Portfolio Manager

• 市場觀點

Why do ‘quality compounder’ stocks always look impossibly expensive?

Trends investing focuses on the structural winners of secular growth trends, better known as ‘quality compounders’ – quality growth stocks able to compound shareholder value on a consistent basis. Skeptics of trends investing often dismiss these stocks because they tend to trade at multiples that are – sometimes much – higher than the market’s. But such reasoning is typically shortsighted.

概要

- Focusing solely on valuation multiples misses the full picture

- Steady-state value must be distinguished from future value creation

- Eyepopping multiples can turn out to be very ‘reasonable’

Most investors tend to implicitly assume there is some reasonable range of multiples at which most, or all, companies should trade relative to the market. Usually, this notion of ‘reasonable’ is based on a historical average or a peer group of similar companies. Multiples, however, have become a shorthand for the valuation process.

Importantly, multiples obscure the value drivers that really matter. It is the value drivers that determine the reasonableness of the multiple, not the multiple that determines the reasonableness of the valuation. More specifically, the market value of a company and its associated valuation multiple can be broken down into two main parts:

The steady-state value assumes that the current assets in place, properly maintained, will produce a level of normalized profits indefinitely into the future. This steady stream of future profits can be valued as a perpetuity – in other words, the normalized profit divided by the cost of capital. Therefore, the appropriate multiple to determine what should be paid for the steady-state value of a business is the reciprocal of the cost of capital. So, if the cost of capital is 8%, the steady-state price/earnings (P/E) multiple is 12.5 (1/8%).

Future value creation is driven by three fundamental factors. First, the spread between returns on incremental invested capital and the cost of capital. Second, the relative size of profitable investment opportunities. And third, the duration of competitive advantage.

Differences in multiples across comavpanies are determined by differences in expected future value creation

The steady-state value is the straightforward function of prevailing risk-free capital market rates and the equity risk premium, which itself depends on aggregate investor risk appetite at a given point in time. The steady-state value of a company can vary a lot over time, as both capital market rates and investor risk appetite fluctuate.

However, this does not cause divergence in multiples across companies. Differences in multiples across companies are determined by differences in expected future value creation. Companies that earn high returns on future investments, have sizeable profitable investment opportunities and can be expected to maintain their competitive

There is an obvious link between a company’s life-cycle stage and the multiple it should trade at. Young companies that have a long runway of future value creation ahead of them deserve to trade at much higher multiples than older, larger and more established companies. The latter make up the bulk of the equity market, but have fewer or no growth opportunities relative to their existing assets.

The Big Book of Trends & Thematic Investing

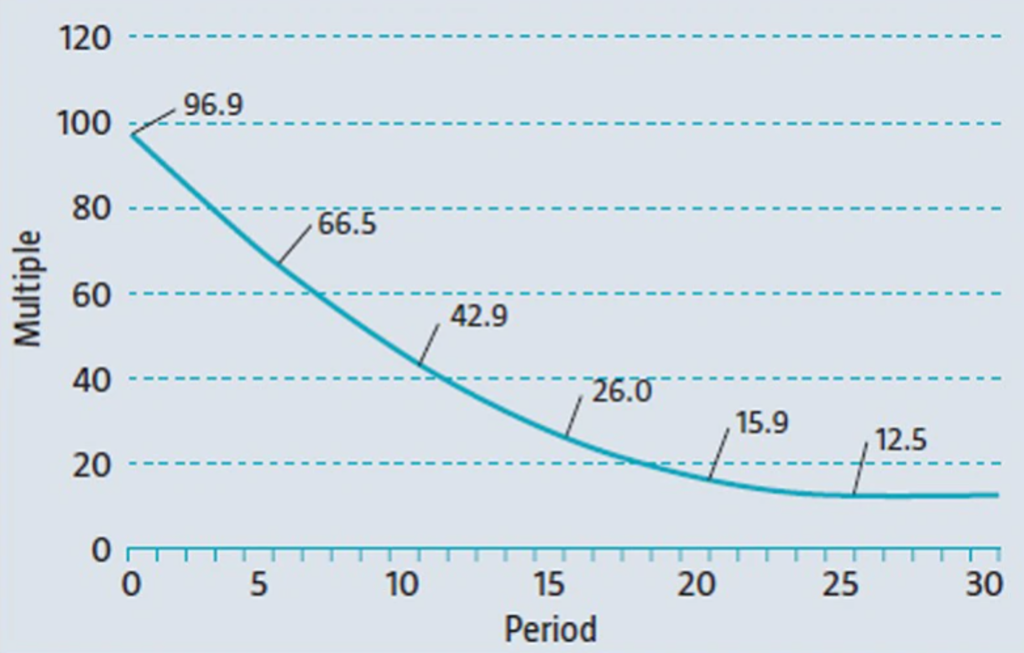

Figure 1: The justified P/E multiple with perfect foresight

Source: Robeco Trends Investing

Figure 1 shows the theoretical multiple trajectory of a fictitious company that starts out with a positive spread of 25% over its 8% cost of capital. The spread is assumed to erode by 1% every year, so that the firm’s competitive advantage will last 25 years. Assuming perfect prescience, investors should be willing to pay a seemingly astronomical P/E multiple of 96.9 at the start of this company’s life.

This high multiple is warranted, however, by the prospect of 25 years of profitable, value-creating growth. As the company matures over time and steadily realizes its growth opportunities, the justifiable valuation multiple will slowly converge towards the steady-state P/E multiple of 12.5 (1/8% after 25 years), reflecting the shrinking prospects for future profitable growth.

Find out more on this topic in our ‘Big Book of Trends and Thematic investing’.

獲取最新市場觀點

訂閱我們的電子報,時刻把握投資資訊和專家分析。

Important information

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.