Head of Sustainability Integration

• SI Debate

SI Dilemma: Optimist, pessimist or realist for sustainable development?

It was Winston Churchill who said: “A pessimist sees the difficulty in every opportunity; an optimist sees the opportunity in every difficulty.” I used to be firmly in the optimist category. Problem? Face it head on! Something wrong with the system? Change it from the inside! But what has been achieved so far when it comes to sustainable development? I am slowly becoming more pessimistic. Let’s look at some numbers.

執筆者

まとめ

- Carbon intensity of the economy has decreased, but still emissions have grown

- Progress in meeting the Sustainable Development Goals has been too slow

- Sustainable development issues such as improving food are complex and interlinked

For this SI Dilemma column, I will be referring to some of our specialists in Robeco’s SI Center of Expertise who have written about progress in their respective areas: climate change and the Sustainable Development Goals (SDGs).

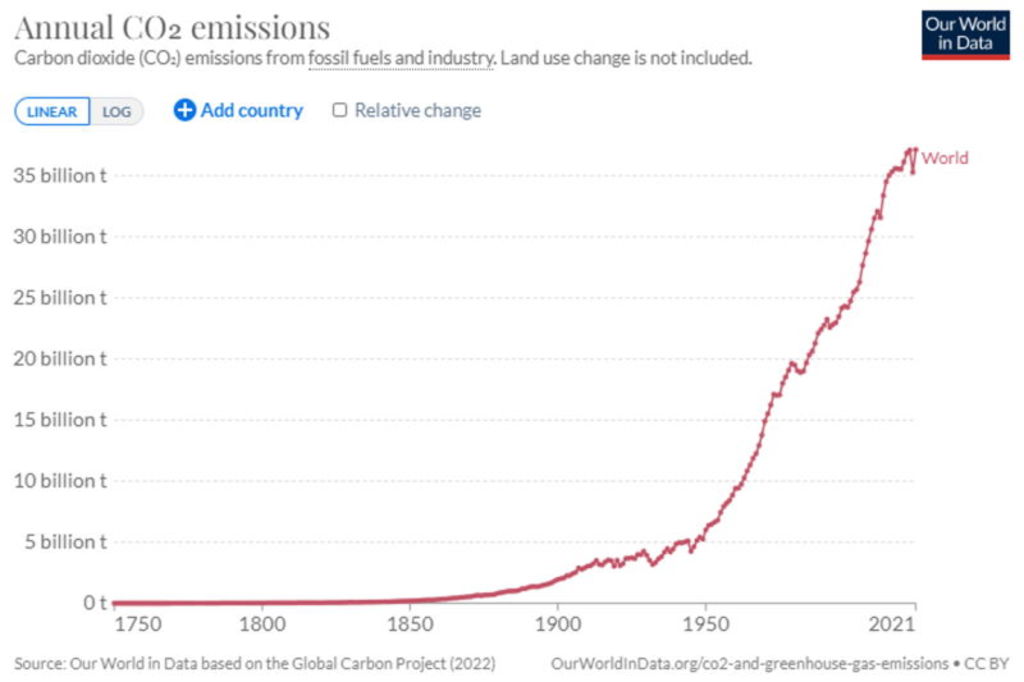

Despite efforts to move to cleaner technologies in producing energy, and despite a global pandemic, which caused global emissions to reduce for one year, CO2 emissions are back at pre-Covid levels. The carbon intensity of our economies has decreased, but due to economic growth, emissions are still increasing, as can be seen in the graph below. And this graph excludes land use change which is a big contributor to climate change as well.

As our climate strategist Lucian Peppelenbos wrote in his column on the Intergovernmental Panel on Climate Change (IPCC) report that was released last year: We are not on track in tackling global warming, but we do hold the answer. With the right leadership, the world can avoid dangerous climate change. That’s still the key message from the UN Climate Science Panel’s IPCC report.

For investors, there is an urgency to respond to the IPCC’s assessment that the financial sector is not sufficiently pricing in climate risk. The IPCC concluded that there must be a massive shift in investments over the next 5-10 years towards low-carbon energy, transport and urban infrastructure.

Another article1 mentions that the COP27 summit at the end of 2022 did lead to plans to create a fund for developing countries to finance decarbonization, but did not produce much in terms of concrete solutions, and climate policies still fall short. If all plans are met, the summit leaves us heading for 2.5 °C of global warming.

Mixed picture on the SDGs

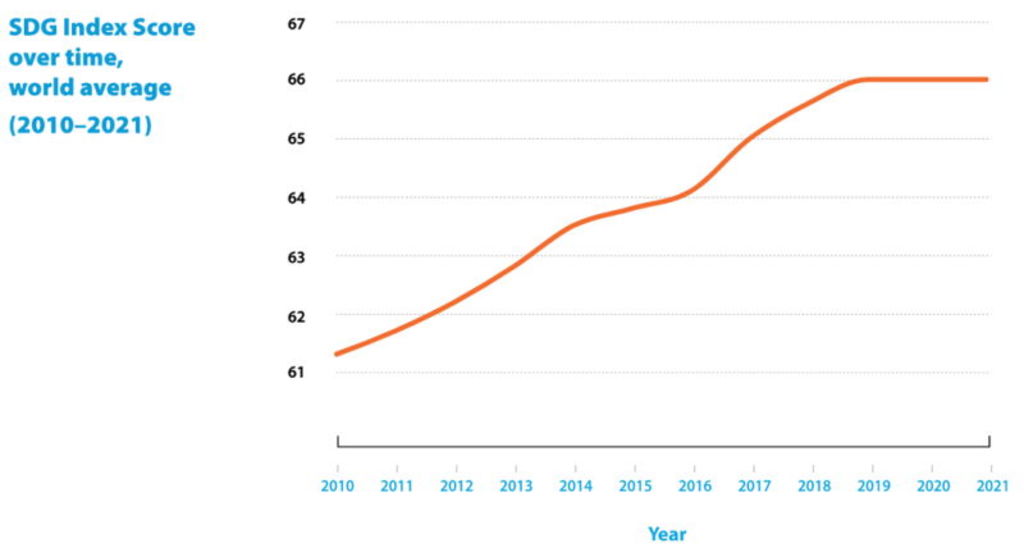

Looking beyond climate change to a broader set of sustainability goals, the UN SDGs, there is a mixed picture. The goals were established in 2015 and should be achieved by 2030. At half time, our SDG strategist Jan Anton van Zanten tallied up the progress.2

Source: https://dashboards.sdgindex.org/

As can be seen in the SDG index, he concluded that progress is being made over time to achieve the goals, but it has been far too slow, and is now even decreasing slightly. No country is on track to achieve them by 2030, partly due to Covid.

Beyond the pandemic, what is now particularly worrying are the negative trends on environmentally focused SDGs. If we do not address climate change and halt the loss of biodiversity embodied in three of the goals, it is unlikely that we will achieve any of the other SDGs, given that all social systems depend on the natural environment.

Optimist, pessimist or realist?

‘I always like to look on the optimistic side of life, but I am realistic enough to know that life is a complex matter’ – Walt Disney

As mentioned above, these matters are indeed complex and interlinked. For example, solving SDG 2.1 to end hunger and ensure year-round access to safe and nutritious food by all people, in particular the poor and people in vulnerable situations, will be difficult to achieve while also simultaneously solving SDG 15.1.

This seeks to ensure the conservation, restoration and sustainable use of terrestrial and inland freshwater ecosystems and their services, in particular forests, wetlands, mountains and drylands, in line with obligations under international agreements or many of the other climate and biodiversity-related targets. Growing more food to meet SDG 2.1 makes this much less likely.

Better global regulation

In recent years, the financial sector has woken up to ‘sustainability’, and focused on integrating financially material ESG factors into portfolios, to make better-informed investment decisions. However, there are two issues with this. What the IPCC mentions in its report about the underpricing of climate risk also goes for other externalities such as the loss of biodiversity, poor labor conditions, poor governance and poor community relations.

This should be solved by better global regulation, which puts a price on these issues and makes sure that investors and corporates internalize these external costs. If not, then ESG integration (as long as not everyone is doing it in the same way or using the same information) could help to create better investment decisions, but would not directly benefit sustainable development.

Moving to impact investing

Or we need to find a way to go beyond ESG integration and move to impact investing, creating structures that can fund the trillions of dollars in investments needed (in emerging markets) to create sustainable development. A start was made at COP27 with the creation of a loss and damage fund by wealthier countries. But this still needs to be operationalized.

Green, social and sustainability-linked bonds are also good instruments for large investors to create impact on the ground. The end-investor needs to be vocal about their desire to not only optimize wealth, but also well-being. We are not there yet. Only a small part of all assets under management goes to directly funding corporate projects that help sustainable development.

No other option

It felt good to let the ‘pessimistic me’ out of the closet for this column. It is important to take stock of what is happening in the real world from time to time. And there is not a lot of reason for optimism.

At Robeco, we have a 50-strong SI Center of Expertise through which all investment teams integrate financially material ESG information into the investment process. We spend a lot of time and effort in researching, integrating and engaging on sustainability issues as well as supporting our clients on this topic. And there is a handful of asset managers and asset owners that have been doing the same as us for many years.

We will never know where we would be if we had not done that. We know we have had some successes with engagement, most notably in getting some board members elected that had the right knowledge, and were able to start transition processes at some of the companies we invest in. And whereas COP27 left us heading for 2.5 °C of global warming, five years ago, we were heading for 4 °C.

So, to end with another quote from Churchill, which also applies to me: “For myself, I am an optimist – it does not seem to be much use to be anything else.”

SIディベート

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会