Portfolio Manager

• 市場觀點

Meet the many trends shaping the future of commerce

Ecommerce benefited significantly from the Covid-19 shock. While mobility restrictions kept consumers away from traditional brick and mortar shops, online shopping adoption surged across geographies and age groups. But the great acceleration seen in 2020 is only one of the many changes shaping global consumer spending. Other sweeping developments are also redefining the future of commerce and the long-term winners of the digitalization trend.

概要

- Rising online sales is just one of the trends shaping the future of commerce

- Many consumer habits begun during pandemic are likely to stick

- We discuss some key recent developments in the retail sector

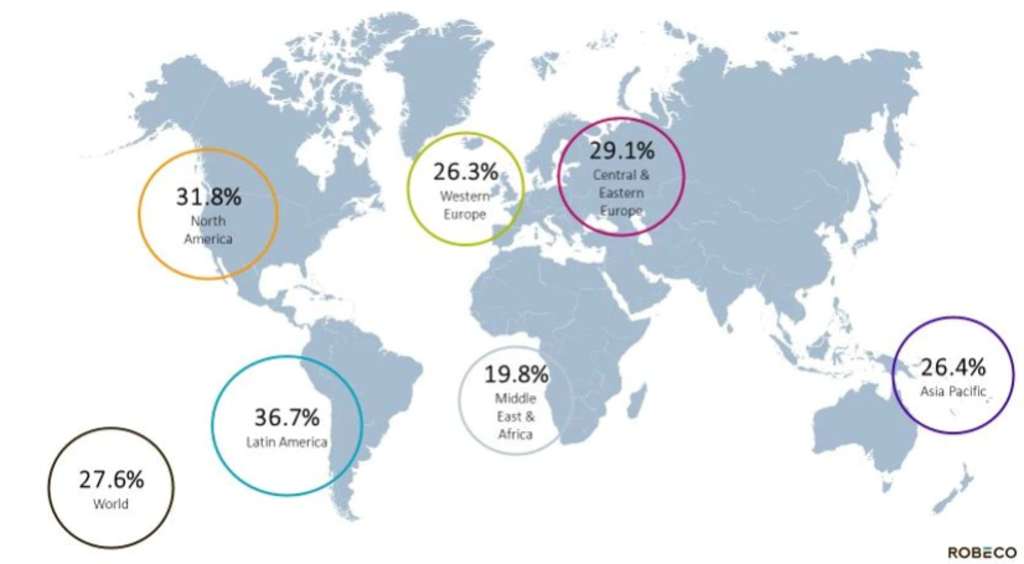

The Covid-19 pandemic triggered a broad-based global surge in digitalization, most dramatically in retail distribution. At the beginning of the first wave people stockpiled basic goods like toilet paper and items with a long shelf life like dried pasta. But as it became clear that the mobility restrictions would remain in place for longer than anticipated, consumers gradually started to change their purchasing behavior, moving online like never before (see Figure 1).

Figure 1: Retail ecommerce sales growth in 2020 by region

Source: eMarketer, Robeco, January 2021.

One key reason behind this surge is new cohorts joining the online ranks, in particular among older generations. People aged 65 and over were the fastest growing segment in terms of online spend last year in the US, according to NPD, a data and analytics firm.1 The array of goods bought regularly online also expanded. A recent survey by audit and consulting firm PwC showed no less than 53% of global consumers were now shopping fashion goods “more or exclusively online” versus in-store.2

Another notable catalyst of ecommerce adoption has been the dramatic rise of so-called ‘social commerce’, an ecommerce modality essentially driven by social networks. Social commerce typically includes sharing recommendations, discounts, games, and other types of content. This has been especially the case in China, where already increasing use of social commerce was further boosted by a spectacular boom in online community group-buying.

These shifts in consumer spending seen during the pandemic are expected to persist going forward, even as economies fully reopen and public health measures, as well as mobility restrictions, are gradually lifted. Despite renewed optimism from rapid vaccination campaign progress, safety concerns remain top of mind for customers. Only 59% of global consumers said they felt safe shopping in-store, according to recent data3 from Deloitte, another audit and consulting company.

But while the Covid-19 outbreak may have dramatically accelerated the digital transformation and propelled ecommerce to new heights, it has certainly also increased competition. For instance, many traditional brick and mortar wholesalers and retailers suddenly found themselves with their backs to the wall in the early stages of the pandemic, forced to move online in order to survive the crisis. Doing so, they started competing even more directly with more established ecommerce specialists.

The most explicit sign of rising competition within the ecommerce arena is the emergence of a series of regional champions. While Amazon may be the undisputed leader at global level, these regional champions are now increasingly in the driver’s seat in many countries. MercadoLibre in Latin America and Shopee in South East Asia are only two examples. Meanwhile, Alibaba dominates in China but nimble competitors like JD.com and Pinduoduo are catching up rapidly.

While ecommerce penetration into groceries had been lagging most other retail sectors, the outbreak suddenly knocked down many of the barriers to consumer uptake

Ecommerce expands into underpenetrated segments

Besides the general surge in ecommerce activity and competition, another key development has been the strong boost in online take-up seen for segments that remained relatively underpenetrated before the pandemic. Groceries is by far the most telling example. While ecommerce penetration into this segment had been lagging most other retail sectors, the outbreak suddenly knocked down many of the barriers to consumer uptake that had been hindering its expansion around the world.

But groceries were not only relatively underpenetrated segment to witness such a move. Non-essential items, such as fashion goods, health & beauty products and sports & fitness equipment, also experienced a strong rise in popularity from online shoppers.4Even pet care products moved online swiftly. Ecommerce specialists, saw their sales grow rapidly last year, as demand for pet products rose and as they gained market share.

A hybrid mix of on and offline shopping

In this context, the role of physical stores has been widely called into question, given the potential savings involved. However, what appears to emerge from current debates within the retail industry has more to do with an evolution than an outright demise of brick and mortar stores. For all the fuss around online shopping gradually displacing traditional commerce, customers still prize human interaction and physical shops.

Survey after survey, global consumers indicate that the convenience of the shopping experience remains crucial and that online cannot fully replace physical stores. In fact, data from the Adyen payments platform, a payments services company, also suggests that companies able to successfully integrate physical and digital commerce fared better than their pure-play counterparts during the pandemic.5 Therefore, the future of commerce will most likely be a mix of on and offline shopping.

Although actual consumer spending may not always reflect consistent behavior in this regard, awareness of the need to shift towards more sustainable consumption habits has now become widespread

Sustainability takes center stage

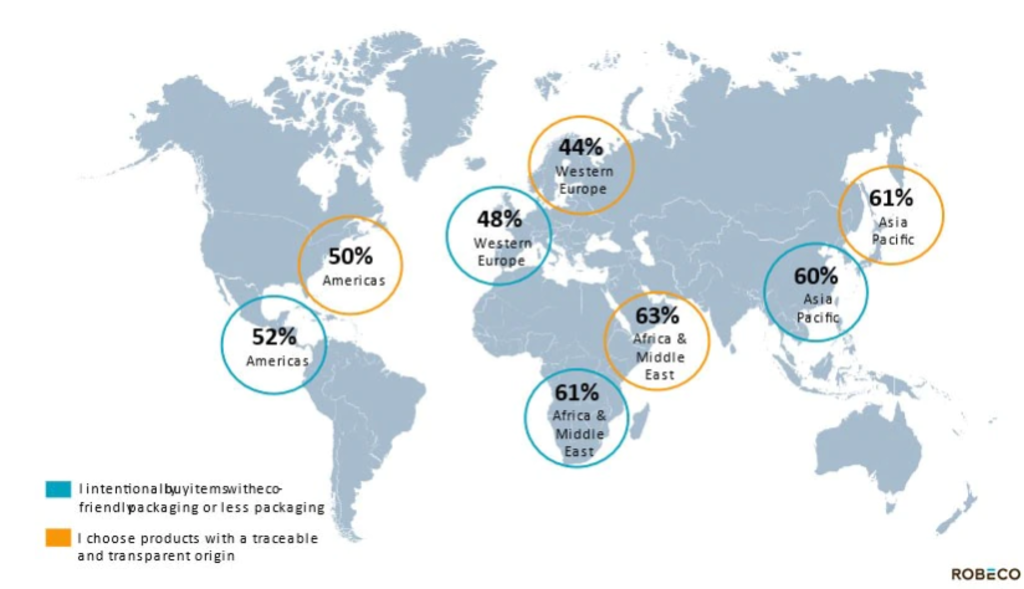

The emergence of companies such as Shopify also illustrates another phenomenon: the rise of the sustainable e-consumer looking for healthier, locally produced, locally distributed, and environmentally friendly products. Although actual consumer spending may not always reflect consistent behavior in this regard, awareness of the need to shift towards more sustainable consumption habits 6 has now become widespread. (see Figure 2)

Figure 2: Propensity to buy more sustainable products

Source: PwC Global Consumer Insights Pulse Survey, March 2021. Question asked: “Please indicate to what extent you agree or disagree with the following statements around shopping sustainability.” Net: Agree.

For example, the recent PwC consumer survey suggested that 55% of respondents were willing to pay more for healthier food and 50% of them were ready to pay more for locally produced groceries. As much as 46% said they would be ready to pay more for sustainable packaging.7 Interestingly, the survey also showed a gap between consumers working from home and those working away from home, with the former being more likely to prioritize sustainable products than the latter.

Footnotes

1Across retail (including grocery and general merchandise) shoppers aged 65 and over made 15% of their purchases online between January and October 2020, up from 10% in 2019, according to NDP Checkout data.

2Source: PwC Global Consumer Insights Pulse Survey, March 2021.

3Source: Deloitte, Global State of the Consumer Tracker, data as of 26 May 2021.4Source: PwC Global Consumer Insights Pulse Survey, March 2021.

5Source: Adyen, October 2020, “2020 Retail report”.

6See for example: LE Europe, VVA Europe, Ipsos, ConPolicy and Trinomics, October 2018, “Behavioural Study on Consumers’ Engagement in the Circular Economy”, report for the European Commission.

7Source: PwC Global Consumer Insights Pulse Survey, March 2021.

獲取最新市場觀點

訂閱我們的電子報,時刻把握投資資訊和專家分析。

重要資料

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。