Portfolio Manager

• Visione

La convenienza guida le tendenze nella spesa dei consumatori

L’inflazione sta diminuendo, ma il sentiment dei consumatori e i comportamenti di acquisto suggeriscono che le famiglie rimangono attentamente concentrate sul valore e sull’accessibilità economica. I modelli di spesa stanno divergendo: le famiglie più benestanti guidano la crescita dei consumi, mentre le fasce a reddito più basso riducono le spese. La battaglia per conquistare il cuore (e il portafoglio) dei consumatori si sta intensificando, con i rivenditori che competono non solo sul prezzo più basso, ma anche sulla loro capacità di offrire il massimo valore.

Autoren/Autorinnen

Zusammenfassung

- La convenienza è al centro delle preoccupazioni dei consumatori e delle società che li servono

- I consumatori sono pessimisti, ma la spesa si mantiene stabile

- I discount di grandi dimensioni, i negozi off-price e il second-hand beneficiano delle tendenze attuali

Il linguaggio delle sale riunioni rispecchia ormai le conversazioni a tavola. Le società dei segmenti relativi ai beni di consumo di prima necessità e ai beni di consumo discrezionali parlano di “convenienza” con frequenza sorprendente: le menzioni da parte dei dirigenti sono triplicate negli ultimi cinque anni fino all’1T del 2026 (cfr. Figura 1). Le famiglie controllano ogni dollaro speso e le società se ne sono accorte.

La stretta in cifre

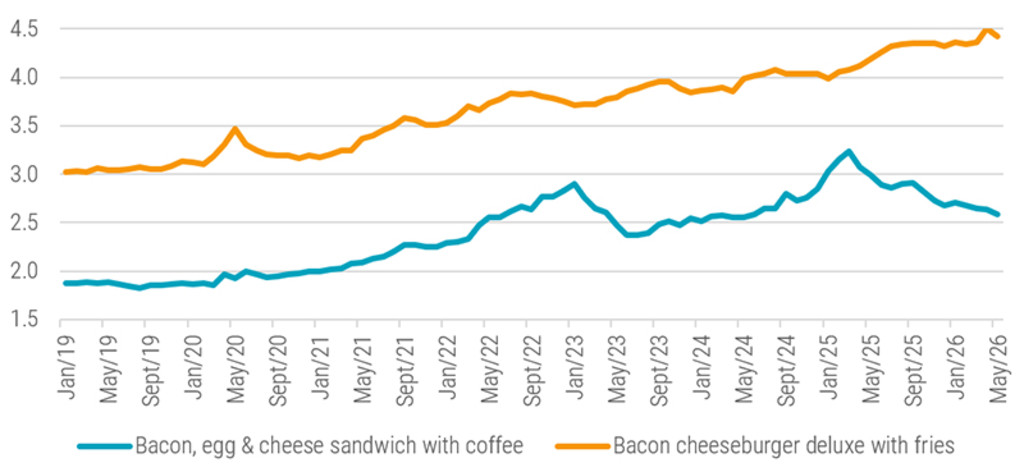

Per molti consumatori, i prodotti di uso quotidiano sono ora causa di uno “shock da prezzo”, ovvero la sgradevole sorpresa di trovare un prezzo insolitamente elevato. L’indice dei prezzi di Bloomberg per un panino americano con pancetta, uova e formaggio accompagnato da caffè è salito del 38% (da 1,87 USD nel 2020 a 2,58 nel 2026), mentre il menu “cheeseburger deluxe con patatine” è aumentato del 42% (da 3,12 dollari a 4,43 dollari, si veda la Figura 1). Questi esempi concreti spiegano perché così tanti consumatori si sentano ancora più poveri, anche se l’inflazione negli Stati Uniti è scesa dal picco del 9,1% del 2022 al 4,2% di maggio.

Figura 1 – Indice dei prezzi per i pasti più consumati negli Stati Uniti

Fonte: Bloomberg, 2026.

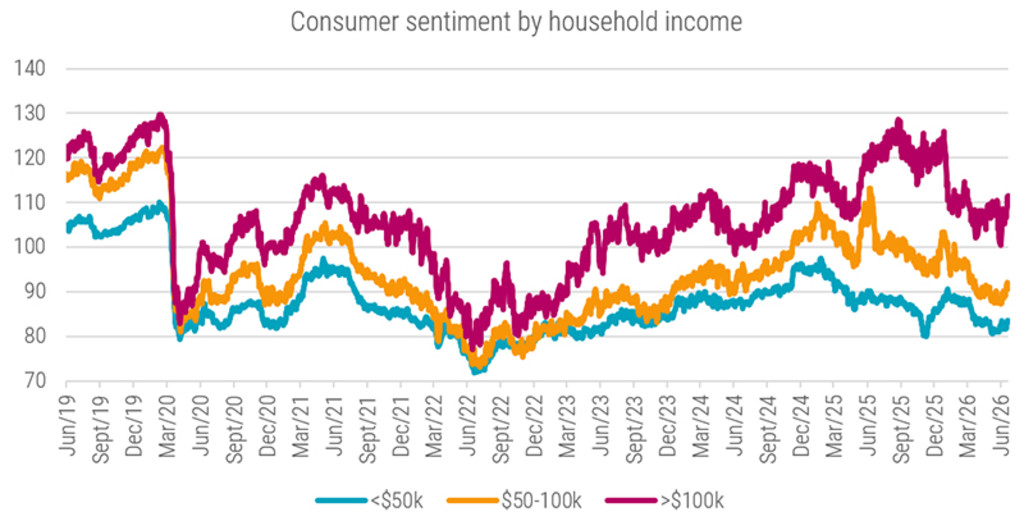

Inoltre, le famiglie su entrambe le sponde dell’Atlantico hanno la sensazione di perdere terreno: l’indice del sentiment dei consumatori dell’Università del Michigan (Stati Uniti) è sceso da circa 100 nel 2020 a un nuovo minimo storico di 45 a maggio, raggiungendo livelli in genere associati alle recessioni. In Europa il sentiment è sceso da -12 a febbraio a -18 a giugno, segnando il peggior deterioramento su due mesi degli ultimi anni (si veda la Figura 2).

Figura 2 – Indice di fiducia dei consumatori

Fonte: Università del Michigan, Eurostat, 2026.

Conta ciò che fanno, non ciò che dicono

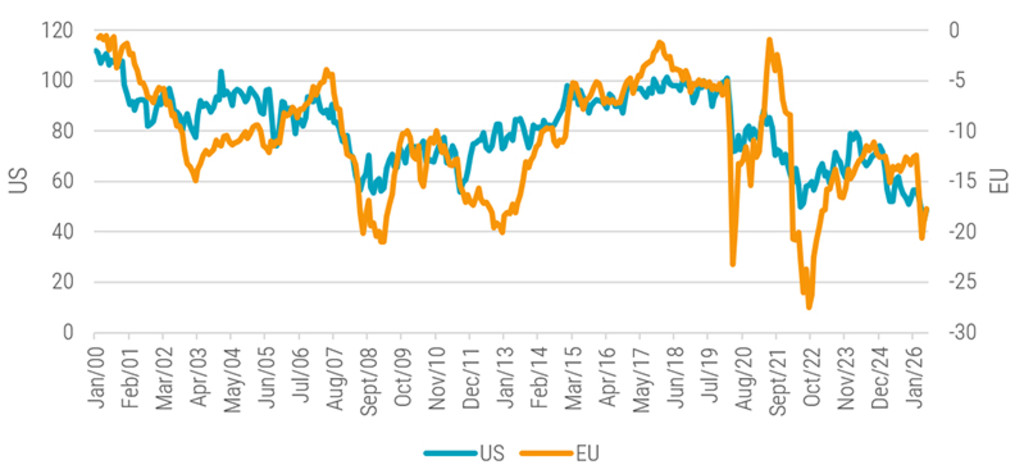

Fortunatamente per i rivenditori, il clima di pessimismo e di catastrofismo percepito dai consumatori è stato compensato dalla resilienza dell’occupazione e dei redditi. Il tasso di disoccupazione negli Stati Uniti resta basso, al 4,3% (a maggio 2026), mentre anche i tassi di disoccupazione nelle altre principali economie si collocano in una fascia sana, tra il 2,5% e il 6%. Al tempo stesso, le vendite al dettaglio continuano a crescere, suggerendo un legame solo debole tra sentiment e spesa effettiva. La crescita dei volumi di pagamento negli USA conferma questo quadro, registrando un aumento di circa il 9,0% ad aprile rispetto al 7,5% dell’1T. A livello globale, i volumi sono cresciuti del 9,0% nell’1T rispetto all’8,0% del 4T, confermando il motto: “conta ciò che i consumatori fanno, non ciò che dicono” (si veda la Figura 3).

Figura 3 – La spesa al dettaglio è in aumento nella maggior parte delle principali economie

Fonte: US Bureau of Labor Statistics, Eurostat, Ministero giapponese degli Affari interni, Istituto nazionale di statistica della Cina, Central Statistics Office India, 2026.

Un paradosso a forma di K

Sebbene gli utili crescano più rapidamente per i percettori di redditi più bassi rispetto ai gruppi a reddito più elevato, i primi consumano comunque meno, dando luogo a un’economia “a forma di K”. Di conseguenza, le società devono rivolgersi a due tipologie di pubblico: i consumatori più abbienti, ancora disposti a pagare per una qualità più elevata, e quelli schiacciati dal carovita, che hanno bisogno che i prezzi dei beni di uso quotidiano diminuiscano. I dati sul mercato del lavoro statunitense mostrano che, dall’inizio del 2019 ad oggi, i salari reali (al netto dell’inflazione) sono cresciuti di più per i redditi bassi che per quelli alti, oltre al fatto che tutti i gruppi di reddito hanno superato l’inflazione. Al tempo stesso, i dati sulla spesa rivelano un’economia chiaramente a due velocità negli USA: le famiglie ad alto reddito hanno aumentato i consumi (crescita compresa tra il 5% e il 10%) dall’inizio del 2025, mentre la spesa di quelle a reddito più basso ha subito un rallentamento e, in alcuni casi, ha registrato un’inversione di tendenza.

Figura 4 – Il sentiment dei consumatori è divergente tra le famiglie a basso e ad alto reddito

Fonte: Morning Consult, Bloomberg, maggio 2026.

Tendenze simili sono osservate dalle agenzie di viaggio, che segnalano il modo in cui i consumatori più facoltosi stiano spendendo generosamente in viaggi, ristorazione ed esperienze premium. La catena alberghiera di lusso Hyatt* ha dichiarato che la domanda da parte dei clienti premium è stata eccezionalmente forte nell’ultimo trimestre, segnando un aumento di circa il 7% rispetto al 2025. Anche le crociere, considerate un bene di lusso, stanno vivendo un momento di grande slancio: le due maggiori compagnie al mondo in tale settore, Royal Caribbean e Carnival, hanno raggiunto livelli record di prenotazioni e prezzi in quanto l’inclusione in un’unica tariffa di alloggio, pasti e intrattenimento è percepita come un buon rapporto qualità/prezzo rispetto alle vacanze sulla terraferma.*

Global Consumer Trends D EUR

- performance ytd (30-6)

- 5,45%

- Performance 3y (30-6)

- 9,04%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Ertragsverwendung (30-6)

- No

Frühere Wertentwicklungen, Simulationen oder Prognosen sind kein verlässlicher Indikator für die zukünftige Wertentwicklung.Annualisiert (für Zeiträume, die länger als ein Jahr sind). Die Performance-Zahlen sind abzüglich Gebühren und basieren auf den Transaktionspreisen.

Il comportamento dei consumatori si sposta verso il valore

Il comportamento dei consumatori si sta orientando in modo deciso verso il valore e una maggiore attenzione ai costi: circa il 75% delle famiglie statunitensi sta passando a marchi e retailer più economici, mentre la metà sta rinviando gli acquisti discrezionali. I consumatori stanno inoltre riducendo le spese per mangiare e bere fuori casa. Il prezzo, tuttavia, non è l’unica variabile decisionale: oltre a cercare occasioni, i consumatori accumulano punti fedeltà dai loro marchi preferiti e vanno verso ciò che ritengono essere di maggior valore.

I retailer si stanno adattando rapidamente e i discount di grandi dimensioni sono i principali beneficiari. Walmart* sta puntando sul valore, quindi, oltre a prezzi più bassi, sta ampliando la gamma “private label” e sta offrendo spedizioni in giornata. Anche le categorie di beni essenziali di uso quotidiano e di generi alimentari di Amazon stanno crescendo rapidamente, tanto che rappresentano ormai un’unità venduta su tre. Come Walmart, Amazon* sta aumentando il valore tramite la comodità, offrendo consegne in giornata anche su articoli a basso prezzo.

Il comportamento dei consumatori si sta orientando in modo deciso verso il valore e una maggiore attenzione ai costi. Circa il 75% delle famiglie statunitensi sta passando a marchi e retailer più economici

Anche la popolarità dei “private label” è in aumento: le vendite negli Stati Uniti hanno raggiunto il record di 283 miliardi di dollari nel 2025, totalizzando quasi un quarto dei volumi in unità. Kirkland Signature di Costco* ha generato l’anno scorso vendite annue stimate in 80 miliardi di dollari (più della maggior parte dei retailer globali). Entro la metà del 2026 ci si attende che la generazione Z destini ai marchi di insegna una quota del budget superiore a quella di qualsiasi altra generazione, il che suggerisce che questo cambiamento sia strutturale e non ciclico. I consumatori cercano inoltre sconti più elevati e affollano di negozi a prezzi scontati come TJ Maxx, Marshalls, HomeGoods, Ross Stores e Burlington*, tutte caratterizzate da una solida crescita.

Anche il mercato dell’usato è diventato mainstream, poiché una quota crescente di consumatori attenti al valore non associa più il “grande affare” esclusivamente a beni di nuova produzione. Il marketplace online eBay* ha registrato una crescita a due cifre, attirando consumatori a reddito più elevato attenti tanto al portafoglio quanto alla sostenibilità. Le piattaforme di rivendita come Vinted, Depop e Poshmark* hanno continuato a crescere, intercettando un mercato dell’abbigliamento di seconda mano che potrebbe valere 350 miliardi di dollari entro il 2028.

Il mercato dell’usato è diventato mainstream, poiché una quota crescente di consumatori attenti al valore non associa più il “grande affare” esclusivamente a beni di nuova produzione

Prezzi e promozioni sono protagonisti anche nel settore della ristorazione veloce: McDonald’s* ha riconquistato con successo i clienti a basso reddito con il lancio dei suoi menu McValue, che hanno contribuito a ridare slancio all’attività nella maggior parte dei suoi mercati. Taco Bell, Wendy’s, Chipotle e persino la catena fast casual Panera hanno seguito l’esempio con i propri menu convenienti. Anche se molte catene di fast food hanno migliorato la propria offerta in termini di valore, continuano ad affrontare venti contrari, tra cui l’aumento delle persone che mangiano a casa e l’adozione di farmaci dimagranti che riducono l’apporto calorico.

È evidente che le società meglio posizionate per intercettare i consumatori di oggi e di domani si concentrano su: 1) costruire fiducia offrendo un valore costante, anziché promozioni a breve termine; 2) investire in funzionalità aggiuntive di prodotti o servizi, affinché “prezzi bassi” non equivalgano a “bassa qualità”; e 3) comunicare la propria proposta di valore in modo tempestivo e frequente.

* Tali società sono riportate a scopo puramente illustrativo per dimostrare la strategia d’investimento alla data indicata. Esse non sono necessariamente detenute dalla strategia, né è garantita la loro inclusione in futuro. Non si tratta di una raccomandazione di acquisto, vendita o detenzione, né si deve fare alcuna deduzione sul futuro sviluppo di tali società.

Leggi gli ultimi approfondimenti

Iscriviti alla nostra newsletter per ricevere aggiornamenti sugli investimenti e le analisi dei nostri esperti.