Researcher

• 市場觀點

Quant chart: alternative peer groups

We use data on analyst coverage to identify firms followed by the same analysts and categorize them as being related peers. From this we can then create a network of connected companies. This is because our research1 shows that standard sector or industry classifications can be a crude proxy for determining fundamentally linked companies.

Identifying which stocks are peers of each other is of great importance to financial research and applications because it allows for an apples-to-apples comparison of companies and the potential exploitation of information spillover effects. The traditional way of grouping similar firms together is based on standard sector or industry classifications such as GICS or SIC codes. While these are useful as a starting point, they sometimes fail to spot homogenous groups of fundamentally related companies.

For instance, Apple and HP are both in the technology hardware and equipment retailing industry group and are arguably economically linked firms. Apple, on the other hand, is also part of the FAANG collection of stocks, but it falls within a different industry group or even sector compared to its Silicon Valley counterparts.2

Alternative peer groups have been proposed in the academic literature based on firms in the same geographic region,3 customer-supplier data,4 textual similarities in companies’ 10-K business descriptions,5 or comparable technologies based on patent data.6

More recently, Ali and Hirshleifer illustrated the efficacy in linking peers based on shared analyst coverage.7 This approach could be superior for several reasons. Firstly, the shared analyst network makes use of analysts’ human intelligence. Not only is it the analyst’s job to gather all relevant information about fundamentals such as information about related firms, customers, suppliers and competitors; an analyst is also more likely to adapt to changing market conditions than relatively static industry classifications.

Secondly, analyst linkages can uniquely identify connected company pairs rather than linking all firms within a sector, industry or a region. Similarly, analysts can also determine linkages beyond industry and geographic classifications, meaning that a company can be linked to firms both within its own but also outside its sector. Thirdly, the number of shared analysts can serve as a proxy for the strength of the relationship because not all relationships within the same region or sector will be equally important.

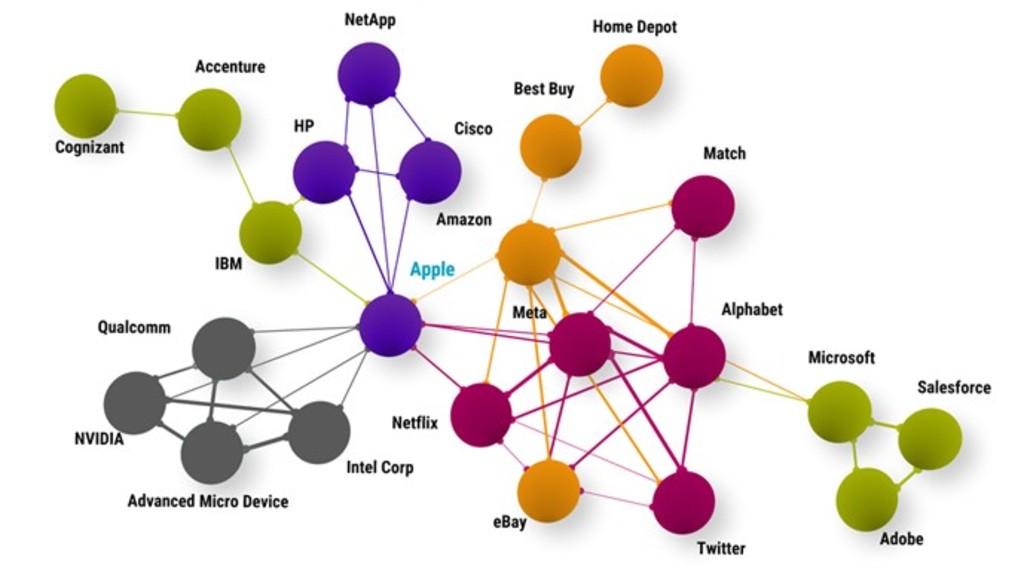

Figure 1 | Analyst-based company network for Apple

Source: I/B/E/S, Refinitiv, Robeco. For illustrative purposes only. The figure shows a simplified analyst network of connected firms for Apple as of September 2022. Two firms are connected when the same analyst covers them. The more analysts cover a pair of stocks, the thicker the line between them. The different colors indicate different GICS industry groups.

Figure 1 visualizes the connected company networks based on shared analyst coverage for Apple. The different colors represent different GICS industry groups. Classic information technology firms such as HP (technology hardware and equipment, purple), IBM (software and services, green) and Intel (semiconductors and semiconductor equipment, grey) are connected with Apple via shared analysts. However, we also observe that FAANG stocks from other sectors such as Meta Platforms, Alphabet, Netflix (all media and entertainment, pink) and Amazon (retailing, orange) are also closely related to Apple.

Therefore, we can conclude that the shared analyst coverage approach is an alternative and adaptive way to identify relevant firm peers.

Footnotes

1 Hanauer M. X., and Huisman R., October 2022, “Shared analyst momentum: extracting signals from connected company networks”, Robeco article.

2 Meta Platforms (formerly known as Facebook), Netflix and Alphabet (formerly known as Google) are in the ‘media and entertainment industry group which falls under the communication services‘ sector. Amazon is in the retailing industry group which falls under the consumer discretionary sector.

3 Parsons, C. A., Sabbatucci, R., and Titman, S., October 2020, “Geographic lead-lag effects ”, Review of Financial Studies.

4 Cohen, L., and Frazzini, A., August 2008, “Economic links and predictable returns”, Journal of Finance.

5 Hoberg, G., and Phillips, G., October 2010, “Product market synergies and competition in mergers and acquisitions: a text-based analysis” The Review of Financial Studies; and Hoberg, G., and Phillips, G., October 2016, “Text-based network industries and endogenous product differentiation” Journal of Political Economy.

6 Bloom, N., Schankerman, M., and Van Reenen, J., July 2013. “Identifying technology spillovers and product market rivalry”, Econometrica; and Lee, C., Sun, S. T., Wang, R., and Zhang, R., June 2019, “Technological links and predictable returns”, Journal of Financial Economics.

7 Ali, U., and Hirshleifer, D., June 2020, “Shared analyst coverage: unifying momentum spillover effects”, Journal of Financial Economics.

Quant Charts

重要資料

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。