Strategist

• Visión

Por qué los inversores están diversificando ahora sus inversiones más allá de EE.UU.

Durante gran parte de los últimos 15 años, la inversión a nivel global parecía aparentemente sencilla: bastaba con mantener una mayor exposición a la renta variable estadounidense, especialmente a las acciones de gran capitalización y de estilo growth, para obtener una generosa recompensa en forma de rentabilidades superiores a la media histórica. Cuanto más duraba el ciclo, más se arraigaba ese posicionamiento, no siempre como una llamada deliberada, sino como un el efecto compuesto de los flujos hacia lo que seguía funcionando.

Autores/Autoras

Top keywords

Resumen

- La confianza en EE.UU. es arriesgada a medida que aumentan las valoraciones y la incertidumbre

- Las ajustadas ganancias lideradas por la tecnología aumentan el riesgo de concentración

- La diversificación aumenta la resiliencia de los activos

Hoy en día, la cuestión no es si EE.UU sigue siendo un mercado crítico. Lo es: sigue siendo el mercado de capitales más profundo del mundo, un ancla de liquidez global y un auténtico líder en innovación y en la carrera hacia la inteligencia artificial (IA). Con una capitalización bursátil del 72%, el mercado de renta variable estadounidense es difícil de evitar.

Sin embargo, con la pérdida de transparencia de las políticas económicas estadounidenses y el aumento de las inversiones en bienes de capital relacionadas con la IA, la cuestión más práctica es si el excepcionalismo estadounidense sigue siendo fiable y si las carteras se han vuelto demasiado dependientes de una fuente de rendimientos ajustada y cada vez más exigente.

Sigue leyendo aquí

De la observación a la suposición: Por qué se pone a prueba el régimen

Un riesgo clave de los largos períodos de liderazgo es que una observación de rentabilidad se convierta en una suposición de cartera. Por lo tanto, el sesgo de referencia abunda.

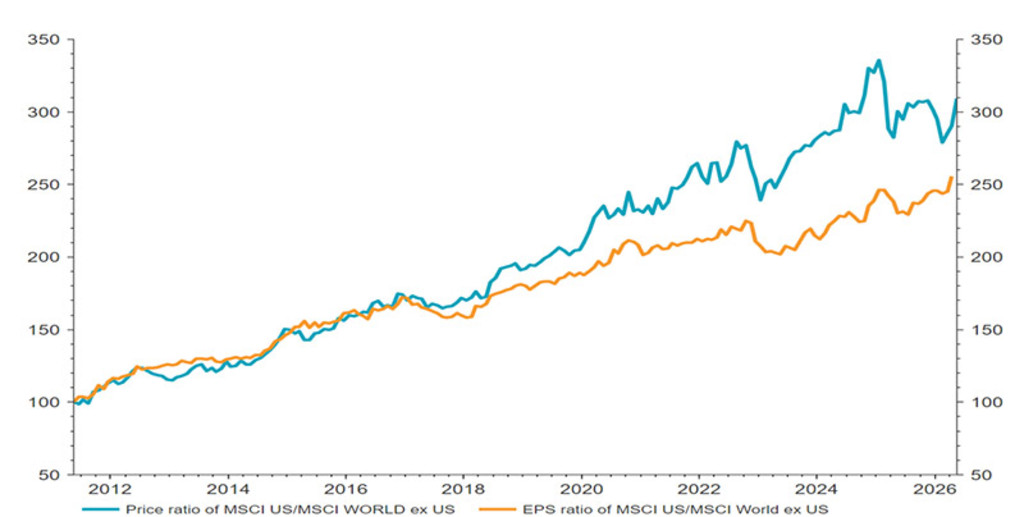

El debate está pasando de centrarse en «¿puede continuar el excepcionalismo estadounidense?» a preguntarse «¿en qué medida se ha descontado ya en los precios y qué otros factores deben salir bien para justificarlo, especialmente en lo que respecta a la capacidad del auge de las inversiones en bienes de capital relacionadas con la IA para generar una rentabilidad adecuada?». En los últimos 15 años, los inversores han estado cada vez más dispuestos a pagar para acceder a un rendimiento superior de los beneficios en EE.UU., como demuestra la rentabilidad relativa de los precios de las acciones estadounidenses, que ha superado el crecimiento relativo subyacente del BPA.

Gráfico 1: Dispuesto a pagar

En la última década, la rentabilidad relativa de los precios en EE.UU. ha superado su rendimiento superior en beneficios

Fuente: LSEG Datastream y Robeco, mayo de 2026

En nuestra opinión, la durabilidad del outperformance* continuado de la renta variable estadounidense depende cada vez más de un conjunto reducido de condiciones exigentes:

Aceleración continua de la productividad

Desinflación moderada, manteniendo los tipos oficiales lo suficientemente bajos como para compensar los elevados déficits públicos, y

Se mantiene la preferencia global por invertir en activos estadounidenses a pesar de la creciente inestabilidad política en ese país (es decir, el «privilegio exorbitante» sigue vigente).

En nuestra opinión, la probabilidad de que se cumplan las tres condiciones es del 60-70%, lo que deja un riesgo de cola significativo.

Además de estos riesgos macroeconómicos estructurales, en nuestro informe Expected Returns 2025-2029 señalamos que el sólido comportamiento del mercado bursátil estadounidense ha elevado los niveles de valoración, lo que conlleva un mayor riesgo de caídas, incluso aunque nos encontremos en una burbuja del tipo «vibrante» que aún tiene recorrido. En cualquier año natural, rara vez se alcanza la rentabilidad media estadística del mercado bursátil del 7% y, en el caso concreto de EE.UU., en este momento coexisten tanto un repunte significativo como un riesgo de caída.

Dado que la distribución de las rentabilidades esperadas de los activos estadounidenses analizados presenta colas más gruesas, la diversificación pasa de ser una virtud teórica a convertirse en una decisión práctica de gestión de carteras.

Un cambio estructural en la percepción del riesgo (y eso importa para las rentabilidades relativas)

Los mercados se interpretan a menudo a través de una lente cíclica. Lo que importa es el crecimiento, la inflación y la evolución de los tipos. Sin embargo, el actual telón de fondo se parece cada vez más a una transición estructural que podría cambiar las primas de riesgo. En muchos países, empezando por EE.UU., los riesgos para la seguridad (como las cadenas de suministro y los cuellos de botella en las importaciones y exportaciones críticas) han pasado a ocupar un lugar central, lo cual ha reducido el margen de maniobra del capitalismo laissez-faire, con los flujos de capital ajustándose en los márgenes. La política comercial estadounidense, la sostenibilidad fiscal y la postura geopolítica han vuelto a entrar en la conversación de un modo que en gran medida no lo habían hecho durante años.

Es importante destacar que la elevada incertidumbre de la política económica en EE.UU. en relación con el resto del mundo no apunta a una debilidad estructural de la economía estadounidense. Aun así, la mayor volatilidad macroeconómica resultante podría justificar un ajuste de las primas de riesgo estadounidenses (ya hemos visto un aumento de la prima a plazo del Tesoro estadounidense desde 2021). Los inversores que miran más allá de las salidas de EE.UU. pueden ver una recalificación de las valoraciones en el resto del mundo frente a un mercado estadounidense todavía caro, incluso cuando los valores de las Siete Magníficas han decaído recientemente.

Si bien EE.UU. sigue ocupando una posición dominante en el panorama económico global, sigue sin estar claro si el mercado está descontando adecuadamente la evolución cíclica. Observamos que el ratio CAPE del S&P 500 ya está descontando un crecimiento del PIB real del 2,9% para los próximos cinco años, casi un 1% por encima de la tendencia de crecimiento a largo plazo y unos 50 pb por encima de nuestra previsión de crecimiento a 5 años para la economía estadounidense. Ello sugiere que las expectativas implícitas en los precios de las acciones estadounidenses son difíciles de cumplir. En este contexto, la diversificación ya no consiste tanto en «predecir el punto máximo» como en mejorar la resiliencia de la cartera, identificando los riesgos a la baja y ampliando el abanico de oportunidades.

Riesgo de concentración: El liderazgo de EE.UU. es limitado

Otra característica de este ciclo es lo concentrado que ha estado el liderazgo: un pequeño grupo de compañías tecnológicas estadounidenses de gran capitalización y relacionadas con la IA ha generado una parte desproporcionada de la rentabilidad, reforzada por la mecánica de los índices y los flujos de inversión pasiva. Eso crea fragilidad. Si el «excepcionalismo estadounidense» se traduce progresivamente en un «excepcionalismo limitado», las carteras construidas en torno a esa concentración pueden resultar más vulnerables de lo que parecen. Los inversores han estado desproporcionadamente dispuestos a pagar más por la obtención de unos beneficios estadounidenses sólidos. Esa prima podría derrumbarse si el liderazgo de la IA fuera cuestionado en algún momento. La historia ofrece abundantes recordatorios de que el liderazgo dominante rara vez permanece incontestado: Standard Oil parecía una compañía magnífica hasta que las leyes antimonopolio la desmantelaron en 1911, mientras que la disolución de Northern Securities en 1904 demostró que incluso las combinaciones industriales y financieras más poderosas podían verse obligadas a separarse. La historia nos lo demuestra: el liderazgo cambia; no es cuestión de si sucederá, sino de cuándo.

Acceda a las perspectivas más recientes

Suscríbase a nuestro newsletter para recibir información actualizada sobre inversiones y análisis de expertos.

La cuestión de la burbuja: Por qué «vibrante» no es lo mismo que «explosiva»

Cualquier debate sobre la reasignación de activos fuera de EE.UU. se topa directamente con una preocupación legítima: ¿estamos simplemente sustituyendo una inversión con un fuerte impulso por otra alternativa más barata que carece del momentum necesario para generar valor?

En primer lugar, la diversificación debe ser una estrategia de gestión del riesgo de la cartera, no una operación contraria al momentum del mercado. Como destacamos en nuestro especial Expected Returns 2025-2029 sobre la historia de las burbujas, EE.UU. podría encontrarse en una burbuja vibrante, en la que las elevadas valoraciones podrían estar ampliamente justificadas porque los inversores anticipan acertadamente un crecimiento extraordinario vinculado a un cambio de paradigma en la economía real. Históricamente, alrededor de la mitad de las burbujas no estallaron. La burbuja de la IA también podría ser vibrante. En vez de infraponderar el momentum como factor, las carteras deberían evitar depender en exceso de un conjunto reducido de ganadores caros.

En segundo lugar, vemos signos de mejora del momentum en segmentos de renta variable baratos que se ignoraron durante gran parte de los últimos 15 años, en particular los mercados emergentes, las compañías small caps, la renta variable defensiva y el valor. Cabe destacar que no se trata de una única apuesta macroeconómica. Son un conjunto de oportunidades distintas con diferentes impulsores de rentabilidad, exactamente lo que debería ser la diversificación. Se debe subrayar que las reasignaciones colectivas fuera de EE.UU. no necesitan ser grandes para tener un enorme efecto positivo de rentabilidad en los mercados más pequeños. El oro, y más recientemente el mercado de renta variable coreano, son ejemplos de este fenómeno.

Diversification is not just an equity story

Las carteras multiactivos se diversifican también a través de los tipos, el crédito y las materias primas. En las semanas posteriores al «Día de la liberación», el 2 de abril de 2025, la correlación entre la rentabilidad de la renta variable y la de los bonos del Tesoro estadounidense a largo plazo pasó de ser negativa a positiva. Mientras tanto, la correlación entre las rentabilidades de los bonos del Tesoro estadounidense a largo plazo y el oro se volvió negativa. Aunque históricamente se han considerado un depósito de valor fiable, los últimos acontecimientos han puesto de manifiesto su vulnerabilidad, especialmente en los bonos del Tesoro estadounidense a largo plazo.

En algunos casos, las rentabilidades de los bonos corporativos estadounidenses con IG se han situado por debajo de los rendimientos comparables de los bonos del Tesoro estadounidense. Los inversores que no sean capaces de predecir la naturaleza de la próxima crisis quizá deban adoptar un enfoque diversificado hacia los activos refugio. Desde que los bonos del Tesoro de EE.UU. han pasado de ser un «sector refugio» a encontrarse en «aguas turbulentas», los bunds alemanes, la renta variable defensiva, el oro, las materias primas, las divisas fiduciarias e incluso el crédito pueden ofrecer una mejor protección durante el próximo episodio de turbulencias en los mercados. Sin embargo, para un inversor en euros, los bonos del Tesoro estadounidense con cobertura siguen ofreciendo un valor atractivo a medio plazo. Para los inversores en deuda pública japonesa, la opción más clara es quedarse en casa.

Mantener las acciones estadounidenses y reflexionar detenidamente sobre el mercado de divisas

En conclusión, EE.UU. puede seguir siendo una asignación importante mientras los inversores amplían su exposición a un conjunto de oportunidades globales más amplio y con valoraciones atractivas. Hacerlo con disciplina, en lugar de intentar sincronizar los cambios en la dirección, podría dar sus frutos.

Aunque se mantenga la exposición, un inversor que opere en euros y reduzca su dependencia de EE.UU. podría tener que replantearse su estrategia cambiaria. Desde la perspectiva de un inversor indiferente ante el riesgo y sin una opinión activa sobre el tipo de cambio EUR/USD, observamos que la cobertura «óptima» en acciones, dadas las correlaciones y las estimaciones de riesgo actuales, se sitúa en torno al 30%. El riesgo para el dólar no reside en el desplazamiento por parte de sus rivales ni en su capacidad para actuar como «sector refugio» durante las crisis internacionales, sino en la erosión interna provocada por el predominio fiscal, la disminución de las propiedades de cobertura de los bonos del Tesoro y la menor escasez de activos seguros.