Co-Portfolio Manager

• 市場觀點

The energy shock will accelerate investment in smart energy solutions

Today’s energy markets are polluting, inefficient, volatile and vulnerable. The need for an energy transition has never been clearer and will be driven by electrification of end-use applications. Investments will be costly, but resistance has been lowered by the ongoing realities of high volatility, supply disruption and the need for domestic manufacturing that is both clean and energy efficient.

概要

- Current power systems victim of and contributor to geopolitical instability

- Electrification is key for a clean and secure energy future

- We’re on the cusp of a new investment cycle for a complex transition

Energy is critical for economic growth, but it is dominated by fossil fuels. Oil, coal and gas account for more than 80% of the primary energy needed to power the world’s economies. The Paris Agreement and the transition to a net-zero economy mean the shift to renewables and other low-carbon sources will accelerate in the next decade and ultimately supplant fossil fuels’ preeminence. But though momentum has increased, we cannot get there fast enough.

With 80% of total CO2 emissions, we always knew the energy sector was dirty. But the recent convergence of crises has underscored additional dangers. It is extremely inefficient; 60% of the fossil fuels extracted are wasted, with half lost in the production of electricity, and another half lost when fuels are inefficiently burned during combustion. It is highly vulnerable due to dangerous dependencies on countries rich in fossil fuels but poor at diplomacy and governance. And it is volatile; the conflict in Ukraine took energy markets off-guard, amplifying the rise in energy prices.

In order to limit extreme global warming, nearly 75% of global electricity generation must come from low-emission sources by 2030

Clean energy requires electrification of consumption

Decarbonizing can only happen when burning hydrocarbons in engines and furnaces is replaced with racing electrons in a circuit. But that future reality depends not only on producing clean energy via renewables but also on clean consumption downstream via electric end-use applications (See Figure 1).

In order to limit extreme global warming, nearly 75% of global electricity generation must come from low-emission sources by 2030. Currently, wind and solar account for only 6% of the global mix. To reach net zero, electricity consumption needs to outgrow energy consumption by a factor of two to three in the coming decades. This will be driven not only by transport markets (via lithium-ion batteries, vehicle powertrains, green hydrogen and passenger railways), but also buildings (via electric heat pumps, HVAC and insulation), and industrial markets (via the electrification of production processes).

The world’s largest economies have already set ambitious targets to increase the share of renewables in the national energy mix, including the US where the recently passed Inflation Reduction Act (IRA) devotes nearly USD 400 billion to building up domestic renewable energy production and storage as well as clean energy use by consumers.

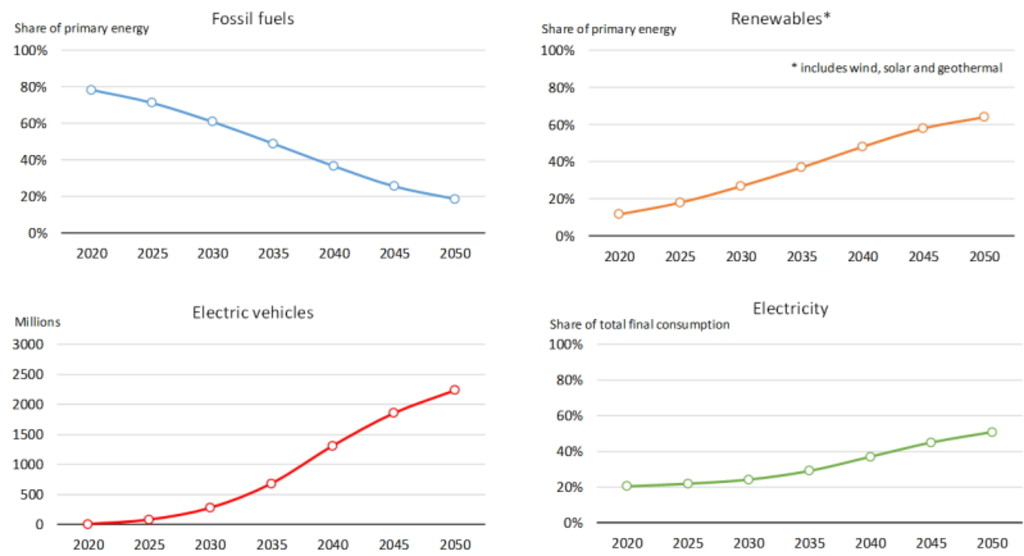

Figure 1 | Synchronized solutions – renewable energy supplies rise to support electric consumption

Renewable energy supplies will increase to support the electrification of end use applications.

Source: BP outlook

Driving not derailing the energy transition

Meanwhile, energy security has replaced climate security as an immediate concern, especially for Europe. Russia has cut EU gas supplies as tensions over the war in Ukraine have escalated, leaving the EU desperate for energy to keep its lights on, its citizens warm and its economies churning.

In the short term, countries are reverting to fossil fuels to fill the gap, but as geopolitical tensions tighten, the crisis emphasizes the high-stakes jeopardy of an economy dependent on fossil fuels. Recognizing this, the EU has acted swiftly to further accelerate its net-zero path. Its “REPowerEU” plan further cuts energy emissions, boosts electrification of buildings and industries, and expands investment in renewable supplies and infrastructure connections across bloc economies.

But the trade-offs between energy security and climate security are complicated by current technological capacity but also political will and public sentiment, especially if consumers are forced to ration.

不為人知的能源轉型事實

釋放智慧能源的力量!

High energy costs create incentives

Per the International Energy Agency, in order to reach net-zero emissions by 2050, annual investment needs to double to USD 5 trillion a year. Energy costs comprise a significant share of total expenses in a variety of business models, which means a company’s energy savings often have an outsized effect on the bottom line.

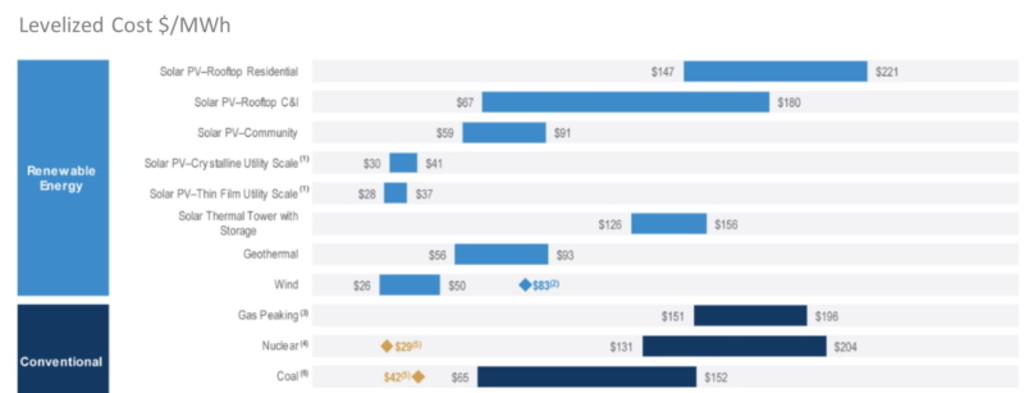

The benefits of transitioning will accrue in the long term, but over the short term many firms will see significant costs, especially in hard-to-electrify industries. However, renewable production costs are falling relative to traditional energy forms (see Figure 2). And with traditional energy costs exploding, consumers and energy-intensive industries will accelerate their own energy transitions as payback periods for investments in renewable energy procurement and energy-efficient solutions shorten.

Figure 2 | Renewables – cost competitive in industry and residential settings

The levelized cost of energy from renewable sources (solar installations, geothermal and wind) are competitive and in industrial settings much lower than conventional forms of energy such as gas, coal and nuclear.

Source: Lazard

Targeted investment in electrification

Despite present challenges, electrification is at the beginning of a huge investment cycle which will spill across sectors. We believe we are reaching a turning point where governments will stop incentivising combustible fuels and encourage the adoption of technologies that facilitate economies running fully on electricity. As the fuel mix diversifies and customers are granted more flexibility, competition between energy sources will increase. This will further accelerate economy-wide shifts in renewables and electrification.

The Smart Energy team invests in companies enabling and accelerating the transition along the entire electrification value chain – from upstream companies supporting the generation of renewable wind and solar power to mid- and downstream companies creating more efficient ways to use, store and distribute it. Alongside investments in maturing technologies, the team is continuously looking for companies that can simplify and scale production of breakthrough solutions that will further accelerate the electrification of the economy.

重要資料

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。