Impact Specialist

• インサイト

Denmark continues to dominate country ESG rankings

In this update, we learn that emissions, renewables and water management were decisive for both top- and lower-tier performers. In addition, country case studies illustrate that poor ‘G’, amplifies poor ‘S’ and ‘E’. Finally, cyberattacks can cause enduring economic and social damage, posing serious risks to sovereigns.

執筆者

ESG Analyst and Impact Specialist

主なキーワード

まとめ

- Environmental policies weigh on ESG leaders

- Country cases show bad governance is bad news for ESG performance

- There’s now a way to measure a country’s resilience to cyber threats

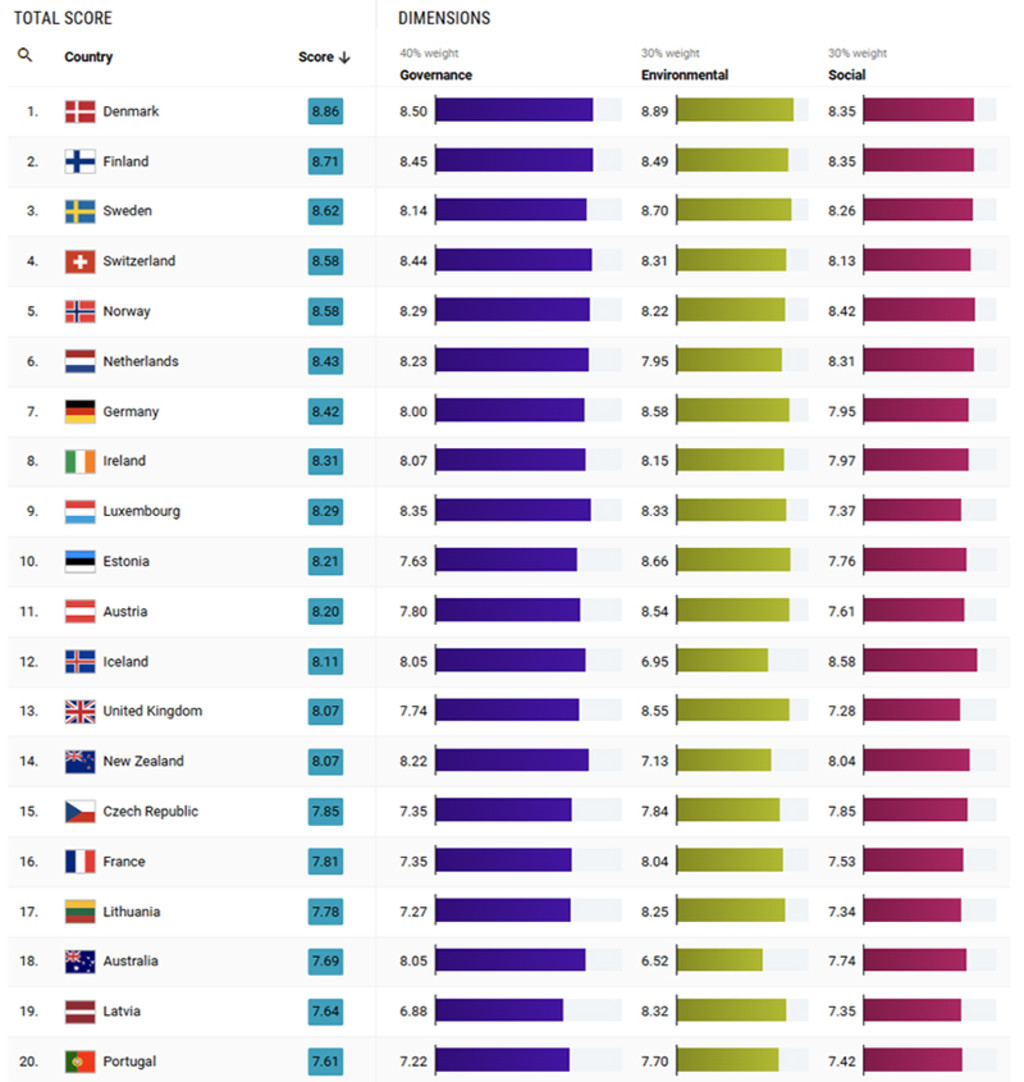

Denmark maintains its ESG leadership, topping Robeco’s Country ESG rankings (click link for complete rankings) for the fourth consecutive time in two years. As in the past, Scandinavian countries had a strong showing which (along with Switzerland) rounded out the top five slots.

ESG performance for those on the leaderboard was not off the charts, however, with most seeing declines in their environmental scores. Denmark and Sweden saw slowdowns in the uptake of renewables as a share of their overall energy mix. Norway lost ground on the management of water stress and climate risks. Runner-up Finland was the only country with a slight increase in environmental scores, due to higher renewable additions and better water use.

Figure 1 - Country ESG score leaders

Source: Robeco, April 2026.

Major govy issuers show mixed (and surprising) results

Scores among the world’s largest sovereign debt issuers continue to diverge. Japan’s ESG score (7.46 of 9.0) slightly declined, while the US score (6.61 of 9.0) remained largely stable. For Japan, reductions in climate and energy criteria were to blame.

Ironically, in the US, lower governance marks (from higher corruption and weaker institutions) were offset by higher environmental scores resulting from Liberation Day tariffs, which reduced CO2 emissions associated with the production of imported goods.

China’s ESG score improved slightly thanks to efforts to improve extinct species, an indicator of biodiversity health.

Scores around the globe

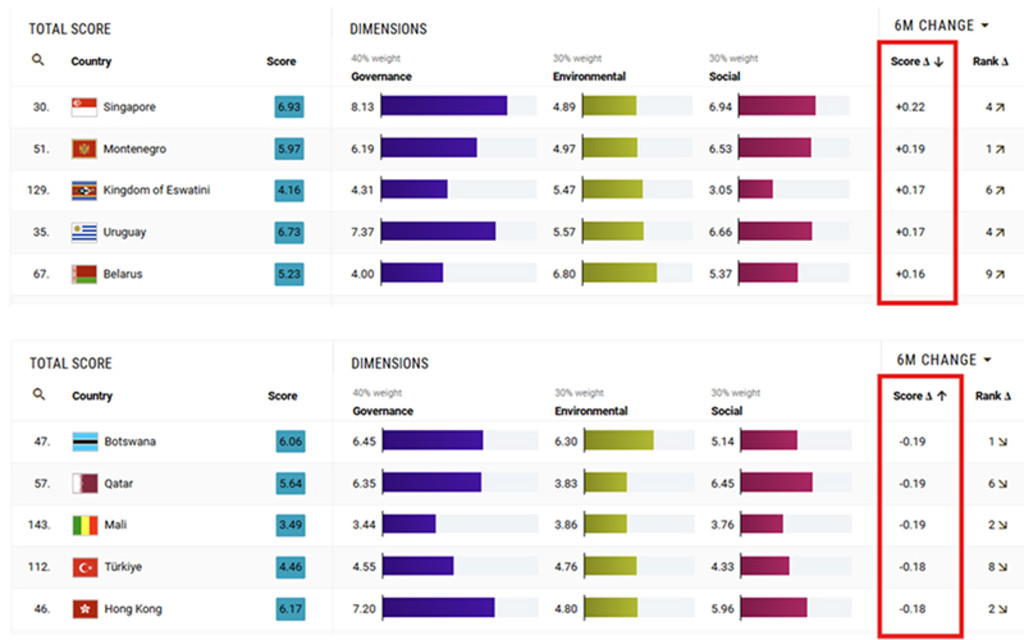

Several emerging markets recorded notable gains in the ranking. Singapore posted the largest absolute score increase due to better water management practices (see Figure 2). Conversely, weaker environmental scores weighed on countries with the largest score decreases including Botswana, Qatar, Mali, Türkiye and Hong Kong.

Figure 2 - Top five countries with the largest gains and losses

Source: Robeco, Country ESG scores, April 2026.

Obstructing Orban’s orbit

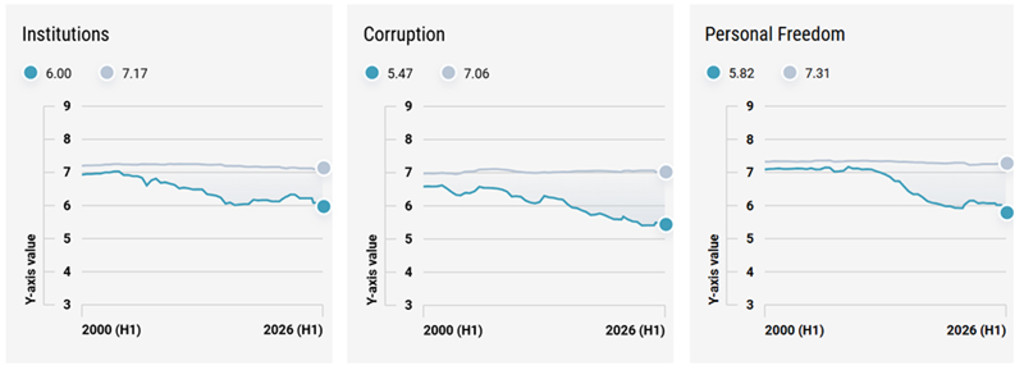

For nearly two decades, Viktor Orban and his Fidesz party dominated Hungary’s political scene. Once seen as a freedom fighter, championing Western ideas, his style became increasingly authoritarian, anti-democratic and corrupt with each passing year. His grip on power ended abruptly in early 2026, when he was voted out of office in spectacular style by Peter Magyar’s Tisza coalition.

However, desired reforms may not come as quickly as his fall, as Orban’s cronies still staff key institutions in the courts, media, and banking often with long-dated appointments. The people have spoken and a clear mandate has been delivered. With Orban out of orbit, progress may be slow, but at least things are now on a positive trajectory.

Figure 3 – Orban’s ESG legacy

Hungary’s Institutional, Corruption, and Personal Freedom scores 2000-2026. Hungary (blue) vs. EU peers (gray)

Source: Robeco, April 2026

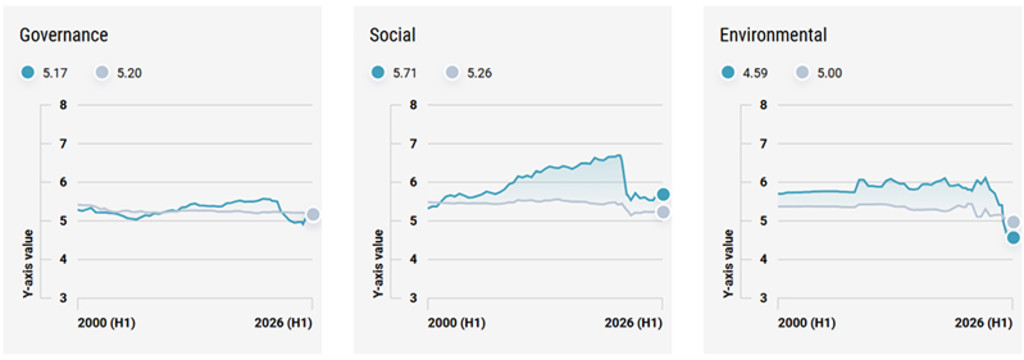

Peru’s perilous plummet

Once a stable ESG performer in the LatAm region, Peru’s standings have slipped of late. The country’s social score has suffered due to widespread protest following chronic crisis of leadership. The country has cycled through several presidents, multiple cabinet reshuffles, and endless friction between branches of government. Corruption scandals of political elites and judges have stoked further distrust.

The chaos highlights deep seated societal tensions related to inequalities, exclusions, and access to basic services. Progress on poverty has stalled, informal work arrangements abound, and weak public services, especially in healthcare and education, are hampering human capital development.

The natural environment is also experiencing troubled waters. Peru is exposed to physical climate risks – including flooding, droughts, and El Niño related shocks – which threaten agricultural production and infrastructure. Weak governance has meant less enforcement of environmental protection, particularly in relation to illegal mining, deforestation, and water pollution. It’s a clear case of how weak governance at the top can intensify social and environmental problems on the ground (see Figure 4). Unfortunately, without some sort of immediate lifeline, Peru’s ESG performance is likely to keep sinking.

Figure 4 – A country in need of more ‘G’- force

Peru’s Governance, Social and Environmental scores, 2000-2026. Peru (blue) vs. Latin American peers (gray).

Source: Robeco, April 2026

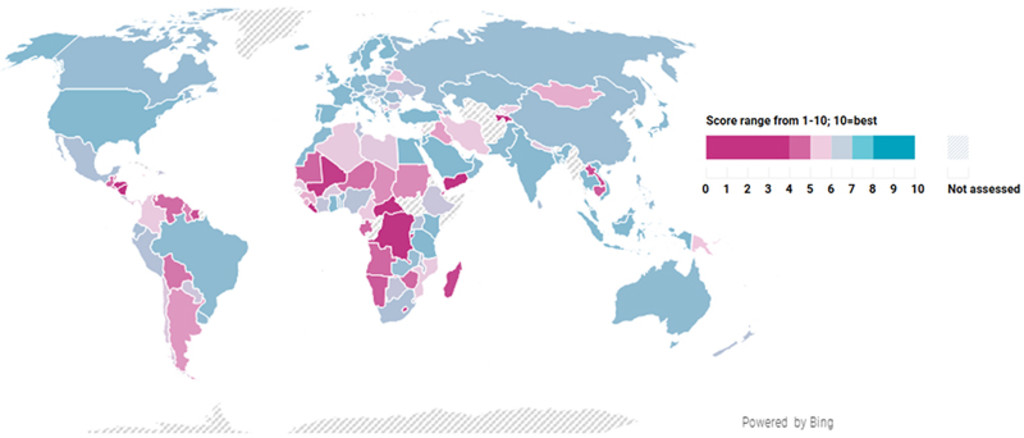

Thematic focus – Cybersecurity

Cybersecurity has become an increasingly material component of sovereign ESG risk, reflecting the growing dependence of governments and economies on digital infrastructure. Large scale cyberattacks have resulted in multi billion dollar losses globally, with governments often bearing indirect fiscal costs through emergency response spending, system reconstruction, litigation, and lost productivity.

The 2017 ‘NotPetya’ cyberattack on Ukraine’s public and private sector systems is widely cited as one of the most destructive, with global damages exceeding USD 10 billion. Moreover, the ‘WannaCry’ ransomware attack in the UK showed attacks were also destructive to public health on a massive scale. It infected National Health Service’s (NHS) computer systems leading to canceled medical procedures and emergency service disruptions.

The Country ESG framework is now integrating cybersecurity as a factor in ESG performance using data from the Global Cybersecurity Index (GCI) developed by the International Telecommunication Union (ITU), a UN agency overseeing global digital networking standards.

Figure 5 – Global Cybersecurity Index world map

Lower scores (pink gradients) indicate that countries are more vulnerable and less prepared for cyber risks.

Source: Global Cybersecurity Index, International Telecommunication Union, April 2026.

Notably, cybersecurity isn’t directly correlated with high GDP. Advanced and emerging countries perform well, from Finland and Italy to Egypt and Indonesia. Though diverse in economy and culture, a characteristic common to them all is that they tend to exercise a whole of government approach, including dedicated cyber agencies, robust legal frameworks, mandatory incident reporting, and strong international cooperation.

Concerningly, many lower-tier performers have rapidly expanded digital services without commensurate investment in cybersecurity governance, leaving them dangerously exposed.

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会