The Investment Engineers

¿Hora de diversificar más allá de EE.UU.?

Este artículo forma parte de una serie de tres entregas sobre inversiones cuyo objetivo es explorar alternativas regionales al crecimiento centrado en EE.UU.

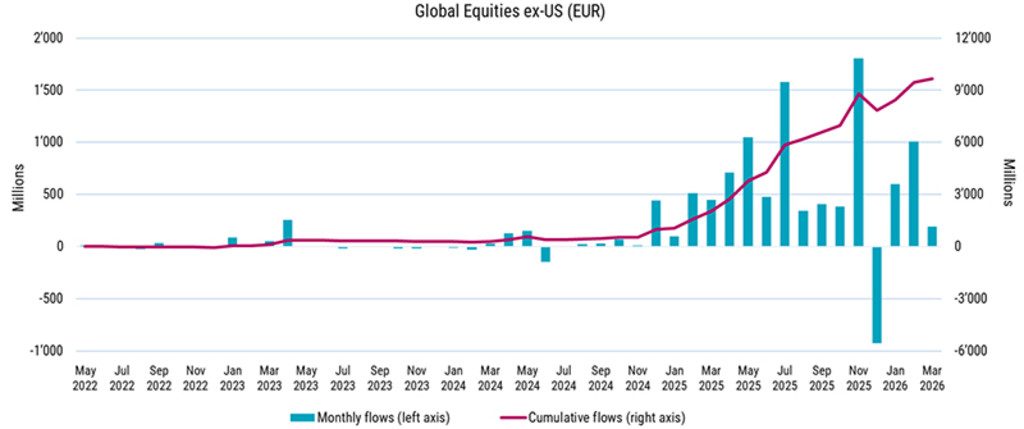

En los últimos 12 meses, ha comenzado a perfilarse un cambio entre los responsables de asignación de activos globales, que están redefiniendo el equilibrio regional de sus carteras de renta variable.

Tras más de una década de outperformance de la renta variable estadounidense, el capital se está reorientando gradualmente hacia un abanico más amplio de oportunidades en los mercados globales. Esto no se debe a una pérdida de confianza en EE.UU., sino al creciente atractivo de las oportunidades en otros lugares. Los mercados globales son cada vez más diversos en sus motores de rentabilidad. Las diferencias en la política, la estructura económica y la composición del sector están creando una mayor dispersión de los resultados entre regiones y compañías. En este entorno, el liderazgo es menos predecible y está más fragmentado, por lo que el acceso a un universo global más amplio es cada vez más importante.

Fuente: Broadridge y Robeco, mayo de 2026.

A su vez, el creciente dominio de los gestores de activos estadounidenses significa que una parte importante de la asignación global de capital está cada vez más influenciada por instituciones con sede en Estados Unidos. Ello puede reforzar el sesgo de origen y la aglomeración, dejando sin explorar las oportunidades en otras regiones.*

Para los inversores que buscan diversificación más allá de EE.UU., manteniendo a su vez la exposición al crecimiento regional y global, destacamos algunos de los enfoques de Robeco para captar este conjunto de oportunidades en expansión.

Robeco BP Global Premium Equities busca oportunidades de inversión en cualquier parte del mundo a valoraciones atractivas. A lo largo de la mayor parte de la historia de la estrategia, algunas de las oportunidades más atractivas se han encontrado en las compañías europeas. Como estrategia value, utiliza el enfoque de los «Tres círculos» de Boston Partners, de eficacia probada. Invierte en compañías que no solo estén infravaloradas por el mercado, sino que además tengan unos fundamentales comerciales sólidos y un fuerte momentum hacia adelante. Este proceso guía la construcción de la cartera, con el objetivo de buscar compañías que puedan generar alfa a lo largo del tiempo mediante el crecimiento de los beneficios y la expansión de los múltiplos.

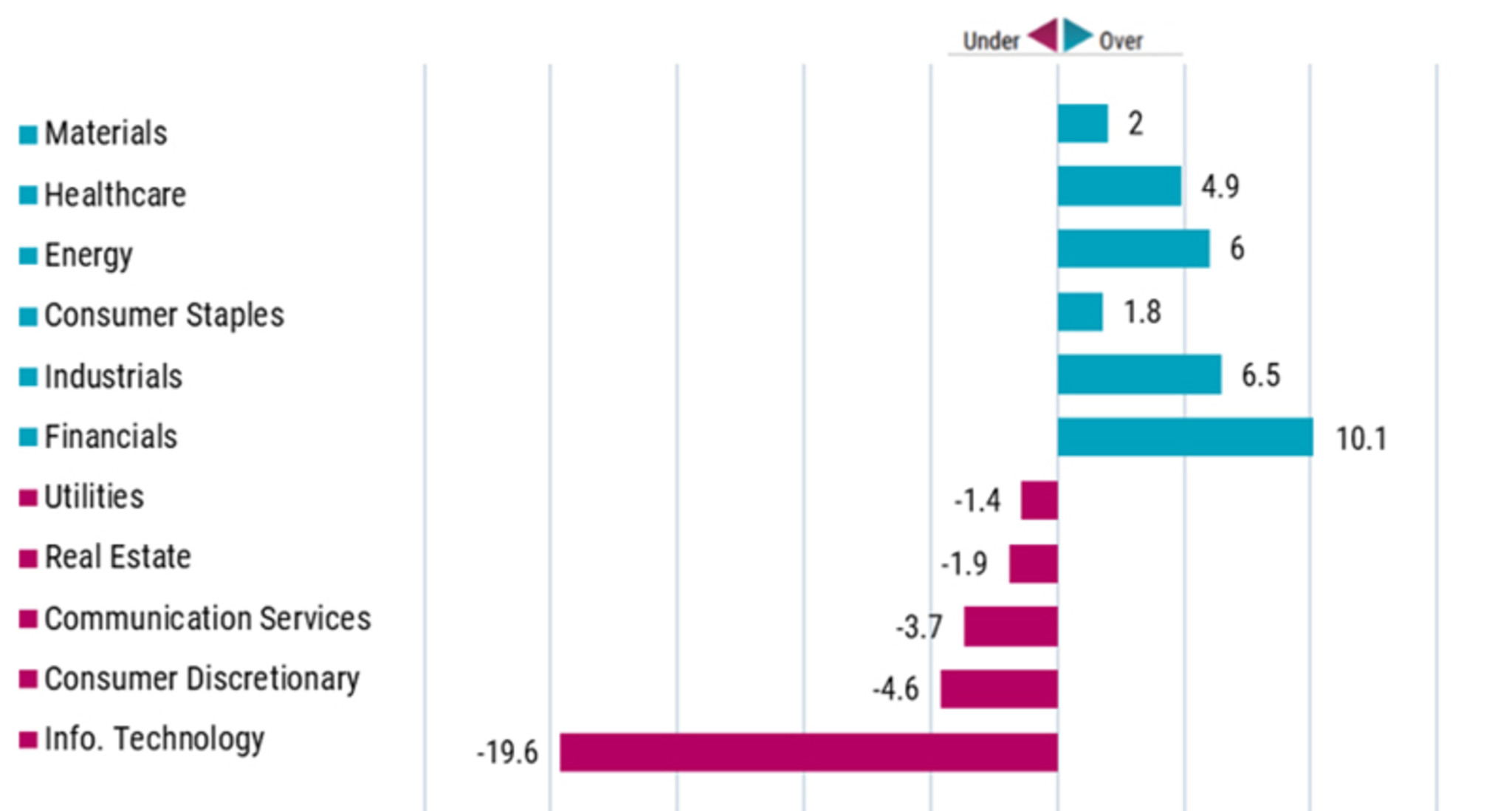

La disciplina de inversión de esta estrategia de renta variable global le permite invertir en todo el mundo. En los últimos años, la rentabilidad se ha visto impulsado en parte por las participaciones europeas, con dos áreas destacadas: bancos e industriales. Los bancos de la zona euro y otras instituciones financieras, como las aseguradoras, antaño deprimidas, han disfrutado de unos márgenes magníficos en medio de la subida de los tipos y de unas tasas de impago/reclamación de seguros inferiores a las de sus homólogos norteamericanos. Posteriormente, los bancos europeos han superado al índice de referencia más amplio desde que los tipos empezaron a subir desde cero en 2022.** Véase la Figura 2 para conocer las diferencias en las ponderaciones sectoriales entre la estrategia y el índice de referencia.

Fuente: Robeco BP Global Premium Equities, que refleja dónde está sobreponderada e infraponderada la estrategia frente al índice de referencia (MSCI World) a 31 de marzo de 2026. Se excluyen monetarios y el neto de otras inversiones. A efectos meramente ilustrativos. Este es el panorama actual en la fecha arriba indicada y no garantiza la evolución futura. No debe presuponerse que las inversiones realizadas en los sectores indicados hayan sido o vayan a ser rentables. Se utiliza la clasificación sectorial GICS. Todas las características de los productos y la ponderación sectorial se calculan utilizando una cuenta representativa frente al índice MSCI World.

Los industriales cuentan una historia similar, apoyados por el aumento de la inversión gubernamental y corporativa en activos reales y gastos de capital, particularmente en infraestructuras de IA y defensa. El desarrollo de la IA está impulsando el gasto a gran escala en nuevos centros de datos y en capacidad adicional de fabricación de chips. Además, la iniciativa «Plan ReArm Europe 2030», dotada con 800.000 millones de euros y destinada a contrarrestar a Rusia, está impulsando la inversión en el sector de la defensa, desde equipamiento —como tanques y armas— hasta infraestructuras terrestres y ciberseguridad. Aunque esta ola de gasto ha supuesto un impulso para las acciones industriales en los últimos meses, la cartera Global Premium lleva más tiempo con una sobreponderación significativa en Europa y el Reino Unido, lo que refleja el enfoque de la estrategia en la identificación de empresas con valoraciones erróneas.

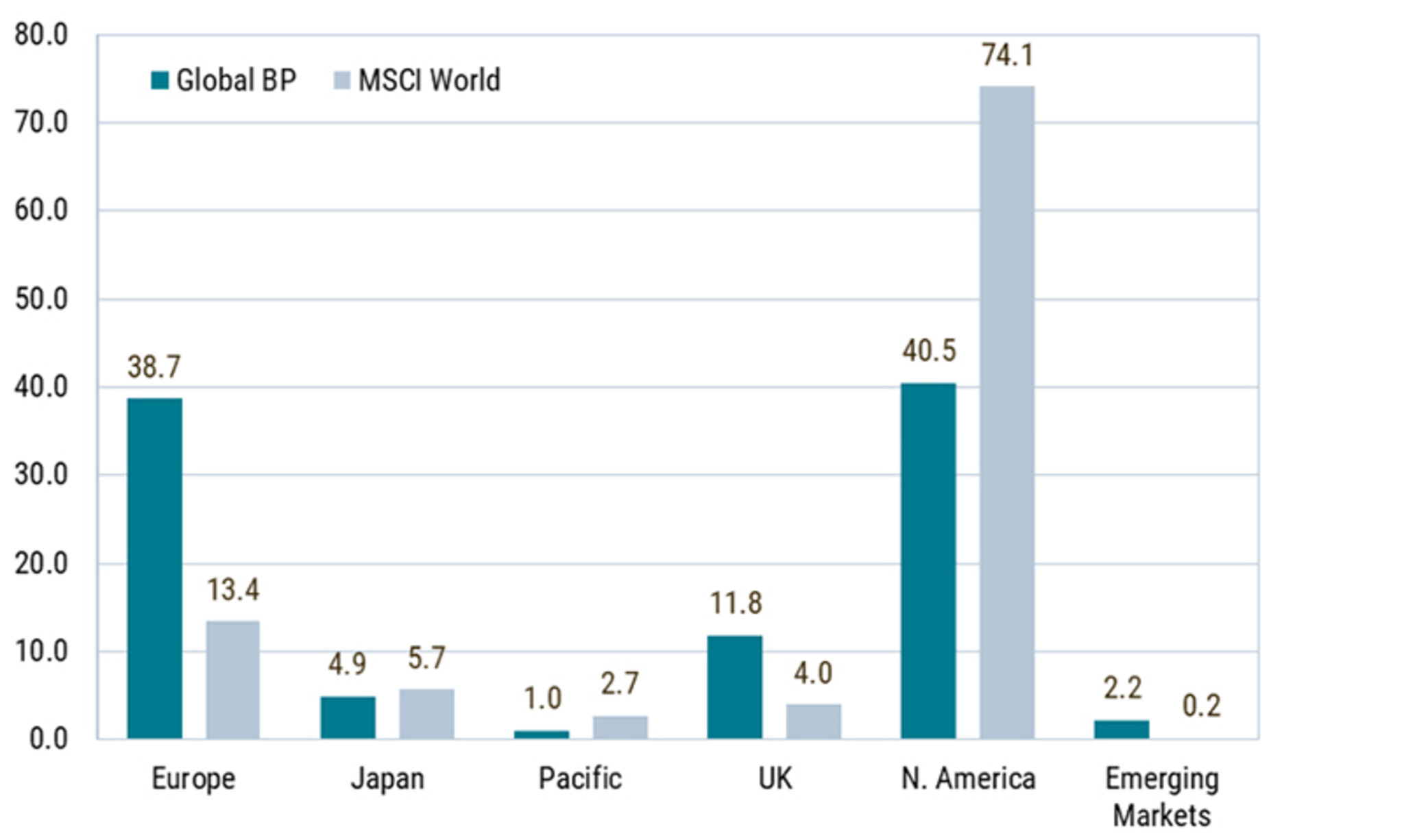

Como consecuencia, la exposición de la estrategia Global Premium a activos europeos ha aumentado del 13,4% al 38,7%, y en el Reino Unido del 4,0% al 11,8%, mientras que la exposición a Norteamérica ha descendido del 74,1% al 40,5%. Las diferencias en las asignaciones regionales entre la estrategia y el punto de referencia se reflejan en la Figura 3.

En conjunto, la estrategia ofrece un medio de diversificación fuera de EE.UU., a la vez que mantiene cierta exposición al mercado norteamericano, donde aún residen algunas oportunidades de valor.

Fuente: Exposición regional de Robeco BP Global Premium Equities (%) a 31 de marzo de 2026.

La renta variable temática se suele relacionar con un sesgo de crecimiento y con una fuerte presencia estadounidense. Sin embargo, las estrategias temáticas de Robeco siempre han tenido un universo amplio. Tratan de captar las mejores oportunidades de las tendencias a largo plazo que evolucionan a escala global, tanto en los mercados desarrollados como en los emergentes. Las estrategias «Smart» de Robeco —que incluyen Smart Materials, Smart Energy y Smart Mobility— ilustran a la perfección nuestro enfoque. Proporcionan exposición a un sólido crecimiento fuera de EE.UU., ya que los gobiernos y la compañía privada de regiones de todo el mundo tratan de aprovechar la transición energética, la electrificación del transporte y otros sectores, así como las tendencias de la IA y la expansión digital.

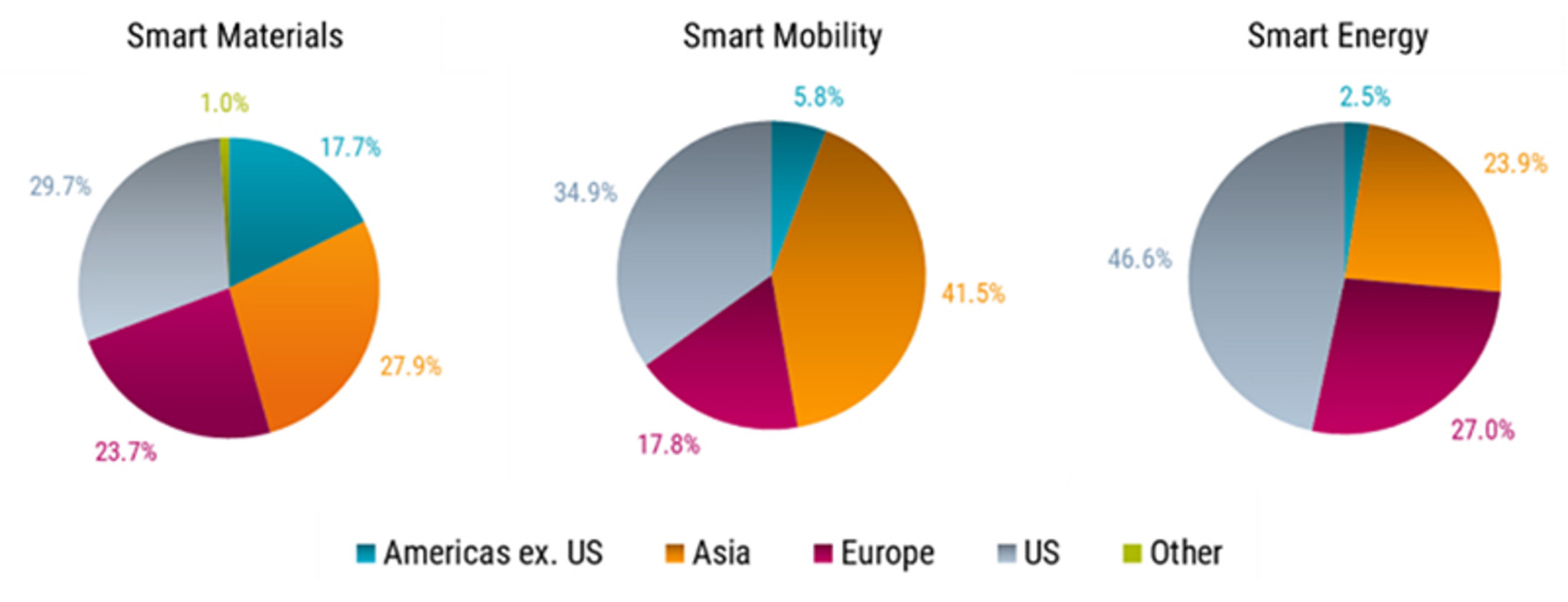

La estrategia Smart Materials invierte en materiales avanzados y en las cadenas de valor de la fabricación industrial en todo el mundo, sectores que están siendo transformados por la IA, la digitalización y las tecnologías de última generación. Capta la creciente demanda de metales de transición y minerales estratégicos, insumos esenciales para semiconductores, sensores infrarrojos, redes de fibra óptica, redes eléctricas e imanes de alto rendimiento utilizados en motores eléctricos y turbinas. Más abajo, la estrategia capta el crecimiento a través de los fabricantes industriales que suministran componentes para la electrónica avanzada, la automatización y la robótica. En conjunto, su exposición abarca la minería y el refinado en América, el procesamiento de especialidades y las tecnologías de automatización en Europa, y la fabricación de componentes y la infraestructura electrónica en Asia (véase la Figura 4 para las asignaciones regionales).

Fuente: Robeco. Abril de 2026. A efectos meramente ilustrativos. Se trata de la asignación regional actual para cada estrategia a 31 de marzo de 2026 y no de una garantía de evolución futura. No debe suponerse que las inversiones en las regiones identificadas vayan a ser rentables.

La estrategia de Smart Energy aprovecha las oportunidades que surgen en torno a la electrificación y a la transición energética en general que se está produciendo a escala mundial. Esto significa invertir en toda la cadena de valor de la «transición», desde la generación de energía y la infraestructura de la red eléctrica hasta la electrificación y las soluciones de eficiencia energética en las fases posteriores. La volatilidad de los precios de la energía y el afán por la seguridad energética están acelerando la inversión en energías renovables, mientras que la creciente demanda de electricidad derivada de la IA y la construcción de centros de datos está impulsando la expansión de la red. En conjunto, estas fuerzas están generando un amplio ciclo de inversión en los principales sectores de la estrategia, entre los que se incluyen la energía solar, la energía eólica, los productores de energía renovable, el almacenamiento en baterías, las infraestructuras de transporte, las redes eléctricas, así como los semiconductores de bajo consumo y los componentes electrónicos de potencia.

La estrategia Smart Mobility invierte en toda la gama de tecnologías que sustentan los vehículos eléctricos y la movilidad moderna, incluyendo chips, software, sensores, componentes de baterías y estaciones de recarga. Esos segmentos son cada vez más sofisticados y están cada vez más impulsados por la IA, lo que favorece el crecimiento de la conducción autónoma, la robótica y las tecnologías facilitadoras relacionadas. El aumento del coste del combustible, las restricciones a las emisiones y el menor coste de propiedad están acelerando su adopción global. Las cadenas de valor subyacentes son globales: las empresas europeas aportan la ingeniería de vehículos y los sistemas de seguridad e inteligencia; América Latina y Asia aportan el litio, las celdas de batería, los semiconductores, los sensores y la fabricación a gran escala; y las compañías norteamericanas aportan el diseño de chips, el software, los robotaxis y los servicios de transporte compartido.

Además de una exposición regional diversificada, las estrategias «Smart» de Robeco también presentan una marcada inclinación hacia las empresas de mediana capitalización, lo que se traduce en un active share elevado (normalmente entre el 96% y el 98%) con respecto al índice MSCI World. Ya sea a partir de la selección de tendencias o de valores, pueden ofrecer una alternativa diferenciada a la renta variable estadounidense al acceder a cadenas de valor dispersas por todo el mundo y fuertemente vinculadas al crecimiento estructural.

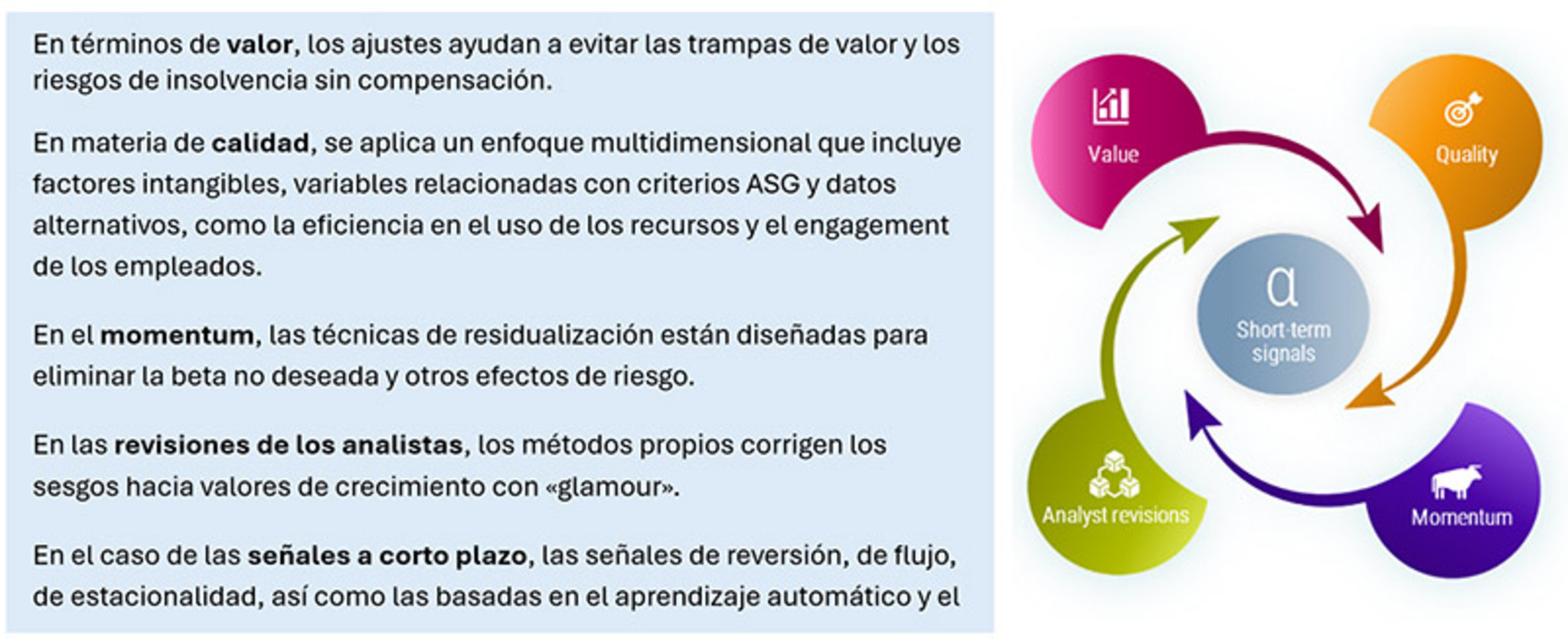

Las estrategias cuantitativas globales de Robeco están diseñadas para analizar amplios universos de inversión, identificar patrones y aplicar los conocimientos obtenidos de manera eficiente. En su núcleo se encuentra el modelo de selección de valores, construido en torno a un conjunto diversificado de señales alfa que evoluciona con el tiempo (véase la Figura 5). Mediante la combinación de diversas señales, nuestro modelo tiene como objetivo identificar de forma sistemática las oportunidades más atractivas, a la vez que se mantiene un estricto control del riesgo. Dentro de este marco, los inversores pueden acceder a las oportunidades globales de diferentes maneras, en función de sus objetivos.

La indexación mejorada está diseñada para los inversores que desean mantenerse cerca del índice de referencia en términos de riesgo global, a la vez que pretenden mejorar la exposición pasiva mediante una selección disciplinada de compañías. La indexación mejorada global opera dentro de unos márgenes de tracking error relativamente limitados y pretende ofrecer una ventaja estable después de costes, con características de riesgo absoluto similares a las del mercado, lo que la hace especialmente relevante para los inversores que buscan una asignación de renta variable global básica que pueda encajar de forma natural en las carteras que aplican políticas y marcos de riesgo existentes.

Para los inversores interesados en tracking error más amplio en busca de un mayor alfa, nuestro enfoque Active Quant en renta variable global sigue prestando atención al índice de referencia y teniendo en cuenta el riesgo, pero permite desviaciones más amplias cuando el modelo identifica oportunidades más sólidas. Eso crea un mayor margen para la generación de alfa sin dejar de mantener un marco disciplinado para el control y la aplicación del riesgo. Esto es importante porque los inversores cada vez son menos propensos a tener que elegir entre «ceñirse al índice de referencia» y asumir un riesgo activo sin restricciones. Quieren estrategias que puedan perseguir un alfa diferenciado sin dejar de ser transparentes, sistemáticas y disciplinadas.

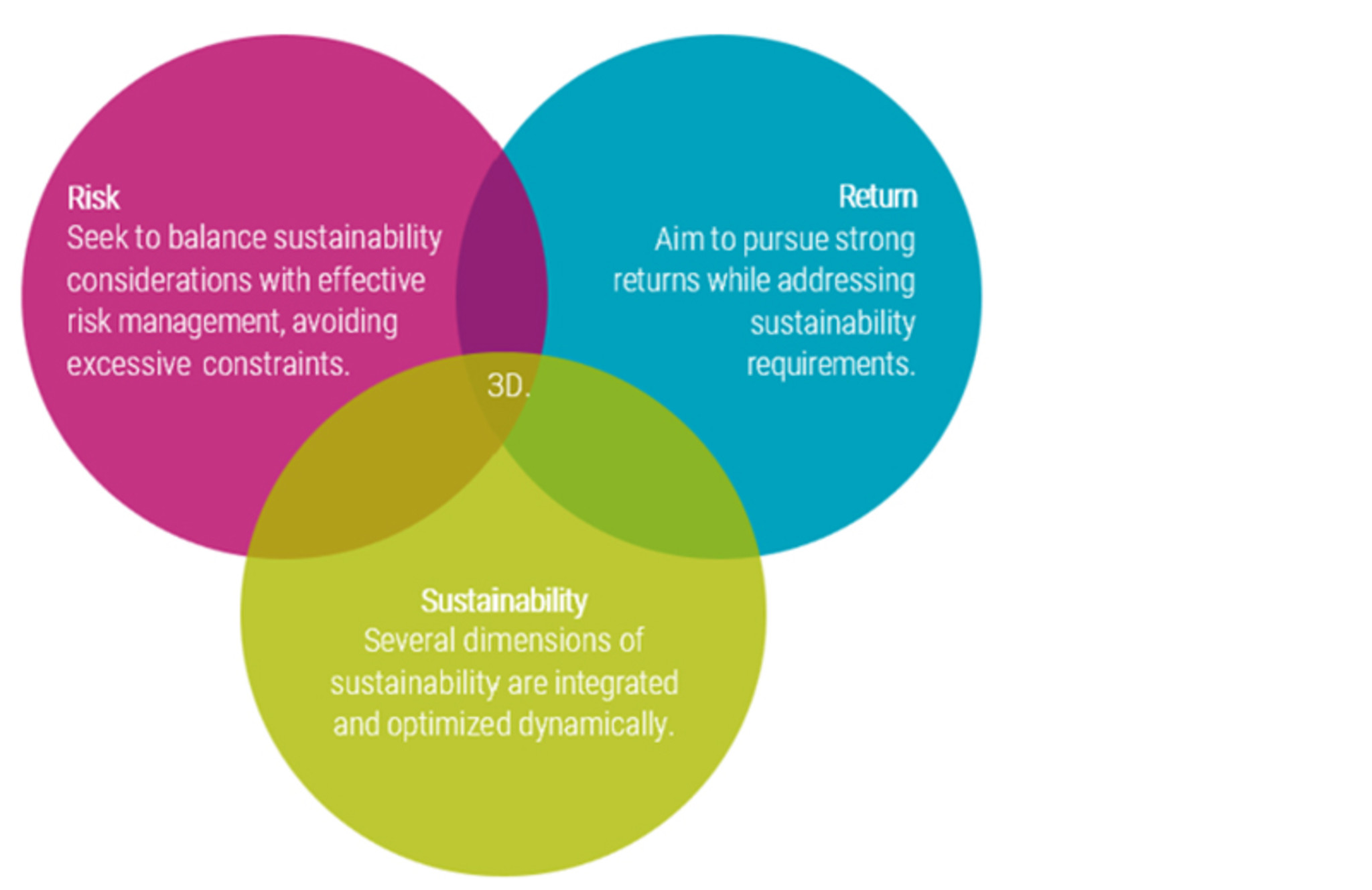

Para los inversores que priorizan la flexibilidad y la eficiencia en la inversión, este ETF activo ofrece una forma moderna de acceder a los mercados bursátiles globales. El marco 3D integra el riesgo, la rentabilidad y la sostenibilidad en un único proceso de construcción de carteras. En lugar de tratar estas dimensiones por separado, se consideran conjuntamente y se optimizan de forma dinámica. Al integrarse en una estructura ETF se obtiene una solución que ofrece transparencia, liquidez y rentabilidad, a la vez que proporciona un enfoque más equilibrado y con visión de futuro para la inversión en renta variable global.

A medida que el liderazgo de los mercados de renta variable muestra signos de ampliarse, los argumentos para mirar más allá de EE.UU. son cada vez más convincentes. Un enfoque global permite a los inversores acceder a un conjunto de oportunidades más amplio y dinámico, conformado por las diferencias entre regiones, sectores y regímenes económicos. Como se ha comentado aquí, ya sea a través de la inversión en valor activa, de estrategias temáticas específicas o de la inversión cuantitativa sistemática, los inversores disponen de múltiples formas de acceder a este panorama en expansión.

* Véase: https://www.bruegel.org/policy-brief/risks-europe-us-dominance-global-asset-management

** Las rentabilidades pasadas no son garantía de resultados futuros. El valor de su inversión puede fluctuar.

Este artículo forma parte de una serie de tres entregas sobre inversiones cuyo objetivo es explorar alternativas regionales al crecimiento centrado en EE.UU.