launch of the new RobecoSAM QI Global SDG & Climate Multi-Factor Credits is testimony to our desire to stay ahead by introducing innovative strategies that contribute to a more sustainable future and at the same time deliver attractive risk-adjusted returns for our clients.

Footnotes

1 Houweling, Van Zundert, 2017, “Factor Investing in the Corporate Bond Market”, Financial Analysts Journal, Vol. 73, No. 2, pp. 100-115.

2 As a result of the lower risk of Conservative Credits compared to its benchmark, the strategy usually outperforms in bearish credit markets and underperforms in bullish credit markets. To neutralize this effect, we use a risk-adjusted benchmark for performance analysis. This risk-adjusted benchmark has the same degree of interest rate risk and credit risk as the portfolio.

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会