Investment Specialist

Subscribe - Indices Insights

Receive an update as soon as a new article is available with insights about sustainability, factors or markets.

We unpack the merits of different carbon metrics used to gauge climate risk in portfolios, including a new climate beta measure. These are discussed with climate strategist, Lucian Peppelenbos, climate data scientist, Thijs Markwat, and Head of Sustainable Index Solutions, Joop Huij, in our roundtable interview.

Many industry participants – both asset owners and asset managers – are committing to net-zero targets to combat climate change and contribute to the low-carbon transition.1 This transition also triggers the question on how to assess the exposure companies have to so-called transition or climate risk. For instance, to what extent can we rely on traditional carbon emissions data and do we need additional measures to get a clearer picture? We tackle these issues by combing through the climate data forest with our in-house experts Lucian, Thijs and Joop.

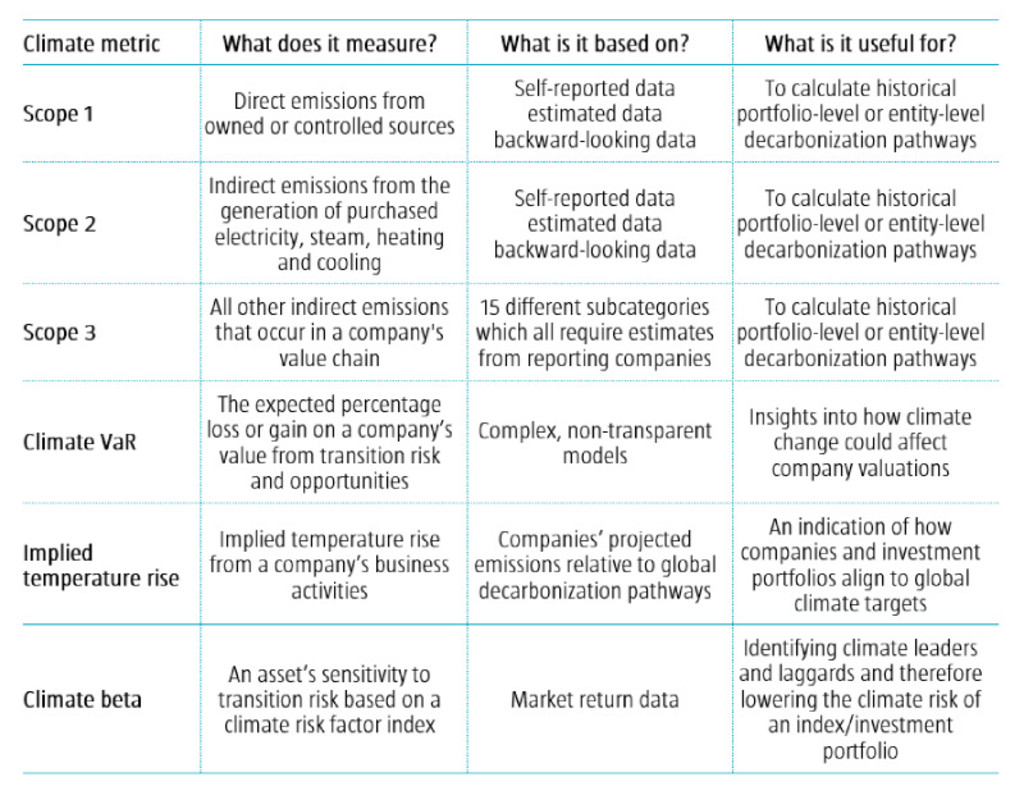

Thijs Markwat: “In general, the quality of Scope 1 and 2 carbon emissions data is relatively good. This stems from the clear guidelines outlined in the Greenhouse Gas (GHG) Protocol on how to calculate and report these emissions. The widespread use of this data also ensures that its quality improves over time. Currently there are several data providers that produce and supply carbon emissions data. In our view, such competition is beneficial for the accessibility and quality of the data.”

“But carbon emissions data does have some less attractive features. For instance, the data is backward-looking with possible lags of over two calendar years. As a result, it does not reflect the recent actions taken by companies to reduce emissions. Another disadvantage is that not all companies report their carbon emissions. In general, we see that smaller firms and those from emerging markets have a lower reporting rate. To address this issue, data providers use their in-house models to calculate estimates for companies that fail to report their data. We observe that these estimates can be significantly different between data providers. Thus, this raises the question on their reliability.”

T.M.: “In my view, Scope 3 currently poses one of the biggest carbon accounting challenges. Aside from the issues that plague Scope 1 and 2, there are additional concerns that are specifically associated with Scope 3. Although the GHG Protocol also outlines how to calculate Scope 3 emissions, this is a significantly more complicated task than for Scope 1 and 2. One complexity is that Scope 3 has 15 different subcategories which all require estimates from reporting companies. Moreover, the quality of reported data is often mediocre or even poor. Consequently, the estimates – which are often based on the reported data – are of lesser quality. For example, Scope 3 data can contain large outliers that lead to a single company dominating a portfolio’s carbon footprint.“

“Apart from the data quality, there is also the fundamental problem of double counting. As Scope 3 measures all emissions along companies’ supply chains, longer supply chains typically lead to higher emissions. Therefore, Scope 3 emissions are less transparent, and as a result, less comparable between companies. There are currently no good methodologies available to resolve this double counting issue.”

Joop Huij: “While climate risk has become a key issue for most investors, there are inherent difficulties in addressing it, some of which are data-related. Carbon emissions data gives a good indication, but it is not designed to gauge transition risk. Climate value at risk (VaR) measures – as developed by various data providers – are based on complex, opaque models and produce divergent results between different providers depending on their assumptions. Against this backdrop, we embarked on a project which was based on proposing a solution to these issues. Specifically, we introduced a measure of transition risk exposure that is determined by how an asset’s return is correlated with a climate risk factor, namely climate beta.”

“Climate beta is not based on a model with many assumptions. Its premise is that the market is relatively efficient in pricing in near and medium-term transition risk. Climate beta incorporates current market-based information (no two-year lag) and market expectations, thus making it a more actual and forward-looking measure. It has wide coverage, as market data is available for virtually all listed companies, and has high transparency, as it is not dependent on voluntary disclosures. And perhaps its most attractive feature is that it not only identifies companies that are vulnerable to the low-carbon transition (climate laggards), but also identifies those that are expected to benefit from it (climate leaders). This is something generic emissions data is not able to do.”

J.H.: “In our paper,2 we articulate the climate beta3 concept – which was initially termed ‘carbon beta’ – in detail. Climate transition risk metrics can be difficult to backtest given the lack of historical data and established methods to define when climate risk is high. In our research, we look to overcome this issue by creating a series of tests which can capture periods of climate policy uncertainty and climate change opportunities. We then outline how an asset with a negative climate beta tends to have high returns when climate policy uncertainty increases, and vice versa.”

“In our analyses, we observe robust associations between climate beta and emission footprints and intensities, and green innovation scores. We also see that stocks with higher climate betas have lower returns in periods of elevated climate risk, and vice versa. Furthermore, we look into green innovation and find that within industries, companies with lower climate betas are usually more active in patenting green technologies. This relationship, however, does not exist when one analyzes a firm’s emissions or emission intensity. Therefore, we believe climate beta is an additional climate risk indicator above and beyond traditional carbon data.”

Receive an update as soon as a new article is available with insights about sustainability, factors or markets.

Lucian Peppelenbos: “There is no single metric that can fully capture climate risk. Therefore, we continuously evaluate our climate analytics toolkit and strive to find ways to enhance or expand it. At Robeco, we develop our own fundamental views on the decarbonization pathways for companies in the heaviest emitting sectors, and we complement this with information from external data providers to obtain wider coverage of the investment universe. Climate change is unprecedented, thus we cannot rely on historical data. Key metrics change as climate scenarios evolve. That is why we believe continuous improvements to our toolkit are crucial to help our clients meet specific climate objectives.”

“So when Joop and I discussed the climate beta measure for the first time about two years ago, I was immediately intrigued by the concept. This is because it has a totally different starting point than carbon emissions data and climate VaR metrics. It can, therefore, complement our toolkit. To highlight Joop’s earlier points, what distinguishes climate beta is that it has forward-looking properties, it has broad coverage based on market data instead of self-reported data, and perhaps most importantly, it helps to differentiate climate leaders from laggards.”

L.P.: “Climate leaders are companies that are expected to benefit from the low-carbon transition. For instance, this could be fueled by green innovation or steps taken towards significant carbon footprint reduction. On the other hand, climate laggards are firms that are expected to be vulnerable to the low-carbon transition. As an example, this could be due to slow decarbonization efforts or business models that are economically linked to a high-carbon economy. All of this is forward-looking, which generic carbon emissions data is not designed to measure.”

“Green innovation provides a good reference point in identifying potential climate leaders. The climate beta research paper outlines how green innovation is driven primarily by the energy, materials and utilities sectors. Within these industries, the more innovative firms have lower climate betas, although they do not necessarily have lower carbon emissions or emission intensities. A good example is a US multinational that is active in the field of power generation. Despite ranking in the top 5% of GHG emitters in our sample, it is also one of the top three issuers of green patents. Thus, its climate beta is among the lowest in the industrials sector. On the other hand, some companies that look ‘clean’ based on their low reported emissions data actually have a high climate beta. For instance, some smaller firms that provide services to the oil & gas sector do not have high-carbon emitting operations, but they are economically vulnerable to a low-carbon transition.”

T.M.: “This is an easy one for me. One of the biggest problems that affects carbon footprint metrics is that funds which invest in companies that offer climate solutions often score poorly on Scope 1, 2 and 3 emissions, particularly Scope 3. Joop recently showed me how the same funds score well on climate beta. In my view, this demonstrates how climate beta better reflects the climate change awareness of these funds. Thus, it is indeed better suited to distinguish between climate leaders and laggards.”

T.M.: “Yes, there are many different alternative measures of transition risk and this number is continuously growing. But in my view, the main drawback for most of these metrics is the lack of transparency. In most cases, complex models are used to estimate transition risk. Climate beta, on the other hand, is an intuitive measure and its calculation is straightforward. It simply measures an asset’s sensitivity to transition risk based on market return data.”

“What I also like about climate beta is that it does not use carbon emissions as a direct input, like climate VaR or implied temperature rise metrics. If emissions are a direct input, we typically see that high carbon-emitting companies score poorly on such transition risk metrics. However, some high carbon-emitting companies can be well positioned for the transition given that they contribute positively to the shift towards a greener economy. Climate beta, on the other hand, is not directly dependent on emissions and is therefore better suited to identify these companies.”

J.H.: “We will impose an index-level restriction on our SDG Low-Carbon Indices – launched in December 2021 – which will result in meaningfully lower climate betas (transition risk) for our sustainable indices versus their respective market cap-weighted indices. The impact of this restriction is particularly noticeable in the weights of index constituents with very low climate betas (more weight) and high climate betas (less weight). We believe this makes our sustainable indices less exposed to transition risk which should be helpful in times when investors are especially concerned about climate policy uncertainty. We can also develop customized indices for clients that place more emphasis on climate risk (climate beta and carbon footprint reduction) to better position their portfolios for the transition.”

L.P.: “We are currently exploring this. As an example, climate beta can potentially enhance Robeco’s proprietary SDG framework by providing additional information that can be used for determining SDG scores for companies, particularly for climate-related SDGs. It can be used as a screen or an idea generator for fundamental research. We are also investigating if we can use the climate beta measure as a climate risk input in our investment processes alongside other climate metrics.”

J.H.: “We will estimate the measure based on a specifically designed climate risk factor index. This index tracks the return difference between a basket of ‘polluting’ stocks and a basket of ‘clean’ stocks. In addition to using climate beta to lower the climate risk for our sustainable indices on an index level, investors could also design portfolios or swaps based on the climate risk factor which could act as an overlay to lower the transition risk of their overall portfolios. Going forward, we expect to experience times of heightened climate policy uncertainty and believe that climate beta could be used as an input to temporarily hedge portfolios during those periods. We also believe that the measure could be interesting for investors with business models that are exposed to transition risk and who would like to assess and mitigate this exposure.”

Source: Robeco

1 Robeco, March 2022, “2022 global climate survey”, Robeco publication.

2 Huij, J., Laurs, D., Stork, P. A., and Zwinkels, R. C. J., November 2021, “Carbon beta: a market-based measure of climate risk“, SSRN working paper.

3 The methodology and calculation of the climate risk factor and climate beta are explained in detail in the above research paper.

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会

重要なお知らせ 当社や当社役職員を装ったSNSアカウントやウェブサイト等を使った投資勧誘にご注意ください さらに表示