Client Portfolio Manager

• 市場觀點

The link between ESG and performance: SDG Credits stands the test

Attribution analysis shows that investing in a way that contributes to the SDGs supports financial performance.

概要

- SDG Credit strategies have outperformed their respective indices year to date

- SDG screening supports the ability to screen out poor performers…

- …and does not impede our capacity to generate alpha via credit selection

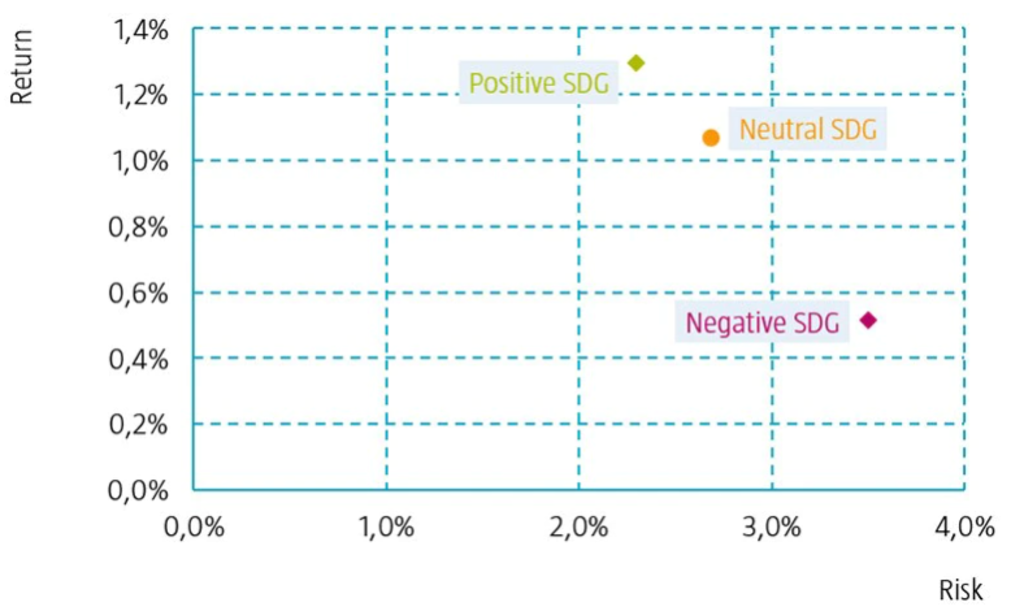

Robeco developed a unique approach in 2018 to screen for UN Sustainable Development Goals (SDGs), which is applied across a range of Robeco strategies. Last year, the initial analysis showed that sectors which were positively aligned with the SDGs had lower credit risk and that, over a five-year period, sectors with a positive or neutral SDG rating had a superior risk-return relationship compared to those with negative SDG scores.

With the SDG Credit strategies now having developed a track record, the next step of evaluating results at the portfolio level was taken, to determine how the SDG measurement framework adds value in practice. In particular, the results were assessed in the wake of the Covid-19-related market and economic crisis.

Figure 1 | Investment grade credit: risk-return, five-year history

Source: Barclays, and Robeco calculations based on the global IG universe. Data up to August 2019, five-year history. The above chart is for illustrative purposes and does not represent the performance of any specific Robeco investment strategy.

Holding strong during Covid-19 crisis

Following a positive start, 2020 has proven to be unprecedented, with a dramatic sell-off in global credit markets in response to the Covid-19 crisis and then a strong rebound in credit markets since the end of March. Spreads moved from late bull market tights to recessionary levels in both investment grade and high yield within just four weeks. Quick and decisive action by governments and central banks prompted a substantial tightening in credit markets in the second and third quarter. The Global Investment Grade Credit Index1 declined by -6.07% (EUR) in March, contributing to the first-quarter decline of -3.6%. The subsequent recovery resulted in a +7.57% (EUR) return in the second quarter and a more tempered gain of +1.49% (EUR) in the third quarter.

Detailed attribution analysis at the portfolio level shows that Robeco’s SDG credit screening methodology contributed to positive results during the height of the crisis and in the months that followed.

Performance of the RobecoSAM Global SDG Credits strategy

The RobecoSAM Global SDG Credits strategy has outperformed2he Bloomberg Barclays Global Aggregate Corporate Index over the year to date. An outperformance of +103 basis points in the first quarter, +149 bps in the second quarter and +31 bps in the third quarter, takes the year-to-date outperformance to +292 basis points (DH EUR share class, gross of fees). Since inception in June 2018, the strategy has outperformed the index by 181 basis points per annum, and the cumulative outperformance over this period was 457 basis points (DH EUR share class, gross of fees).

Attribution analysis shows that a quarter of this cumulative outperformance is directly attributed to the SDG screening, through avoiding the bad names. In particular, the findings show:

Avoiding names with negative SDG scores contributed 68 basis points cumulatively over the period since June 2018. This included avoiding some large integrated oil and gas companies that have a negative SDG score, avoiding the bigger automotive manufacturers with little or no revenues from electric vehicle sales and not being exposed to some of the sizeable, well-known utilities and banks with a negative SDG score. Amongst banks, for example, we avoided exposure to those with negative SDG scores owing to concerns related to corporate conduct.

Of the outperformance, 38 basis points is linked to favoring companies with a positive SDG contribution. Robeco’s SDG methodology led to the inclusion of a number of firms due to their positive SDG scores for business practices – amongst others, an Indian and US telecoms operator and a US technology company. These SDG-related selections contributed to the overall outperformance.

Beyond the SDG screening process, there is also a strong contribution from issuer selection, totaling 161 basis points since June 2018. This is support for our conviction that SDG screening does not hinder our ability to generate performance through bottom-up issuer selection, which is an important performance driver in all our credit capabilities.

了解最新的可持續性市場觀點

訂閱我們的電子報,探索塑造可持續投資的趨勢。

Performance of the RobecoSAM Euro SDG Credits strategy

SDG screening was implemented for the RobecoSAM Euro SDG Credits strategy in January 2019. Over the period January 2019 to September 2020, the strategy outperformed3 the Bloomberg Barclays Euro Aggregate Corporate Index by +113 basis points. A similar outcome is seen here with regard to the contribution of the SDG screening to relative performance, albeit over a shorter period.

The SDG screening added 68 basis points, with equal contributions from avoiding names with a negative SDG score and being overweight in names with a positive SDG score. A strong contribution from issuer selection is evident here, too, at 79 basis points.

How the SDG screening works

Robeco selects the SDG-eligible universe of credits using its proprietary SDG screening methodology, which was developed in 2018. This process of screening companies and giving each an SDG score comprises three steps: establish how the products or services produced by the company contribute in a positive or negative way to the SDGs, analyze how the company’s conduct contributes to the SDGs, and determine whether it is or has been involved in any controversies and, if so, whether measures have been taken by the management to prevent this from reoccurring. The SDG scores range from +3 to -3. Only bonds with a positive or neutral SDG score are eligible for inclusion in the portfolio; those with a negative score are excluded from further consideration.

This is an updated version of an article that was published in April 2020.

Footnotes

1Global Investment Grade Credit Index: Bloomberg Barclays Global Aggregate Corporate Index.

2Source: Robeco. RobecoSAM Global SDG Credits DH EUR, gross of fees, based on gross asset value. Benchmark: Bloomberg Barclays Global Aggregate Corporate. In reality, management fees and other costs are charged. These have a negative effect on the returns shown. The value of your investments may fluctuate. Results obtained in the past are no guarantee for the future.

3Source: Robeco. RobecoSAM Euro SDG Credits, gross of fees, based on gross asset value. In reality, management fees and other costs are charged. These have a negative effect on the returns shown. Periods shorter than one year are not annualized. The value of your investments may fluctuate. Results obtained in the past are no guarantee for the future.

Important information

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.