Head of Sustainability Integration

了解最新的可持續性市場觀點

訂閱我們的電子報,探索塑造可持續投資的趨勢。

Climate change is the problem, net zero is the goal, and decarbonization is the means. But are there obstacles blocking the road ahead? Masja Zandbergen, Robeco’s Head of Sustainability Integration, explains the caveats and challenges that may trip up investors in their quest to decarbonize portfolios and contribute to the net zero transition.

“Put simply, it is reducing the carbon intensity of the portfolio by including companies with low emissions or which have made credible commitments to reduce their emissions. Similar to a portfolio’s financial performance, progress in this area requires continuous measurement against a reference point. Otherwise, the informational value of reported emissions is low. That reference could be the overall market, such as the emissions performance of a global index, or an internal standard such as a point in time from which a portfolio’s year-on-year progress is measured. The emissions amount is irrelevant; what matters is that you start to measure.”

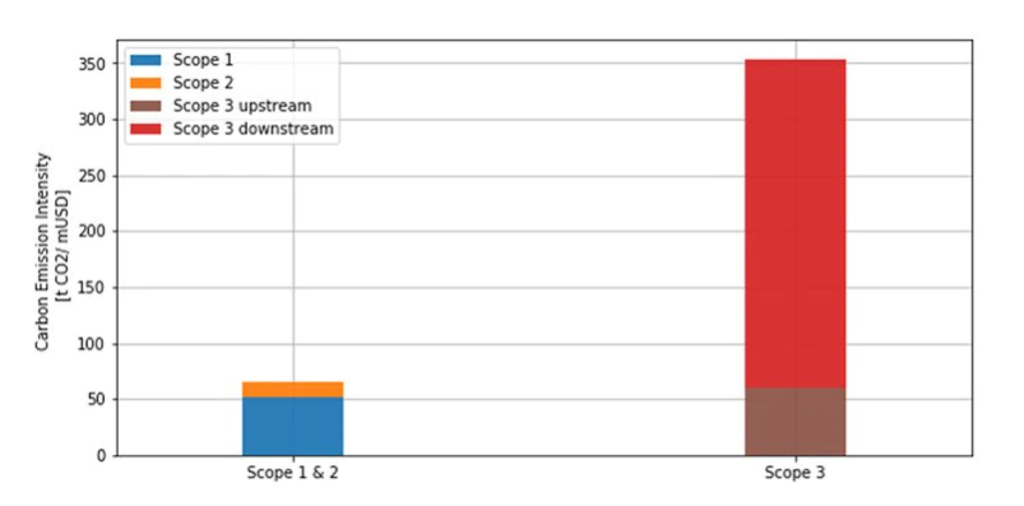

“It would be if company-reported data were complete, but the bulk of emissions generated is excluded from this, so true emissions performance is underestimated. Currently, companies report and investors measure emissions from production processes (Scope 1) and the electricity used to power those processes (Scope 2). But they don’t report emissions generated further along in the supply chain by a product’s consumers. Oil and gas producers have a high carbon footprint in the production phase, but that’s still only 20% of total emissions. The other 80% is generated when the oil is burned by customers (Scope 3).”

“Oil and gas companies aren’t alone; economy-wide scope 3 emissions are underestimated. Many food companies, for example, have comparatively low operational footprints upstream, yet hefty unaccounted emissions from things such as deforestation and fertilizers in other parts of their supply chains. Comprehensive supply chain data is not yet calculated, publicly disclosed or considered by most investors (see Figure 1).”

Source: Robeco, Trucost

The graphic shows the annual weighted average carbon intensity (WACI) of constituents of the MSCI All World AC. Constituent emissions data are based on average annual emissions reported by companies for 2019. WACI measures the carbon intensity (Scope 1 + 2 + 3 emissions / enterprise value including cash in millions USD) for each portfolio company multiplied by its portfolio weight.

“It can lead to the emissions of some companies and sectors being underestimated or overestimated. Many ‘green and clean’ solution providers have paradoxically high carbon emissions if you only take backward-looking emissions into account. For example, wind turbine operators, electric vehicle makers and hydrogen producers, are all clean technologies but their carbon-reducing benefits lie in the consumer use phase further down the supply chain. Given they may need steel for parts or use electricity from a carbon-intensive regional power grid, their Scope 1 and 2 emissions may still be high. That means their decarbonization potential is not being fully realized in portfolios. Predictive power is needed to combat this effect.”

Many ‘green and clean’ solutions providers have paradoxically high carbon emissions if you only take backward-looking emissions into account Masja Zandbergen-Albers

“Our most advanced decarbonization strategies take Scope 3 emissions into account. For other strategies, we use proprietary estimation techniques and third-party modelling to derive best case estimates of future emissions. This involves mapping out net zero transition pathways for sectors based on available or near-term technologies. Besides Scope 3 emissions, we incorporate other types of forward-looking data to help predict companies’ climate preparedness and future climate-adjusted performance. Which companies have strategic plans that incentivize a shift to low-carbon technologies and business models? How are they expected to benefit and profit from the net zero transition? Which are financially strong enough to make the capital investments needed to transition?”

“The ultimate goal is to ensure client portfolios are climate proof by reducing their exposure to carbon risk and ensuring they are climate-ready. This is a much more complex responsibility, involving many more considerations than how a portfolio measures up against a benchmark in terms of emission reductions.”

Ensuring a portfolio is climate ready is more complex than measuring [carbon] reductions Masja Zandbergen-Albers

“ESG integration brings more information across a wide range of risk factors; social, economic, governance and environmental. This can be combined with financial analysis to more accurately assess future risks, evaluate financial performance and make better-informed investment decisions.”

“Decarbonization, on the other hand, is often done to reduce climate risks as well as to combat climate change. An investor’s decision to decarbonize their portfolio is not always based on purely financial objectives. Often, it is motivated by a desire to invest in companies that are making positive impact by not contributing to climate change and environmental damage.”

“The economy grows where capital flows, so channeling capital towards companies with strong carbon reduction momentum and away from laggers accelerates the transition to a carbon-free global economy. That said, selling the securities of a high carbon emitting company has no immediate effect on the real economy. Real world impact requires large pools of investors to ‘vote with their feet’ by refusing to own securities of heavy polluters. This will ultimately raise their financing costs and expedite change.”

“However, there are caveats to this approach. For one, denying financing will hurt many companies that want to transition but need capital to do it. In addition, some heavy polluters are so cash-flow rich, they don’t need new capital. In the latter case, financing boycotts may have little effect. But even cash-rich companies care about their reputations, so if investors position their portfolios away from these companies, it sends an amplified, high-alert message to company management.”

“Investors must also use active engagement and voting as a tool to exert their influence over company management. Given that carbon emissions are spread across entire economies and require major structural changes, engagement needs to take place not just with the company but also at the country level. Robeco has recently started engaging with country leaders to help them understand the aggregate effects of conflicting carbon policies at the national level. It is counterproductive to force some industries to decarbonize while allowing others to cut down forests or to offer protective subsidies to heavy carbon polluters. Country leaders must also understand that national decarbonization policies will impact their ability to attract global businesses, foreign investments and financing via sovereign bonds.”

訂閱我們的電子報,探索塑造可持續投資的趨勢。

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。