Head of Investments China

• Insight

China needs fiscal firepower to spark equity revival

More aggressive fiscal expansion to offset continued property market weakness is needed after CEWC signals a pro-growth bias for 2024

Authors

Client Portfolio Manager

Top keywords

Summary

- China’s Central Economic Work Conference (CEWC) foreshadows ambitious 2024 growth target

- Fiscal boost is the key to offset negative wealth effect from property market

- Policy announcements will provide a catalyst for beaten-down equities

We are constructive on Chinese equities in the coming year. Some investors might think that going long China equities now feels like a brave move given the deeply negative investor sentiment in 2023 but this is where we need to be clear-sighted. Earnings revisions are still being subdued by the weak and bumpy macroeconomic recovery, but this is likely to change when the explicitly pro-growth fiscal policy starts taking effect in 2024.

Growth focus at the CEWC

The 2023 CEWC which took place on 11 and 12 December has set the scene for policy focused on supporting growth in 2024. The adoption of the mantra ‘pursuing stability through growth’ was new and represents a firm indication that China’s 2024 growth target to be set at an ambitious 5%, matching the 2023 target despite the less favorable base effects. The detail will have to wait until the new year but the acknowledgement of “a lack of effective demand” in state media1 was a clear sign that there is a need for action to offset the drag from the property sector.

So far, a piecemeal easing of monetary policy, relaxation to regulation and quiet words with bankers have not been able to revive the property market with house and apartment prices still falling during Q4 2023. This in turn is having a negative wealth effect and undermining consumer confidence, leaving the economy struggling for momentum. Against this backdrop, and despite global equities rallying through November, China equities slid to their lowest levels since November 2022, completely wiping out the post-pandemic recovery trade. Valuations are now at a deep discount to other emerging markets, never mind the US. Given the high quality and long term growth prospects of many companies in the China universe, especially in technology self-sufficiency, industrial upgrade, energy transition and healthcare, this discount won’t persist for long in our view.

Fiscal policy still to be unleashed

With monetary policy already accommodative, it’s logical to anticipate a more expansive fiscal policy to support growth and enable the GDP target to be achieved. This will include renewed public spending on social housing and infrastructure. The China bond market’s sanguine response to the Moody’s downgrade of its outlook for Chinese sovereign bonds shows it’s ready to absorb an expected rise in bond issuance. Consequently, a significant expansion of central government spending, channelled via local government, is very likely and will be positive for China equities.

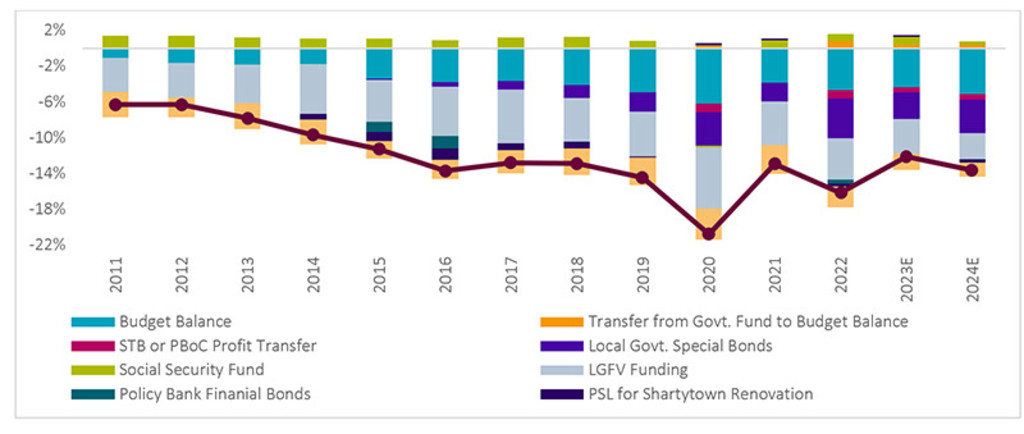

Figure 1: Fiscal expansion will be key in 2024

Source: Morgan Stanley Research, December 2023

Global flows likely to reverse in China’s favor

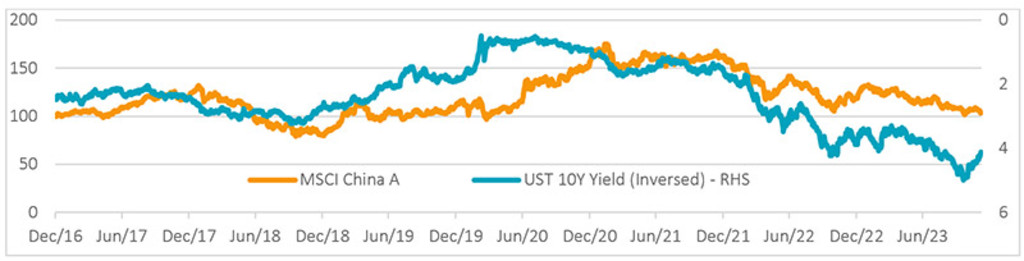

We anticipate the global macroeconomic environment to help China’s policymakers with Fed rate cuts reducing pressure on the CNY and promoting investment flows away from the US. US treasury yields have had a negative correlation with Chinese equity market performance over the last seven years. That will be important, given global asset allocation to China has been at very low levels with USD 100 billion withdrawn from China in 2023. There could also be a reaction from domestic investors with institutional investors including insurance companies starting to rebuild positions. Valuations are now at historic trough levels and retail investors are capitulating.

Figure 2: US Treasury yields have been negatively correlated with China equity market performance

Source: Bloomberg, MSCI, Morgan Stanley Research; data coverage from January 1, 2017 to December 7, 2023. Note: RHS axis refers to MSCI China A performance indexed to 100 as of Jan 1, 2017 while LHS axis refers to US 10Y treasury yields (%) inversed.

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Contrarian thinking

Rather than seeing this as a crisis, we continue to take a constructive view that this is a long term buying opportunity for active investors with local market knowledge seeking exposure to some of the world’s best companies. In our China strategies we are employing a barbell strategy focusing on value with cyclical upside as well as structural growth.

Footnote

1 ‘Signal from the Central Economic Work Conference is enlightening’ - Global Times, 13 December, 2023