獲取最新市場觀點

訂閱我們的電子報,時刻把握投資資訊和專家分析。

Bitcoin is often derided as being highly volatile, but as digital gold it could play a role in a multi-asset portfolio, says investor Jeroen Blokland.

The virtual currency reached a record high of more than USD 60,000 in March – rising from lows of under USD 10,000 one year ago – to achieve a market cap of over USD 1 trillion.

Research by Robeco’s Multi-Asset team suggests that bitcoin could be used with a 1% allocation in a standard, well-diversified multi-asset portfolio, providing that certain risk controls and strict portfolio management rules are applied.

“Bitcoin makes the headlines every day – not only because of its meteoric rise and unrivaled volatility, but also due to the heated debate between its supporters and opponents,” says Blokland, Head of the Multi-Asset team.

“What is more interesting to us, however, is that there’s growing consensus on what bitcoin really is. In recent months, a clear and emphatic narrative that bitcoin is becoming a store of value in the form of digital gold has developed.”

“Recently, US Federal Reserve Chairman Jerome Powell referred to bitcoin as ‘essentially a substitute for gold rather than for the dollar’. Just like gold, bitcoin is scarce and durable. In addition, bitcoin exhibits high portability, is easily transactable and programmable. What it lacks relative to gold, of course, is a long history of being perceived as a store of value.”

“As digital gold, bitcoin has monetary value. In our view, the discussion about bitcoin’s lack of intrinsic value is mostly irrelevant. As with diamonds, art, stamps, gold and the US dollar, bitcoin does not provide cash flows. Yet, all these asset classes have monetary value, and most of them are considered to be a store of value.”

訂閱我們的電子報,時刻把握投資資訊和專家分析。

Gold has traditionally been the ultimate asset used as a backstop for economies and hedge against inflation. “Since the end of the gold standard in 1971, gold has significantly outpaced inflation, rising about 7.7% in value per year,” says Blokland.

“This has been accompanied by a realized volatility of 17. Hence, it is flawed to assume that something considered to be a store of value should have a realized return close to inflation with a relatively low amount of risk.”

“Also, an investment in digital gold does not require extreme views on the economy or fiat currency. If you are looking for a potential hedge against inflation, a collapse in real bond yields and/or a devaluation of the US dollar, allocating to digital gold could be a prudent step towards better portfolio diversification.”

“Given its potential of becoming a store of value as digital gold, we consider bitcoin to be an asset class, albeit an extreme one. Virtually all of its characteristics are very different from traditional asset classes.”

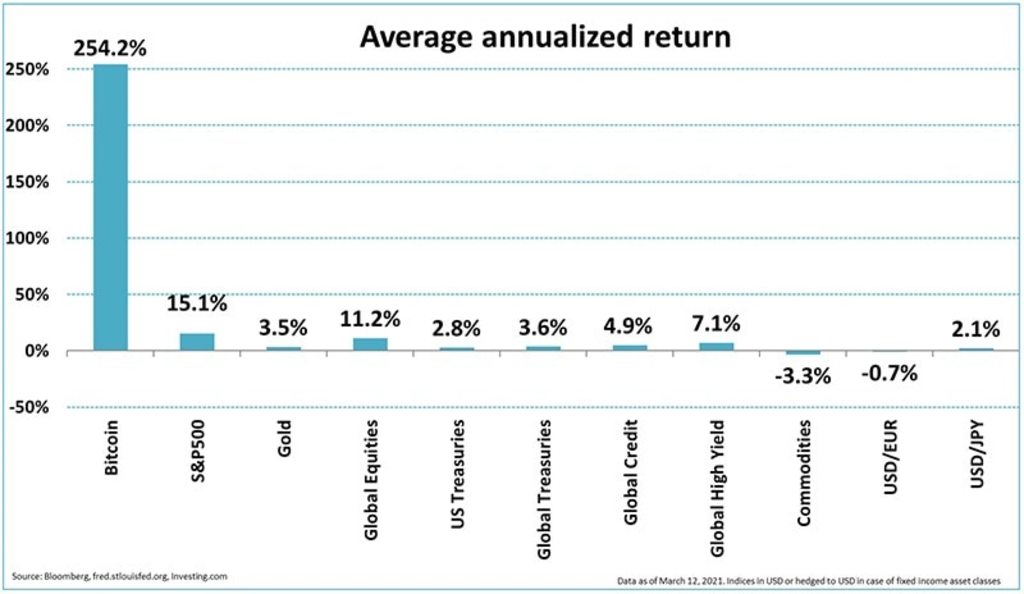

Bitcoin has certainly delivered returns for those brave enough to hold it. Since July 2010, when it first started trading on exchanges, bitcoin’s average return has been an eye-popping 254% per year, compared to 15% for the S&P 500, the next best-performing asset class.

Bitcoin’s return has been far higher than other asset classes. Source: Bloomberg, St. Louis Fed, investing.com.

“Volatility too is extreme – the average realized annualized volatility of bitcoin is a staggering 114%, almost ten times as much as equites and gold,” says Blokland. “Yet, bitcoin’s Sharpe ratio is significantly higher than that of other asset classes. And bitcoin’s correlation with other asset classes has been close to zero, suggesting sizeable diversification benefits.”

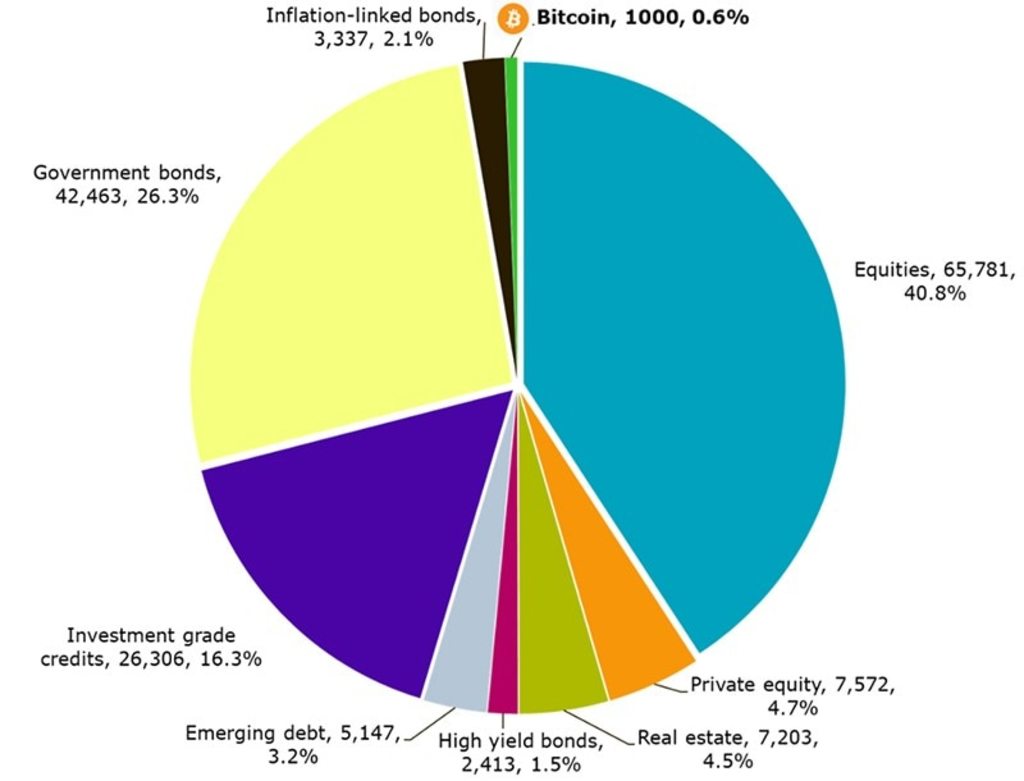

Despite its meteoric rise, bitcoin’s market cap of USD 1 trillion based on the price of USD 55,000 on 29 March translates into a weight of just 0.6% in the Global Multi-Asset Market Portfolio, which consists of the total investable market caps of the major asset classes.

And its recent success is not necessarily sustainable. “Obviously, extrapolating bitcoin’s extraordinary characteristics would lead to some remarkable as well as unrealistic outcomes,” says Blokland. “For example, if we extrapolate bitcoin’s realized return for the next five years, its market cap would rise to over USD 500 trillion.”

“To get to a more realistic estimate of bitcoin’s return going forward, we assume that it reaches the USD 3 trillion market cap of investable gold – gold that is used for investment or is in some way linked to financial markets – somewhere in the next five to ten years. This implies an expected return range of 12%-25% per year.”

So, how much bitcoin could safely be used in a portfolio? The Multi-Asset team uses a complex ‘smart mean variance optimization framework’ to work out how it could fit into a standard and well-diversified multi-asset fund. This looks at 36 different combinations of bitcoin’s risk, return and correlation with other asset classes.

“Our results are unambiguous – for all 36 combinations of risk-return-correlation, our smart optimization allocates the maximum 2.5% towards bitcoin,” says Blokland. “This is better than we anticipated, expecting some drop-off as the combination of characteristics ‘worsens’.”

“However, based on our impact analysis, for example that bitcoin can represent up to 15% of total portfolio volatility, together with the fact that bitcoin’s volatility is currently still well above our highest estimate of 60%, we believe capping the maximum weight of bitcoin to 1% is warranted. A 1% weight also better aligns with overall portfolio management, including rebalancing.”

Some additional considerations should be taken into account, Blokland says. “First, the number of investment alternatives is currently limited, but increasing at the same time. The number of investable exchange-traded funds (ETFs) is growing, as is the futures market.”

“Not all ETFs invest in ‘physical’ bitcoins, however. And cold storage cannot always be insured in full. For bitcoin futures, setting up trading accounts is less straightforward, and margin requirements (up to 33%) are much higher than for bonds and equities.”

“Next to that, regulatory aspects should also be taken into account. In Europe, UCITS regulations limit exposure to single-commodity investments. Still, a bitcoin ‘fund investment’ in Europe is possible as an exchange-traded note (ETN).”

Finally, there is the controversy over the amount of electricity needed to mine digital currencies. “Bitcoin’s assumed energy consumption, as well as its potential use in illicit practices, are further factors of importance,” Blokland says. “They are, however, incredibly complex to judge and value.”

“For example, while bitcoin’s energy use has risen sharply as the processing power (‘hash rate’) to mine bitcoin increases, the impact of this trend depends on the source of the energy. Renewables now represent a significant part of the energy mix, and several studies have emphasized the role of bitcoin mining in reducing the curtailment of renewable energy.”

“But perhaps the most important thing to consider is the fact that bitcoin might not be digital gold, and that there is huge uncertainty surrounding bitcoin’s future compared to asset classes that have a much longer history.”

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。