Portfolio Manager

• インサイト

How M&A, IPOs and a bit of GENIUS are driving fintech fever

A series of successful IPOs and M&As combined with the passage of the groundbreaking US GENIUS Act are rapidly expanding fintech solutions in financial markets and creating significant opportunities for Robeco’s FinTech strategy.

Summary

- Capital market activity is roaring back to life

- Landmark legislation is laying foundations for tokenization of assets

- Fintech strategy well positioned as structural momentum accelerates

In our 2025 Outlook at the start of the year, we anticipated a resurgence in private and public fintech funding which began to materialize in late spring with a wave of IPOs. Online brokerage platforms WeBull and eToro went public in April and May, respectively, while neobank Chime followed in June, closing the month 28% above its listing price and reaching a market value of USD 13 billion.

Though stellar in their own right, the star performer in this season of launches is stablecoin issuer Circle. It made an exceptional debut, with its share price increasing almost ninefold at its peak before closing in June with a market capitalization of USD 40 billion. And there’s more capital action still to come. Klarna, a buy-now-pay-later provider has already initiated its IPO process, and digital wealth manager Wealthfront confidentially filed for an IPO last month.1

Private fintech funding also continued with Ramp, a spend-management fintech, which raised another USD 200 million in its latest funding round, lifting its valuation to USD 16 billion. Additionally, payment processor Stripe acquired crypto wallet provider Privy for an undisclosed amount, while accounting software provider Xero acquired bill payments platform Melio for USD 2.5 billion. Robust capital market activity signals growing confidence in a diverse and broadening fintech market, creating significant growth opportunities for the FinTech strategy over the short-, mid- and long-term.

Robust capital market activity signals growing confidence in a diverse and broadening fintech market

Genius in motion means more tokens

Stablecoins, once a crypto novelty, are set to become mainstream with the passage of the GENIUS Act (Guiding and Establishing the National Innovation for US Stablecoins Act of 2025) in the US Senate. This landmark legislation will most likely allow banks and regulated issuers to release tokenized US dollars by the end of this summer. That’s the first step in legitimizing stablecoins in cross-border and domestic payments, but also for corporate treasury operations and financial services infrastructure.

The swiftness of response from retail commerce leaders is significant. Both Amazon and Walmart are exploring their own stablecoin issuance which could save them substantial amounts in fees.2 Meanwhile, in partnership with Shopify, Coinbase introduced its stablecoin payment stack built on its base layer-2 blockchain.3 The technology, which went live in June, seamlessly integrates US dollar coin (USDC) payments into Shopify’s processing systems for vendors. These modular stacks leverage programmable payment flows that replicate traditional e-commerce logic4 and will enable tokenized payments to be easily adopted and scaled by online vendors.

Additionally, Fiserv’s forthcoming launch of FIUSD (a US dollar-backed stablecoin) on the Solana blockchain, supported by Paxos and Circle, demonstrates how core banking infrastructure is integrating with blockchain, offering 24/7 settlement and embedded compliance tools. These announcements indicate that stablecoins’ programmable logic and real-time interoperability serve as a foundation for future financial services.

Both Amazon and Walmart are exploring their own stablecoin issuance which could save them substantial amounts in fees

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

Simply stellar stablecoins

Stablecoin issuers primarily earn revenue through interest on fiat currency by depositing it in banks or purchasing US Treasury bills. By the end of June, stablecoins on public blockchains totaled USD 254 billion, with USDT 159 billion (Tether) and USDC 61 billion (Circle). For comparison, the US Federal Reserve’s M2 money supply (a measure of how much fiat currency is circulating in the US economy) was USD 22 trillion at the end of May. In an X post, US Treasury Secretary Scott Bessent projected stablecoins could reach a market size of USD 3.7 trillion by 2030, indicating potential adoption beyond digital assets.5

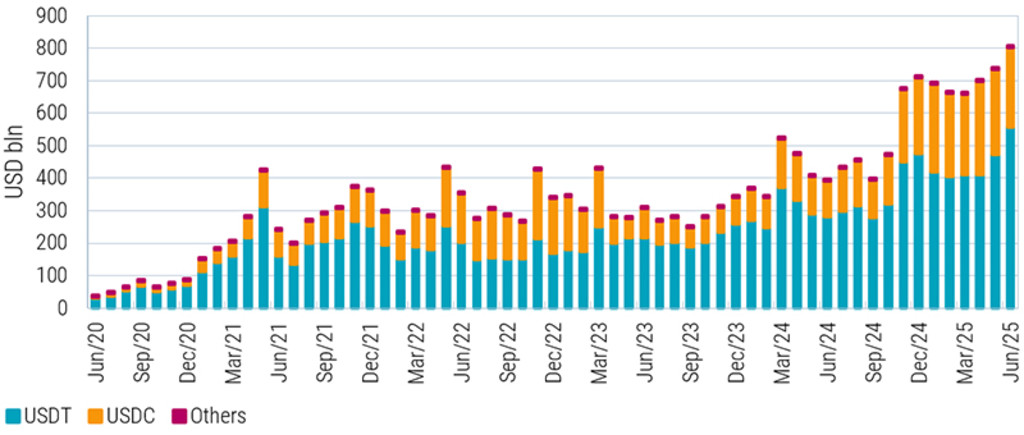

This adoption should be tracked by transaction volume growth (albeit with distortions from bots and high-frequency trading). Figure 1 shows adjusted transaction volumes growing 104% year-on-year to over USD 800 billion in June. JP Morgan CEO Jamie Dimon says his firm moves about USD 10 trillion daily – taken as a proxy for stablecoin volumes, it is clear there is significant room for growth.

Figure 1 – Stablecoin adjusted transaction volumes are growing rapidly

USDT = US dollar tether stablecoin backed by digital currency provider, Tether. USDC = US dollar backed stablecoin offered by Circle, a leading digital infrastructure provider. Source: Allium, Visa, Robeco

The implications of tokenization

Both Visa and Mastercard, giants in traditional commercial payment-settlement systems, have invested heavily to incorporate stablecoin use into their networks. Visa’s CEO, Ryan McInerney, has expressed optimism about stablecoin’s future, but stresses the need for trust, ease-of-use, and scale.

Although stablecoin adoption beyond the digital asset ecosystem is still in its early stages, it appears to be more of a threat to the business models of card issuers than to payment network companies. Visa and Mastercard’s tokenization and merchant network capabilities remain a powerful moat to connect the traditional system with the crypto world, although it does put a question mark around terminal growth. Share prices of both Visa and Mastercard reached all-time highs in June but contracted 5.5% by the end of the month.

Also in June, Robinhood’s ‘To Catch A Token’ event focused on their development of a layer-2 blockchain optimized for real-world assets. This blockchain infrastructure enables the seamless transfer of assets at any time. Robinhood announced stock tokens on listed US equity, such as Nvidia, Microsoft, and Apple, while also offering tokenized shares of OpenAI and SpaceX to users in Europe. Ironically, the regulatory challenges are greater in the US than in Europe, although Robinhood and Coinbase are reportedly in discussions with the SEC to smooth issuance without added legal complexity.

We are confident that the buildout of robust technological infrastructure that is governed by regulatory oversight are strong signals of structural tailwinds that will spur legitimacy, acceptance and growth of tokenization in the wealth management industry. Clearly, Robinhood and Coinbase are on the forefront of these efforts. Robinhood’s stock increased 13% on the day of the event and added 151% year-to-date, despite volatility in April.

Footnotes

1‘Robo-advisor Wealthfront files confidentially for an IPO.’ Bloomberg, June 2025.

2Walmart and Amazon Are Exploring Issuing Their Own Stablecoins, The Wall Street Journal, 13 June 2025.

3Layer-2 networks are built atop the original blockchain base layer and provide additional functionality and flexibility to blockchain architecture. Layer-2 stacks are making blockchain transactions cheaper, faster and more flexible, which will promote scale and adoption for real-world financial transactions.

4Essentially mirroring fiat workflows – from customer checkout, payment authorizations, digital wallet connections, on-chain ledgering, escrow-based captures and refunds.

517 June 2025, X post from the account of US Treasury Secretary, Scott Bessent

Important note:

The companies referenced are for illustrative purposes only in order to demonstrate the investment strategy on the date stated. The companies are not necessarily held by the strategy. This is not a buy, sell or hold recommendation, nor should any inference be made on the future development of the company.

Important information

insights.detail.disclaimer.text