Head of Investments China

• 市場觀點

China: charting the course to carbon neutrality

China’s pledge to become carbon neutral by 2060 has left many observers both excited and perplexed. Making the world’s largest CO2 emitter carbon neutral within the next 40 years is no mean feat, and will have far-reaching consequences. But the formidable challenges associated with the transition also come with many investment opportunities.

概要

- Achieving carbon neutrality by 2060 will require radical changes

- Formidable challenges lie ahead, but also investment opportunities

- Renewables, electric vehicles and energy storage technologies set to benefit

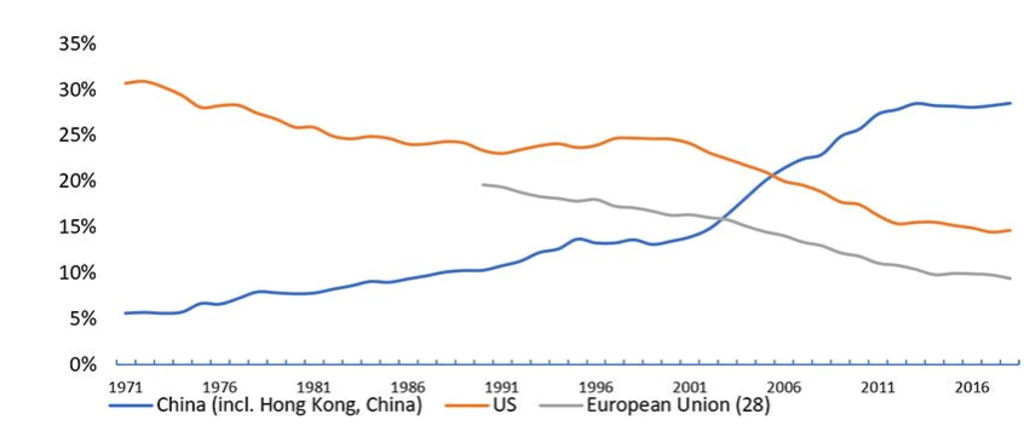

China is by far the largest carbon emitter in the world. The country currently accounts for close to 30% of global CO2 emissions, according to the International Energy Agency (IEA), versus 15% for the US and 9% for the European Union.1 Colossal investments will be required to help the transition, especially in areas such as renewables, the electrification of transport and nuclear power generation.

Figure 1: China’s rising share of global CO₂ emissions

Source: IEA. CO2 emissions from fuel combustion in metric tons.

The rapid pace at which CO2 emissions re-embarked on their upward path last year, in spite of all the havoc caused by the Covid-19 pandemic, is a testament to the disruption needed only to put our economies on the necessary trajectory. So, while current trends in CO2 emissions may not be comforting, the recent change of tune at the highest level clearly warrants close attention.

Net zero carbon emissions will require combined efforts in three directions. Firstly, a shift in the country’s gross domestic product (GDP) mix, away from carbon-intensive industries such as manufacturing and construction, towards more carbon-light activities such as services. In fact, China’s gradual move away from industrial activities started over a decade ago.

Secondly, a change in the country’s energy mix, away from coal and oil towards renewables. Despite sizable investments in areas such as hydro, wind and solar power over the past decade, China’s economy remains heavily dependent on fossil fuels. In particular, China is extremely reliant on coal, which is arguably the most problematic energy source in terms of carbon emissions.

Finally, carbon compensation plans will also play a key role. Even with the most radical measures, full decarbonization is unlikely to be achieved without compensation initiatives. From this perspective, carbon capture, utilization and storage (CCUS) techniques, as well as forestation and reforestation, will likely become an indispensable part of the government’s toolbox.

While current trends in CO₂ emissions may not be comforting, the recent change of tune at the highest level clearly warrants close attention

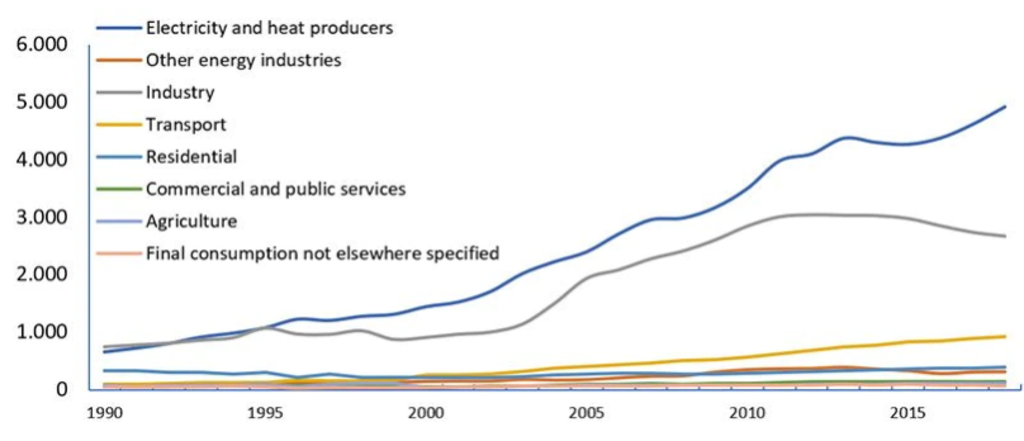

Around 90% of China’s CO2 emissions come from electricity and heat production, industry, and transport, with electricity and heat production representing half of all emissions.2 Logically, these three areas will be affected most by the transition, with electricity and heat production at the forefront.

Figure 2: China’s historical carbon emissions

Source: IEA. CO2 emissions from fuel combustion, in million metric tons.

Yet there are also important differences across sectors. For instance, while industry emissions already peaked almost a decade ago, emissions from electricity and heat production, as well as from transport sectors, have yet to. But there are signs that the tide is slowly turning. For one, investments in coal-fired power generation have been slowing sharply over the past few years.

Meanwhile, moving towards a more sustainable transport sector will also require drastic changes, as well as sizable investments. These include a greater use of public transport infrastructures, an accelerated increase in the use of electric vehicles, and a further improvement in the efficiency of conventional oil-powered vehicles.

Seizing investment opportunities

Given the changes needed in most sectors to achieve carbon neutrality, the key issue for investors is to identify any major risks they might be exposed to, and to find the most attractive opportunities. Arguably, the most exposed companies are fossil fuel producers and in particular oil majors. Their core business is fundamentally at odds with decarbonization.

了解最新的可持續性市場觀點

訂閱我們的電子報,探索塑造可持續投資的趨勢。

Companies able to support the transition are poised to benefit from the decarbonization trend

But many other industries also stand to suffer from a badly-handled transition, including petrochemicals, steel and cement. Conversely, companies able to support the transition are poised to benefit from the decarbonization trend. In some cases, the likely impact of decarbonization is already well known, but in others, the consequences remain difficult to fully grasp.

For now, we see opportunities in three major areas. Renewables are expected to retain the lion’s share of investments. But electric vehicles are also expected to be among the big winners. Finally, upgrades in power networks and energy storage technologies, as well as the hydrogen industry are likely to capture a significant portion of total investments too.

Recent official announcements suggest there will be an ambitious ramping up of clean power over the coming decade, with the share of non-fossil fuels in primary energy now expected to reach 25% by 2030, compared to an earlier target of 20%.3 Given the gradual exhaustion of hydropower potential and slowing nuclear power additions, this targets implies a rapid step-up of wind and solar.

Beijing has also made it clear that it wants to continue leading the way in new energy vehicles (NEVs), with a recently approved plan for the industry. According to the plan, NEV sales are expected to reach 20% of overall new car sales by 2025, up from 5.4% last year.4 This target for 2025 is lower than the previously stated target of 25%, as it takes into account the rough patch of 2019 and 2020.

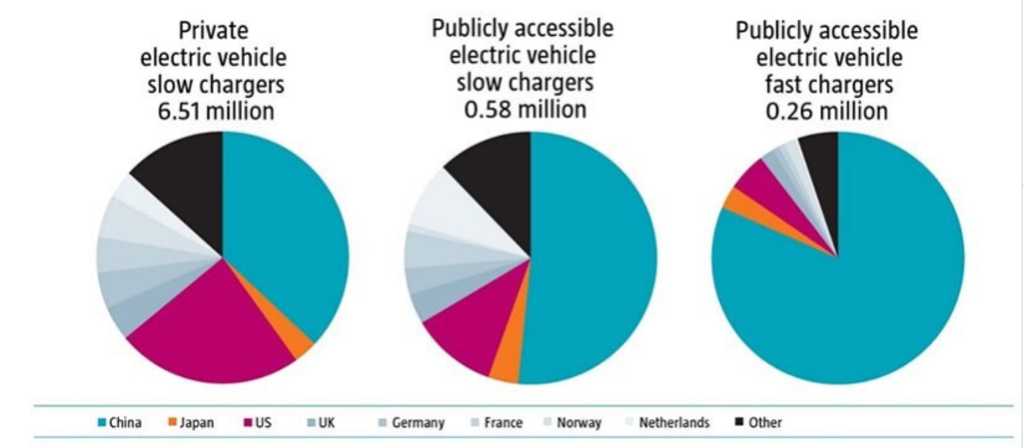

Figure 3: China leads in the number of EV charging points

Source: IEA, ‘Global EV Outlook’, 2020.

Finally, while renewables will play the most critical role in the transition toward carbon neutrality, additional storage technologies will be also needed to address intraday and seasonal variability issues inherent to wind and solar energy, and to decarbonize all parts of the economy – including the most carbon intensive ones, such as steel and cement production.

From this perspective, two complementary technologies – batteries and hydrogen – are likely to play a key role given their ability to convert electricity into chemical energy and vice versa. China is already the world leader in terms of battery manufacturing, accounting for around 70% of global capacity.5 Despite the air pocket experienced early in 2020, production recovered rather quickly.

Meanwhile, developments in hydrogen are also set to accelerate over the coming decades. The China Hydrogen Alliance, a trade group representing the sector at large, estimates hydrogen could account for up to 10% of China's total energy mix in 2050, compared with less than 1% today.6

Footnotes

1Source: IEA. Based on CO2 emissions from fuel combustion for 2019.

2Source: IEA. Based on CO2 emissions from fuel combustion for 2019.

3Myllyvirta, L., 15 December 2020, “Analysis: China’s new 2030 targets promise more low-carbon power than meets the eye”, Carbon Brief article.

4Yu, C., 4 November 2020, “High-quality growth of new energy vehicle sector prioritized”, China Daily article.

5Gül, T., Fernandez Pales, A. and Paoli L., May 2020, “Batteries and hydrogen technology: keys for a clean energy future”, IEA.

6China Hydrogen Alliance, 2018, ‘White Paper on China Hydrogen and Fuel Cell Industry’, white paper.

下載刊物

重要資料

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。