Co-Portfolio Manager

• Visione

L’IA fisica e il nuovo calcolo energetico nella produzione manifatturiera

La produzione manifatturiera è ancora dominata dai combustibili fossili, il che la rende altamente inquinante ma anche esposta a shock energetici costosi e imprevedibili. Parallelamente, l’IA fisica promette non solo di migliorare la produttività, ma anche di promuovere l’elettrificazione, l'efficienza energetica e, più in generale, la transizione energetica.

Relatori

Equity Analyst

Top keywords

Sommario

- Le fabbriche rappresentano il singolo maggior potenziale inesplorato per la decarbonizzazione

- L’IA fisica può generare risparmi energetici compresi tra il 15% e il 75% in ambito industriale

- L'IA contribuirà a gestire la sfida energetica della robotica e dell'automazione nelle fabbriche

Per la maggior parte delle persone, la transizione energetica richiama alla mente pannelli solari, turbine eoliche e veicoli elettrici. Sebbene efficaci, questi strumenti trascurano il singolo settore che consuma più energia al mondo: l'industria. Il settore industriale ha rappresentato quasi il 40% della domanda finale globale di energia, la quota più elevata tra tutti i settori di utilizzo finale.1 E sebbene l'industria si stia elettrificando, non lo sta facendo abbastanza velocemente, poiché i tassi di elettrificazione globali si sono stabilizzati intorno al 20% (il che significa che circa l’80% della domanda dipende ancora dai combustibili fossili).2

Inoltre, l'industria è responsabile anche della quota prevalente di tutta la crescita della domanda di energia (circa due terzi), il che la rende un obiettivo primario per gli sforzi volti a migliorare l'efficienza energetica.3 In questo contesto, una nuova generazione di tecnologie, in particolare l'IA fisica, si sta affermando come un fattore chiave che dovrebbe favorire un'ulteriore elettrificazione, l'efficienza energetica e la sicurezza energetica (grazie a una ridotta dipendenza dai combustibili fossili) in tutti i settori, in particolare in quello produttivo.

L’IA fisica rappresenta una svolta per la tecnologia industriale, spostando l'IA dagli ambienti digitali alle fabbriche, agli edifici e alle reti elettriche. Combinando rilevamento, connettività e inferenza in tempo reale, le macchine ora percepiscono, decidono e agiscono in modo autonomo nel mondo fisico.

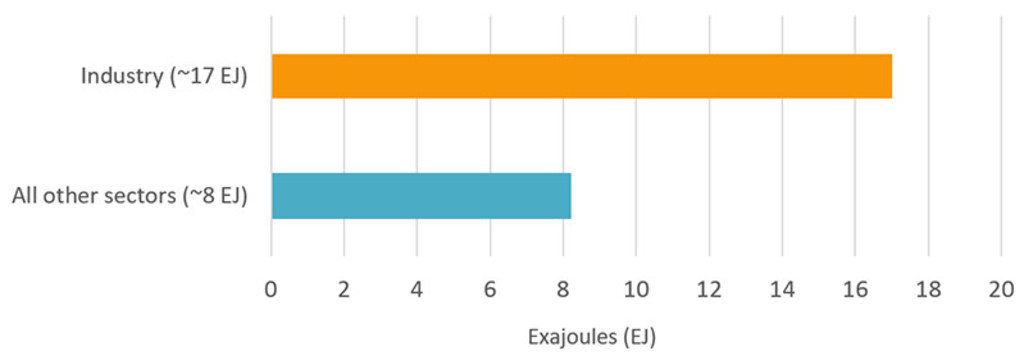

Figura 1 – La quota dell'industria nella crescita della domanda di nuova energia

Fonte: IEA Energy Efficiency, 2025. Crescita del consumo totale di energia finale a livello globale, 2019-2024 (~25 EJ).

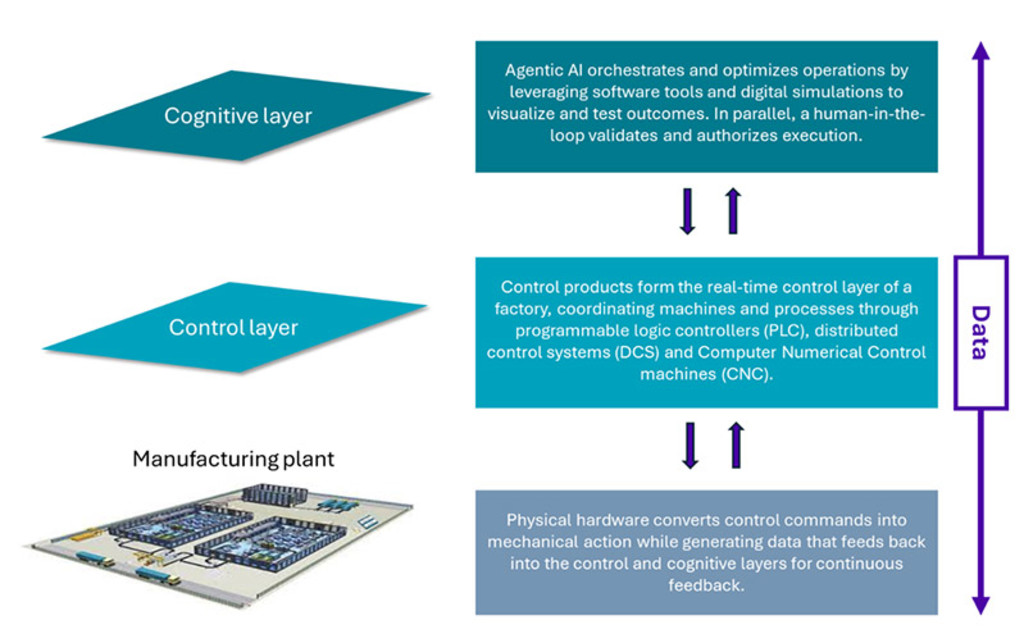

L'adozione dell’IA fisica sta procedendo in tre fasi. La prima, che comprende l’automazione “pick-up-and-place”, la manutenzione predittiva e il rilevamento industriale, è già ampiamente diffusa. La seconda, attualmente in fase di sperimentazione, si concentra su progettazione assistita dall’IA, monitoraggio avanzato dei processi e digital twin. La terza, più avanzata, prevede la collaborazione tra più robot e esseri umani e simulazioni tramite “world model”, in cui l’IA comprende i vincoli fisici in modo sufficientemente approfondito da gestire autonomamente interi ambienti di stabilimento (si veda la Figura 2). Una quota compresa tra il 5% e il 10% dei principali ricavi derivanti dall'automazione industriale include già funzionalità di intelligenza artificiale, e l'IA è integrata in una quota significativa dei nuovi prodotti lanciati sul mercato.4

Figura 2 – L’IA è già integrata nella produzione industriale

Fonte: Siemens, Robeco, 2026. 5

Smart Energy D EUR

- performance ytd (30-6)

- 54,65%

- Performance 3y (30-6)

- 25,47%

- morningstar (30-6)

- SFDR (30-6)

- Article 9

- Pagamento del dividendo (30-6)

- No

I rendimenti passati non sono indicativi dei possibili risultati futuri. Il valore degli investimenti può subire oscillazioni.Annualizzati (per periodi superiori ad un anno). Le performance si intendono al netto delle commissioni e sulla base dei prezzi delle operazioni.

Casi d'uso dell’IA – cosa stanno realizzando i leader del settore industriale

Le conversazioni con le principali aziende del settore delle tecnologie industriali rivelano una corsa per il controllo dello stack fisico dell’IA, con la gestione dell'energia come priorità fondamentale. Per esempio, Siemens* si sta posizionando come spina dorsale dell’“IA per il mondo reale”. Il suo robot umanoide su ruote, impiegato nell'ambiente reale di una fabbrica di elettronica, ha registrato tassi di successo elevati nello svolgimento autonomo di attività logistiche come la selezione, il trasporto e la movimentazione dei container.5

Il prossimo prodotto dell'azienda, "Digital Twin Composer", combina la simulazione Omniverse di Nvidia* con dati ingegneristici in tempo reale, consentendo la creazione di ambienti metaverso industriali su larga scala in cui agenti di intelligenza artificiale simulano le modifiche di processo con una precisione pari a quella della fisica prima che venga apportata qualsiasi modifica fisica.6 I primi progetti pilota hanno già consentito di ottenere una convalida quasi completa della progettazione e una riduzione significativa delle spese in conto capitale.

Il colosso industriale francese Schneider Electric* utilizza inoltre le GPU e Omniverse di Nvidia per creare digital twin di sistemi energetici avanzati. Questi modelli simulati mostrano i requisiti di potenza dalla rete elettrica fino ai singoli chip, consentendo una pianificazione precisa della distribuzione dell'energia e della resilienza a livello di impianto.7 Il conglomerato industriale giapponese Hitachi* impiega già agenti di IA per diagnosticare con elevata precisione i problemi delle apparecchiature industriali, con tempi di risposta molto brevi. Nelle reti elettriche, le ispezioni abilitate dall’IA hanno migliorato sensibilmente l'efficienza operativa.8 Nexans*, società francese specializzata in cavi e trasmissione di energia, utilizza l’IA in modo analogo, integrando IA e sensori lungo l'infrastruttura di rete per migliorare la previsione dei guasti e l’ottimizzazione in tempo reale dei flussi di energia.9

Sebbene si tratti di casi d'uso differenti, tutti si avvalgono di piattaforme di "digital twin" per generare simulazioni utilizzando dati reali di fabbrica, sistemi di IA perimetrale integrati in macchinari e apparecchiature per un adattamento in tempo reale sul campo e, infine, agenti di IA autonomi in grado di sintetizzare rapidamente produzione e processi a partire da dati aziendali su scala globale. Ogni livello dell’IA riduce il consumo energetico e gli sprechi, avvicinando la produzione a un futuro a zero emissioni nette (vedere Figura 3).

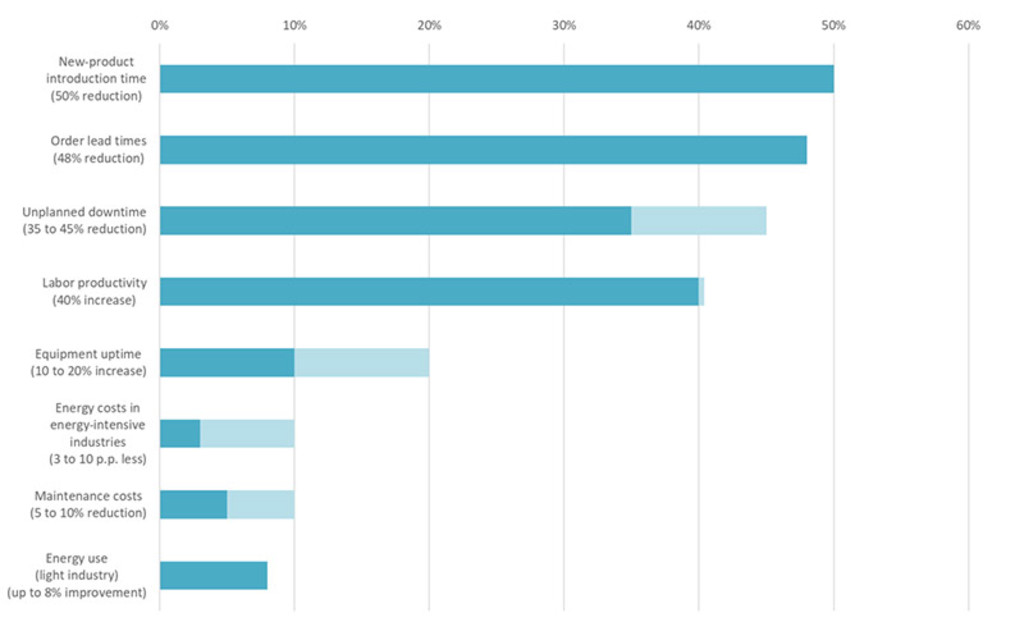

Figura 3 – I benefici quantificati di IA e machine learning nella produzione

Fonte: IEA (Energy & AI, 2025), IEA Key Questions on Energy & AI (2026), WEF & McKinsey Global Lighthouse Network (2025-26), US Dept of Energy FEMP, Operational Best Practices, Deloitte Analytics Institute, dati sulla manutenzione predittiva (2017).

Efficienza energetica tra cervello e muscoli

Se l’IA consente un’elaborazione e un'inferenza rapida dei dati, e rappresenta il cervello, gli attuatori all'interno dei robot possono essere considerati i muscoli. Gli attuatori, che trasformano l'energia in movimento, rappresentano una dimensione meno discussa ma in rapida evoluzione dell'efficienza energetica delle fabbriche. Ogni robot industriale, ogni braccio robotico collaborativo, ogni umanoide è in definitiva un insieme di sistemi di controllo del movimento (ad esempio attuatori, motori, riduttori e azionamenti). Le prestazioni energetiche di questi componenti stanno rapidamente diventando un tema di interesse per gli investimenti.

I motori elettrici nelle articolazioni robotiche raggiungono un'efficienza di circa l’80% se considerati singolarmente, ma questa percentuale scende a circa il 40% una volta inclusi riduttori e sistemi di trasmissione.10 Su una base installata globale di circa 4,3 milioni di robot industriali,11 le perdite energetiche complessive saranno considerevoli. La pianificazione dei movimenti ottimizzata dall’IA è una potente leva di efficienza, al pari degli aggiornamenti hardware. Per esempio, grazie ai digital twin collegati ai robot industriali Fanuc*, gli ingegneri hanno ridotto del 74,8% il consumo di energia nelle operazioni pick-and-place.12

Gli umanoidi, che possono contenere decine di attuatori oltre ad altri componenti ad alto consumo energetico, rappresentano una sfida energetica ad ampio spettro. Per esempio, Optimus di Tesla, Digit di Agility Robotics e Apollo di Apptronik presso Mercedes-Benz* hanno un’autonomia di sole due-quattro ore per ricarica, limitata dall’inefficienza degli attuatori, dalla dispersione di calore e dalle batterie a bassa densità energetica.13

Tutto ciò riduce la produttività, l'efficienza e, in ultima analisi, la sostenibilità economica degli umanoidi in ambienti produttivi reali. Tuttavia, la risposta ingegneristica sta accelerando. Gli attuatori ad azionamento quasi diretto (QDD) di nuova generazione offrono rapporti coppia-peso da tre a cinque volte superiori rispetto ai riduttori armonici convenzionali,14 mentre le nuove tecnologie di ingranaggi magnetici e i motori brushless ad alta efficienza stanno portando l'efficienza degli attuatori oltre il 90%.15

Le società che risolvono il problema energetico degli attuatori, attraverso progettazione avanzata dei motori, elettronica di potenza e ottimizzazione del movimento basata sull’IA, stanno creando un vantaggio tecnologico che sarà al centro della prossima era industriale.

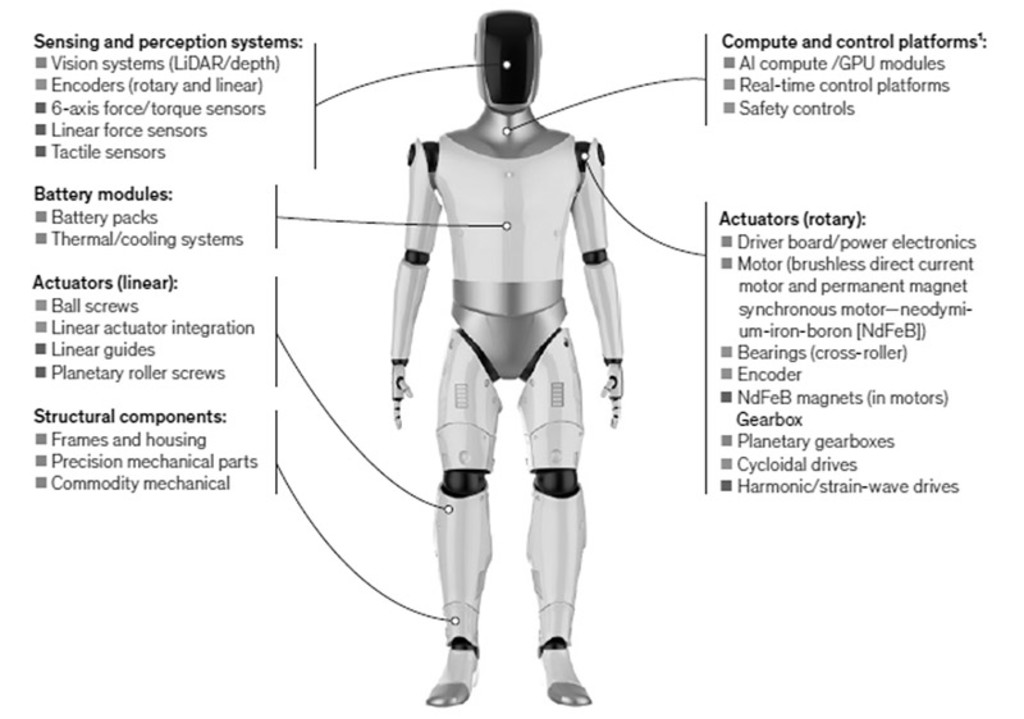

Figura 4 – Gli attuatori rappresentano fino al 60% dei componenti a maggior impatto di un umanoide

Fonte: McKinsey, 2026. I principali componenti hardware dei robot umanoidi includono attuatori (40-60%), sistemi di rilevamento e percezione (10-15%), componenti strutturali (5-10%) e moduli batteria (5-10%).16

Investire è imperativo

L'industria consuma il 40% della domanda finale di energia, il che la rende un obiettivo ideale per tecnologie come l’IA fisica, che promettono di aumentare l'efficienza energetica e ridurre gli sprechi. Ma non si tratta solo di adottare l'IA: la prossima generazione di leader industriali sarà definita dall'efficienza con cui implementerà l'IA fisica, combinando il “cervello” intelligente con i “muscoli” ad alta intensità energetica.

A livello di stabilimento, i “muscoli” dell’IA fisica - attuatori, motori e sistemi robotici - sono fattori fondamentali della domanda di energia, e ciò rafforza la necessità di processi industriali e tecnologie di movimento più efficienti. Con l'elettrificazione della produzione e la crescente automazione basata sull'IA, il consumo di energia elettrica sta emergendo come un fattore chiave di competitività.

Al contempo, il “cervello”- semiconduttori, modelli di IA e software di controllo - determina l'efficacia con cui viene utilizzata tale energia, alimentando la domanda di chip ad alta efficienza energetica, sistemi di controllo avanzati e software di ottimizzazione. I sistemi di IA fisica richiedono dati operativi reali e di alta qualità per ottimizzare le prestazioni in presenza di vincoli concreti, e molte aziende consolidate con basi dati e piattaforme di produzione stanno cogliendo l'opportunità, collaborando con leader tecnologici dell’IA per ottenere un vantaggio competitivo.

Tuttavia, la produttività guidata dall’IA può essere applicata anche anche ad altre aree a supporto delle operazioni di fabbrica. Tra queste rientrano la distribuzione e la gestione dell'energia tramite reti intelligenti, i sistemi di stoccaggio e l'elettronica di potenza, che consentono un approvvigionamento elettrico affidabile e flessibile. Con l'espansione dell'integrazione dell'IA, la consolidata presenza della strategia Smart Energy lungo l'intera catena del valore energetico aiuterà il team a individuare le aziende meglio posizionate per integrare e implementare tecnologie di IA al fine di ottimizzare i flussi energetici e la crescita futura.

*Tutte le società citate in questo articolo sono riportate a scopo puramente illustrativo per dimostrare la strategia d'investimento alla data indicata. Tali società non sono necessariamente detenute dalla strategia né è garantita la loro inclusione in futuro. Non si tratta di una raccomandazione di acquisto, vendita o detenzione, né si deve fare alcuna deduzione sul futuro sviluppo di tali società.

Nota in calce

1 Sito web IEA, “Industry — Energy Efficiency 2025.

2 IEA, World Energy Outlook 2025

3 IEA, Energy Efficiency Market Report, novembre 2025. Il consumo finale totale nel 2024 ha superato i 450 EJ ed è aumentato di circa 25 EJ dal 2019. L'industria rappresenta la quota maggiore di questa domanda, con quasi il 40%. Dal 2019 l'industria ha registrato la crescita più forte, contribuendo per due terzi all'aumento complessivo della domanda globale di energia.

4 Ricerca proprietaria Robeco; informazioni presentate alla Fiera di Hannover 2025. Prodotti con IA integrata: quota di mercato compresa tra il 5% e il 10% nei principali settori dell'automazione industriale.

5 Ricerca proprietaria Robeco; dichiarazioni del management Siemens alla Fiera di Hannover 2025. L'umanoide su ruote ha eseguito in autonomia operazioni di prelievo, trasporto e movimentazione in una fabbrica operativa.

6 Ricerca proprietaria Robeco; annuncio di Siemens su Digital Twin Composer, 2025. Lancio previsto per metà 2026 tramite Siemens Marketplace; basato su NVIDIA Omniverse.

7 Ricerca proprietaria Robeco; comunicazioni Schneider Electric / AVEVA / NVIDIA. Modello di digital twin dalla rete al chip sviluppato con software ETAP.

8 Ricerca proprietaria Robeco; dichiarazioni del management Htachi. Diagnostica basata su agenti di IA implementata su apparecchiature industriali e reti elettriche.

9 Ricerca proprietaria Robeco; dichiarazioni del management Nexans. Analisi basate sull’IA per la previsione dei guasti e l’ottimizzazione in tempo reale della rete.

10 Qviro, analisi tecnica citata in Articsledge, “AI Humanoid Robots 2026”, 2026.

11 International Federation of Robotics, World Robotics 2024.

12 Springer Nature, “Digital Twin-Based Self-Learning Decision-Making Framework for Industrial Robots”, IJAMT, giugno 2025. FANUC ER-4iA pick-and-place: riduzione del consumo energetico del 74,79% tramite ottimizzazione bayesiana.

13 GlobalSpec, “Humanoid Robots Are Tripping Over Their High Energy Demands”, settembre 2025. Autonomia attuale: 2–4 ore per carica.

14 Intel Market Research, “Humanoid Robot Rotary Actuator Market Outlook 2025–2032”, 2025. Attuatori QDD: rapporto coppia/peso superiore da 3 a 5 volte rispetto ai riduttori armonici.

15 Intel Market Research, 2025. I motori brushless e la tecnologia degli ingranaggi magnetici spingono l'efficienza degli attuatori oltre il 90%.

16 McKinsey & Company, Turning humanoid supply chain constraints into billion-dollar wins, aprile 2026.

Quali sono i temi caldi del momento?

Iscriviti per ricevere in un’unica newsletter tutte le ultime tendenze dell’investimento tematico.