Portfolio Manager

• Visión

El precio marca las tendencias de gasto de los consumidores

La inflación está disminuyendo, pero el sentimiento del consumidor y el comportamiento de compra sugieren que los hogares siguen centrados de forma vigilante en el valor y la asequibilidad. Los patrones de gasto están divergiendo: los hogares de mayores ingresos impulsan el crecimiento del consumo, mientras que los grupos de menores ingresos reducen sus gastos. La competencia por los corazones (y bolsillos) de los consumidores se está intensificando, ya que los minoristas compiten no solo en el precio más bajo, sino también en su capacidad para ofrecer el mayor valor.

Authors

Summary

- La pérdida de poder adquisitivo es una preocupación clave para consumidores y compañías

- Aunque el sentimiento del consumidor es pesimista, el gasto mantiene una notable resiliencia

- Los minoristas que ajustan los precios, los comercios de descuento y los mercados de segunda mano se están beneficiando

El lenguaje de las salas de juntas refleja cada vez más las preocupaciones de los hogares. Las compañías de los segmentos de bienes de consumo básico y consumo discrecional hablan de «asequibilidad» con una frecuencia sorprendente: las menciones por parte de cargos ejecutivos se han triplicado en los últimos cinco años que comprenden hasta el T1 de 2026 (véase el gráfico 1). Los hogares controlan cada dólar que gastan, y las compañías se han dado cuenta.

La pérdida de poder adquisitivo en cifras

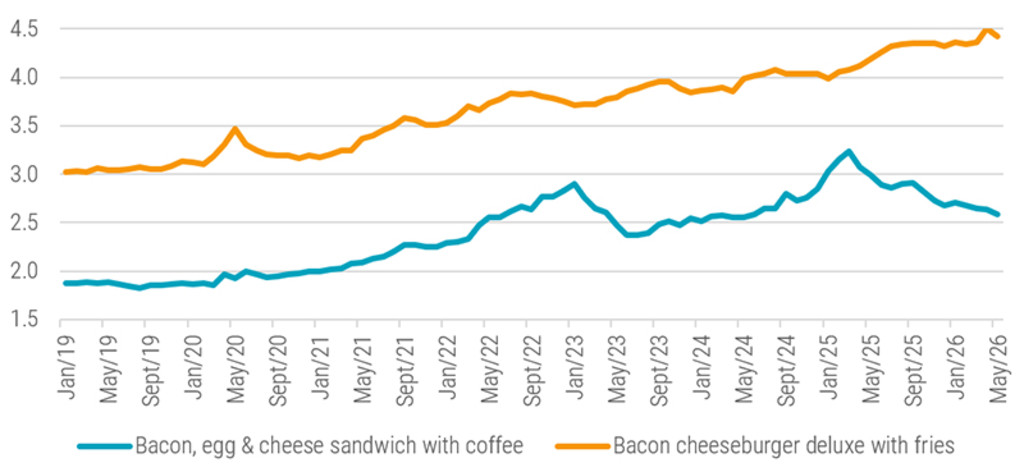

Los precios de artículos cotidianos dejan con la boca abierta a muchos consumidores a la hora de hacer la compra. Según el índice de precios de Bloomberg, pedir un bocadillo de beicon, huevo y queso con un café cuesta un 38% más (ha pasado de 1,87 USD en 2020 a 2,58 USD en 2026). El precio del menú de hamburguesa con queso «deluxe» con patatas fritas aumentó un 42% (ha pasado de 3,12 a 4,43 USD, como se ve en el gráfico 1). Estos «picos» explican por qué tantos consumidores se sienten más pobres a pesar de que la inflación en EE.UU. se ha moderado, pasando de un máximo del 9,1% en 2022 al 4,2% en mayo.

Gráfico 1: Índice de precios de las comidas más consumidas en EE.UU.

Fuente: Bloomberg, 2026.

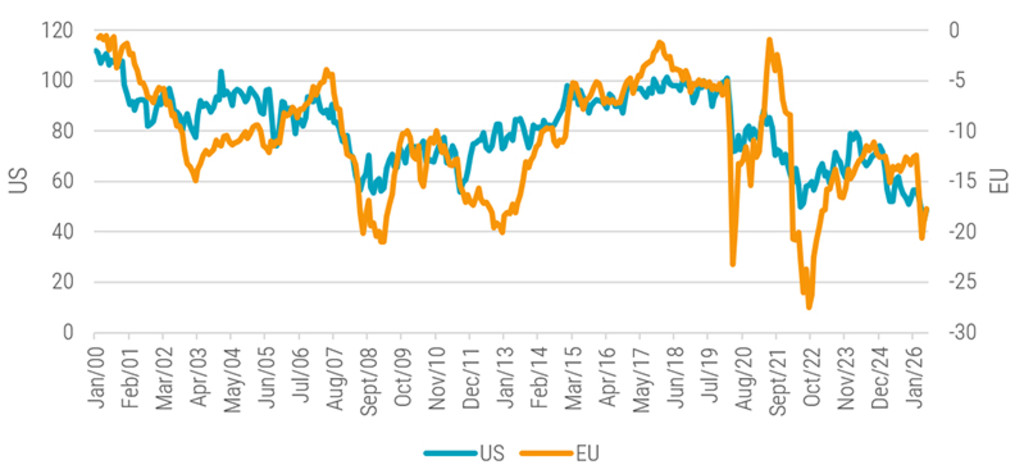

Es más, los hogares a ambos lados del Atlántico tienen la sensación de que están perdiendo poder adquisitivo. El índice del sentimiento de los consumidores de la Universidad de Míchigan (EE.UU.) cayó desde unos 100 puntos en 2020 hasta un nuevo mínimo histórico de 45 puntos en mayo; unos niveles que suelen asociarse a las recesiones. El sentimiento en Europa descendió de -12 en febrero a -18 en junio, lo que supone el mayor deterioro en un plazo de dos meses que se ha producido en muchos años (véase el gráfico 2).

Gráfico 2: Índice del sentimiento de los consumidores

Fuente: Universidad de Míchigan, Eurostat, 2026.

Hay que fijarse en lo que hacen, no en lo que dicen

Afortunadamente para los minoristas, el pesimismo que sienten los consumidores se ha visto compensado por la resiliencia del empleo y los ingresos. La cifra de desempleo en EE.UU. sigue siendo baja, del 4,3% (a fecha de mayo de 2026), de forma similar a como ocurre en otras economías principales, que también se sitúa dentro de un rango aceptable de entre el 2,5 y el 6%. Mientras tanto, las ventas al por menor siguen creciendo, lo que sugiere que existe una escasa relación entre el sentimiento de los consumidores y el consumo real. El aumento del volumen de pagos en EE.UU. así lo confirma, ya que se ha incrementado de aproximadamente un 9% hasta abril, frente al 7,5% registrado en el T1. A nivel global, dicho volumen creció un 9% en el T1, frente al 8% registrado en el T4, lo que refuerza la creencia de que hay que fijarse en lo que hacen los consumidores, no en lo que dicen (véase el gráfico 3).

Gráfico 3: El consumo al por menor repunta en la mayoría de las economías principales

Fuente: Oficina de Estadísticas Laborales de EE.UU. (BLS), Eurostat, Ministerio del Interior de Japón, Oficina Nacional de Estadística de China, Oficina Central de Estadística de la India, 2026.

Una paradoja en forma de K

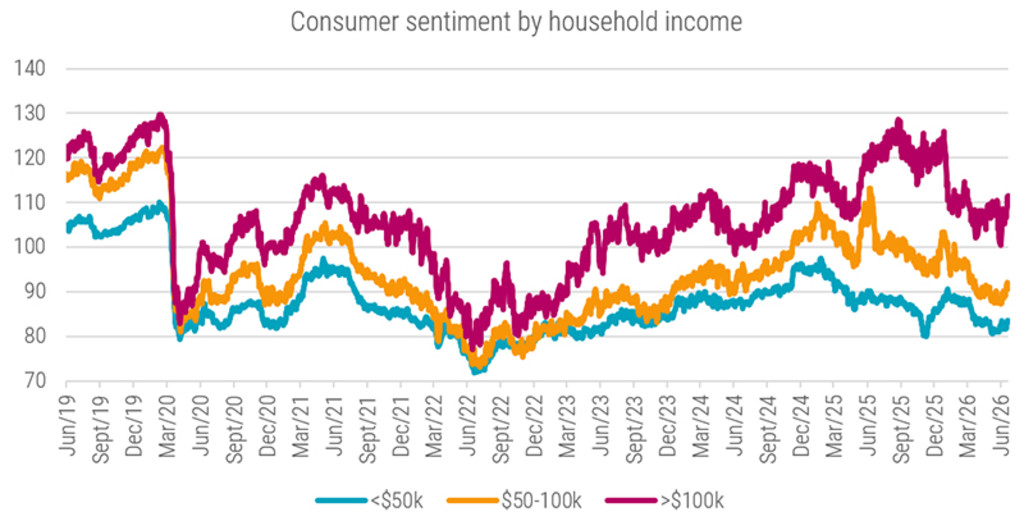

Los ingresos de los hogares con rentas más bajas están creciendo a un ritmo mayor en comparación con los ingresos de los grupos con rentas más altas; pero los primeros siguen gastando menos, lo que da lugar a una economía en forma de K. En consecuencia, las compañías deben dirigirse a dos públicos: los consumidores con mayor poder adquisitivo (que siguen estando dispuestos a pagar por la calidad) y los consumidores con un presupuesto ajustado (que necesita que bajen los precios de los productos de uso diario). Los datos de empleo de EE.UU. muestran que, desde principios de 2019 hasta la actualidad, los salarios reales (una vez descontada la inflación) han aumentado más entre las personas con ingresos más bajos que entre aquellas con ingresos más altos. Además, en todas las categorías de ingresos, dicho aumento superó la inflación. Al mismo tiempo, los datos sobre consumo ponen de manifiesto que la economía se divide en dos vías muy marcadas. Los hogares estadounidenses con mayores ingresos gastan más (entre un 5 y un 10%) desde principios de 2025, mientras que el gasto de los hogares con menos ingresos se ha ralentizado y, en algunos casos, se ha invertido.

Gráfico 4: El sentimiento de los consumidores diverge en los hogares con ingresos bajos respecto a los hogares con ingresos altos

Fuente: Morning Consult, Bloomberg, mayo de 2026.

Las agencias de viajes observan tendencias similares y señalan que los consumidores con mayor poder adquisitivo están gastando sin reparos en viajes, restaurantes y experiencias de lujo. La cadena hotelera de lujo Hyatt* ha señalado que la demanda de los clientes de gama alta ha sido excepcionalmente sólida durante el último trimestre, y ha aumentado aproximadamente un 7% en comparación con el año pasado. Los viajes en crucero, que se considera otro producto de lujo, también van viento en popa. Las dos mayores compañías de cruceros del mundo, Royal Caribbean y Carnival, han registrado cifras récord de reservas y precios, ya que la combinación de alojamiento, comidas y entretenimiento en una única tarifa se considera una buena relación calidad-precio en comparación con las vacaciones en tierra firme.*

Global Consumer Trends D USD

- performance ytd (30-6)

- 2,65%

- Performance 3y (30-6)

- 10,75%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Dividend Paying (30-6)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

El comportamiento de los consumidores se orienta hacia el valor

Los consumidores están cambiando de forma decisiva su comportamiento: cada vez les interesa más el valor y los costes de lo que adquieren. Aproximadamente el 75% de los hogares estadounidenses están optando por marcas y comercios más económicos, mientras que la mitad está posponiendo las compras no esenciales. Los consumidores también están reduciendo las salidas de ocio. Sin embargo, el precio no es el único factor que influye en las decisiones: además de buscar gangas, los consumidores acumulan puntos de fidelidad de sus marcas favoritas y se decantan por productos que les ofrecen un mayor valor percibido.

Los minoristas se están adaptando rápidamente a esta situación y los que ajustan el valor que ofrecen son, sin duda, los que más se benefician. Walmart* está apostando por la relación calidad-precio, por lo que, además de ofrecer precios más bajos, está ampliando su gama de marcas blancas y ofreciendo envíos en el mismo día. Las categorías de productos de uso diario y alimentación de Amazon también están creciendo rápidamente y, en la actualidad, representan una de cada tres unidades vendidas. Al igual que Walmart, Amazon* está aumentando el valor añadido gracias a la comodidad que ofrece su servicio de entrega en el mismo día de artículos a precios reducidos.

Los consumidores están cambiando de forma decisiva su comportamiento: cada vez les interesa más el valor y los costes de lo que adquieren. Aproximadamente el 75% de los hogares estadounidenses están optando por marcas y comercios más económicos

La popularidad de las marcas blancas también va en aumento, y se prevé que las ventas en EE.UU. alcancen la cifra récord de 283.000 millones de USD en 2025, lo que supone casi una cuarta parte del volumen de unidades vendidas. La marca Kirkland Signature de Costco* generó unas ventas anuales estimadas de 80.000 millones de USD el año pasado (una cifra superior a la de la mayoría de los minoristas globales). Se prevé que, para mediados de 2026, la generación Z destine una mayor parte de su presupuesto a marcas blancas que cualquier otra generación, lo que sugiere que este cambio es de carácter estructural y no cíclico. Los consumidores también buscan descuentos más sustanciales y acuden en masa a cadenas de tiendas de descuento como TJ Maxx, Marshalls, HomeGoods, Ross Stores y Burlington*, todas las cuales registran un crecimiento sólido.

Los productos de segunda mano también se han generalizado, ya que cada vez más consumidores que buscan una buena relación calidad-precio ya no asocian la «excelente relación calidad-precio» exclusivamente con los productos nuevos. La plataforma de comercio electrónico eBay* ha registrado un crecimiento de dos dígitos al atraer a compradores con mayores ingresos que se preocupan por la economía y la sostenibilidad. Las plataformas de reventa como Vinted, Depop y Poshmark* también han seguido creciendo hasta hacerse con una cuota del mercado de moda de segunda mano cuyo valor se estima que alcanzará los 350.000 millones de USD en 2028.

Los productos de segunda mano también se han generalizado, ya que cada vez más consumidores que buscan una buena relación calidad-precio ya no asocian la excelente relación calidad-precio exclusivamente con los productos nuevos

Los precios y las promociones también forman parte de la oferta en el sector minorista de la alimentación. McDonald’s* ha logrado recuperar a los clientes con bajos ingresos gracias al lanzamiento de sus menús McValue. Esta iniciativa les ha ayudado a recobrar el impulso en la mayoría de sus mercados. Taco Bell, Wendy's, Chipotle e incluso la cadena de comida rápida Panera han seguido sus pasos con sus propios menús económicos. Aunque muchas cadenas de comida rápida han mejorado su oferta en cuanto a la relación calidad-precio, siguen enfrentándose a retos. Dos de ellos son el hecho de que cada vez más personas comen en casa y el uso de medicamentos para adelgazar que reducen la ingesta calórica.

Lo que está claro es que las compañías mejor posicionadas para captar a los consumidores de hoy y de mañana se centran en: 1) generar confianza ofreciendo un valor constante, en lugar de recurrir a trucos promocionales a corto plazo; 2) invertir en características adicionales de los productos o servicios, de modo que «precio bajo» no sea sinónimo de «calidad baja»; y 3) comunicar la propuesta de valor desde el principio y con frecuencia.

* Las compañías mencionadas aparecen a efectos meramente ilustrativos para explicar la composición de la estrategia de inversión en la fecha indicada. Las compañías no pertenecen necesariamente a la estrategia ni se garantiza su inclusión en el futuro. No se trata de una recomendación de compra, venta o conservación, ni debe hacerse inferencia alguna sobre la evolución futura de las compañías.

Acceda a las perspectivas más recientes

Suscríbase a nuestro newsletter para recibir información actualizada sobre inversiones y análisis de expertos.