Head of Fixed Income Client Portfolio Management

概要

- Quant strategies have performed well in credits, unlike in equities

- Value factor in credits unaffected by outperformance of big tech

- Multi-factor portfolios in credit and equity have a low correlation

Quant equity strategies, hedge funds and alternative risk premia strategies have struggled in recent years to keep up with markets, with strategies exposed to the value factor being hit particularly hard. Not surprisingly, then, terms such as ‘quant quake’ and ‘quant crisis’ were coined to label this period of underperformance in quant strategies. The positive performance of quant credit strategies during this period seems to have received less attention, though. Remarkably, the value factor was the main driver of the outperformance in the credit market. In this article we explain in more detail why value did not struggle in credits – and, consequently, why there is no quant crisis in credits.

Most quant or factor-based equity strategies have exposure to the value factor. Value investing is the best-known and oldest investment style, and the value premium has been documented in numerous academic studies. Attractively valued stocks are typically those of mature companies in traditional business sectors that are less popular among investors. Although value stocks have historically outperformed growth stocks, the experience in recent years has been completely different: the incredible returns generated by a handful of very large growth companies in the technology sector have dominated the market’s average return and boosted stock market indices to all-time highs.

To illustrate, the cumulative total return of the FAANG stocks1 over the last five years was a staggering 280%, compared to 78% for the broad MSCI World Index, which would have been 11 percentage points lower without the FAANG stocks. From a valuation perspective, big tech stocks were unattractive as they were trading at expensive multiples such as the traditional price-to-book ratio. They were therefore not selected in value portfolios. Portfolios without big tech stocks clearly lagged their benchmarks, and so did most quant equity strategies that employed the value factor in their investment process. Outperforming equity factors like profitability and momentum failed to offset the losses of the value factor2.

獲取最新市場觀點

訂閱我們的電子報,時刻把握投資資訊和專家分析。

No big tech dominance in credits

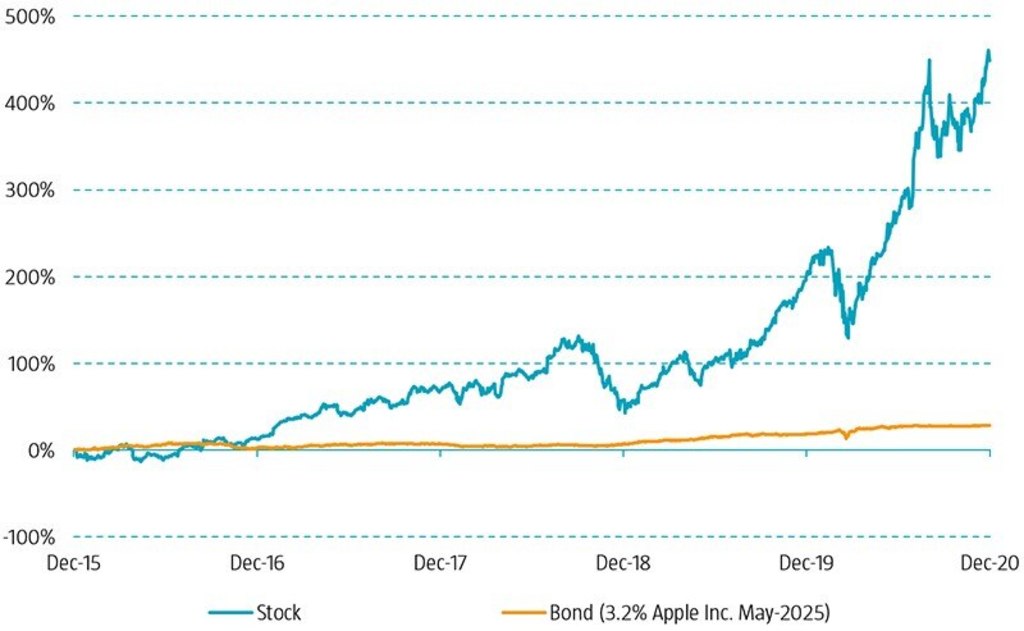

The dominance of big tech firms in the equity market does not exist in credits. While the high returns of big tech stocks may have been justified by the theoretically unlimited upside potential in future revenues for equity investors, bond returns were much lower because bond holders are left with just fixed coupons and repayment of the bond’s notional value. We illustrate this in Figure 1, in which we compare the return of an investment in an Apple stock and an Apple bond over the 2016-2020 period. The cumulative return of the Apple stock was 453%, compared with 28% for the bond.

Figure 1 | Apple stock and bond return

Source: Bloomberg. Apple stock return in USD based on closing prices adjusted for dividends and stock splits. Apple bond return is the total return in USD including coupons.

Due to the extreme rally of big tech stocks, the weight of the technology sector in the MSCI World index also grew rapidly, from 14% at the end of 2015 to 22% at the end of 2020, amplifying their dominance in equity index returns. In short, tech stocks were already big and expensive in 2015, but due to their strong performance they only got bigger and more expensive over the past few years.

By contrast, the returns of big tech firms had much less of an impact on credit index returns. This is not only because the bond returns were much lower than the equity returns, but also because the weight of these firms in the credit index was much smaller. Big tech firms did not issue a lot of bonds as they could more cheaply finance their acquisitions with stocks or cash. To illustrate, the total weight of Apple, Microsoft, Amazon, Facebook, Alphabet and Tesla in the credit market is only 1.5%, while these six companies represent almost 15% of the global equity market.

Value in credits

We see that value in equities struggled, mainly due to missing out on the staggering returns of big tech companies, and that big tech did not dominate in terms of returns and market weight in credits. So how did value perform in credits?

Remarkably, value was the best-performing factor in the credit market over the past five years compared to other well-known factors such as low-risk, quality, momentum and size. How can the strong performance of value in credits be explained? In short, value prefers bonds that are attractively priced and thus have above-average credit spreads compared to other bonds with the same risk profile. Such bonds generally perform strongest when credit markets compress and deliver positive credit returns, while the low-risk factor does better when credit returns are negative, as it prefers bonds and issuers that are safer than average. In recent years, credit markets generally posted positive credit returns, supported by the ongoing search for yield and central bank corporate bond buying programs. In this environment, value performed strongly.

In terms of the value factor’s preferences in the credit market, we find that it actually had a modest preference for the technology sector on average over the last five years. So, bonds from tech firms on average carried somewhat attractive risk premiums given their credit risk and given the credit spreads of similarly risky bonds. This contrasts sharply with the unattractive valuations of tech firms in the equity market and the underweight in many quant equity strategies. Robeco’s Multi-Factor Credits strategy did have overweigh

t positions in tech companies. Next to the somewhat attractive valuations, the overweights were mainly driven by the low-risk/quality and momentum factors that appreciated their characteristics of – on average – solid balance sheets, attractive profitability and strong equity market momentum. The divergent relative performance of multi-factor portfolios in equities and credits is not a surprise. Previous research shows that the two only have a 17% correlation.

Footnotes

1 The weighted average total return in USD of a group of big tech firms: Facebook, Apple, Amazon, Netflix and Alphabet (Google) over the period January 2016 to December 2020.

2 For more insights we refer to the article “The quant equity crisis of 2018-2020: Cornered by big growth” by David Blitz, published in February 2021.

重要資料

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。