Chief Researcher

• Vision

Repenser l’exceptionnalisme américain : Arguments en faveur de la diversification

Depuis des années, une conviction domine les marchés : privilégier les États-Unis et délaisser le reste du monde. Pour certains investisseurs, ce positionnement n’était même pas un choix délibéré. Il s’est progressivement imposé, porté par les performances relatives, l’évolution des indices de référence et l’effet cumulatif des flux se concentrant discrètement sur les segments les plus performants. Aujourd’hui, cette hypothèse mérite d’être examinée de plus près.

Résumé

- L’exceptionnalisme américain n’est plus une évidence

- Un vaste univers d’opportunités attractivement valorisées se cache sous vos yeux

- Allier diversification et génération d’alpha peut contribuer à renforcer la résilience d’un portefeuille

Il ne s’agit pas ici de remettre en question les États-Unis, qui demeurent le marché des capitaux le plus profond au monde, le pilier de la liquidité mondiale et un moteur majeur de l’innovation. Mais cela soulève une question plus nuancée : les investisseurs peuvent-ils encore tabler sur la poursuite de l’exceptionnalisme américain ?

Les marchés sont souvent analysés sous l’angle des cycles : inflation, taux, croissance. Mais le changement que l’on observe aujourd’hui ressemble moins à un revirement conjoncturel cyclique classique qu’à une transition structurelle. Pendant des décennies, les marchés mondiaux ont évolué autour d’une seule monnaie de réserve, d’un seul centre majeur d’innovation et d’une destination privilégiée pour les capitaux internationaux. Les États-Unis ont particulièrement bien rempli ce rôle. Ce système n’est pas en train de s’effondrer, mais il évolue.

L’objectif n’est pas de réduire l’exposition aux États-Unis, mais de limiter la dépendance à une seule source de rendement

L’activité économique, l’innovation et le capital humain se diffusent progressivement à travers les différentes régions. Les flux de capitaux s’ajustent légèrement. Parallèlement, les risques spécifiques aux États-Unis liés à la politique commerciale, à la viabilité budgétaire et à la position géopolitique du pays sont revenus sur le devant de la scène comme ils ne l’avaient pas fait depuis des années. Pendant la majeure partie des quinze dernières années, les risques politiques et macroéconomiques ont surtout été associés à l’Europe et aux marchés émergents. Cette hypothèse est de plus en plus remise en question.

Les actifs non US pourraient s’affirmer avec un rôle moins central des États-Unis

Cela ne signifie pas pour autant que les États-Unis doivent connaître un affaiblissement structurel pour que les actifs non américains surperforment. Peut-être ont-ils simplement besoin d’une Amérique moins dominante. La croissance du revenu disponible réel s’est ralentie dans un contexte d’inflation persistante, tandis que les déficits budgétaires élevés, l’augmentation de la charge d’intérêt de la dette publique et les marges bénéficiaires américaines proches de niveaux historiquement élevés suggèrent un environnement moins favorable aux valorisations.

Le risque d’un leadership trop concentré

Une autre évolution marquante de ces dernières années est la concentration croissante du leadership sur les marchés actions. Une poignée d’entreprises américaines à méga-capitalisation, principalement issues des secteurs de la technologie et de l’intelligence artificielle, a généré une part disproportionnée des performances mondiales. Des résultats solides, l’expansion des valorisations et la repondération des indices ont créé un cercle vertueux : les performances ont attiré les flux de capitaux, qui ont soutenu les capitalisations boursières, renforçant à leur tour la concentration du marché.

À y regarder de plus près, l’exceptionnalisme américain s’est donc progressivement transformé en un exceptionnalisme de plus en plus concentré. Cet aspect est important, car les portefeuilles construits autour de cette concentration pourraient se révéler plus fragiles qu’ils ne le paraissent. L’histoire est claire sur un point : le leadership sur les marchés actions finit toujours par tourner.

L’opportunité qui se cache sous vos yeux

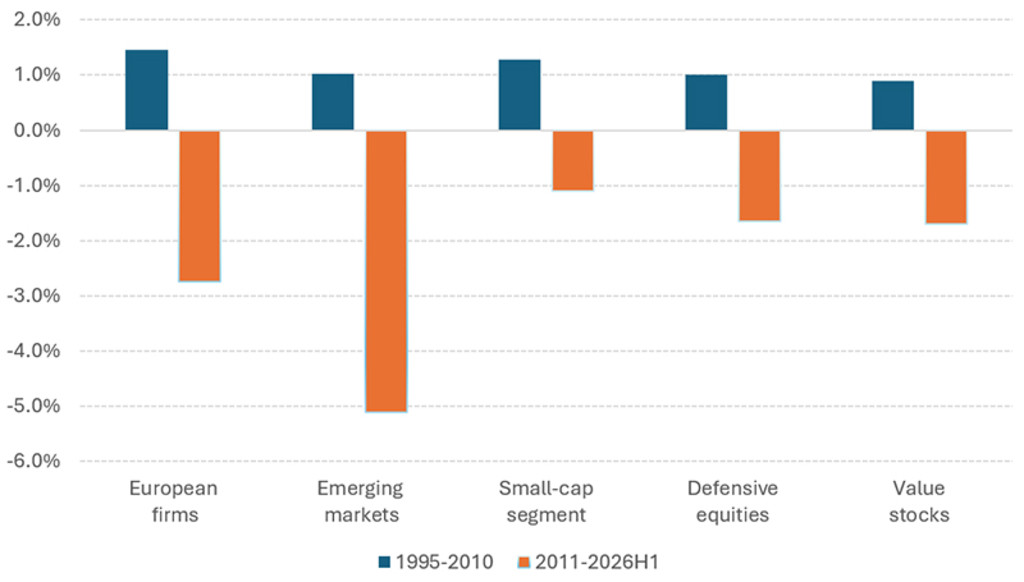

Au-delà des valeurs « growth » américaines à grande capitalisation se cache un large éventail de segments actions qui ont été négligés, voire dans certains cas activement évités, pendant la majeure partie des 15 dernières années. Il s’agit notamment des actions européennes, des marchés émergents, des petites capitalisations, des valeurs défensives et des titres « value ». Chacun d’entre eux a enregistré des performances nettement inférieures à celles des marchés mondiaux au cours de la période récente. Mais c’est précisément en raison de cette sous-performance que les allocations ont diminué, et que l’opportunité pourrait désormais se cacher sous vos yeux.

Si l’on élargit la perspective historique, la situation apparaît sous un autre jour. Au cours des 16 années ayant précédé la récente période de domination américaine, ces segments ont enregistré une surperformance significative, à des moments différents et dans des environnements de marché variés, plutôt que simultanément.

Graphique 1 – Performance relative par rapport à l’indice MSCI ACWI, de janvier 1995 à juin 2026

Les performances passées ne préjugent pas des performances futures. La valeur de vos investissements peut fluctuer.

Source : LSEG, MSCI, Robeco. Pour le marché mondial, nous utilisons l’indice MSCI All Country World Investable Market Index (ACWI IMI), tandis que pour les alternatives contrariantes, nous prenons en compte l’indice MSCI Europe pour les entreprises européennes, l’indice MSCI Emerging Markets pour les marchés émergents, l’indice MSCI All Country Small Cap pour le segment des petites capitalisations, l’indice MSCI World Minimum Volatility pour les valeurs défensives, et l’indice MSCI All Country World Investable Value pour les titres « value ». Les données sont disponibles de janvier 1995 à juin 2026. Toutes les performances sont exprimés en performances totales et libellées en dollars américains.

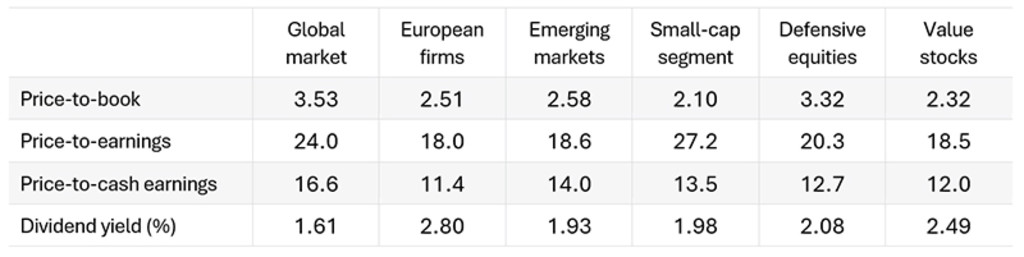

Aujourd’hui, elles présentent également une autre caractéristique commune : chacune d’entre elles se négocie avec une décote significative par rapport au marché dans son ensemble, qu’il s’agisse des ratios cours-valeur comptable, cours-bénéfice, bénéfice cours-flux de trésorerie et rendement du dividende.

Tableau 1 – Valorisations au 30 juin 2026

Les performances passées ne préjugent pas des performances futures. La valeur de vos investissements peut fluctuer.

Source : LSEG, MSCI, Robeco. Pour le marché mondial, nous utilisons l’indice MSCI All Country World Investable Market Index (ACWI IMI), tandis que pour les alternatives contrariantes, nous prenons en compte l’indice MSCI Europe pour les entreprises européennes, l’indice MSCI Emerging Markets pour les marchés émergents, l’indice MSCI All Country Small Cap pour le segment des petites capitalisations, l’indice MSCI World Minimum Volatility pour les valeurs défensives, et l’indice MSCI All Country World Investable Value pour les titres « value ». Les données sont disponibles de janvier 1995 à juin 2026.

Cinq segments, cinq moteurs de performance différents

Il est essentiel de souligner qu’il ne s’agit ni d’une opération isolée ni d’un pari macroéconomique unique. Les performances récentes l’illustrent bien : les marchés émergents ont signé de solides performances, contrairement à plusieurs autres segments, ce qui confirme qu’ils n’évoluent pas de concert et ne sont pas guidés par les mêmes facteurs. L’Europe, les marchés émergents, les petites capitalisations, les valeurs défensives et les titres « value » sont chacun portés par des facteurs de performance différents.

L’Europe pourrait bénéficier d’une reprise tirée par les mesures budgétaires et d’une réduction des primes de risque.

Les marchés émergents pourraient bénéficier de la bonne santé du secteur manufacturier mondial et des effets positifs liés à la dépréciation du dollar.

Les petites capitalisations ont tendance à réagir à la baisse des coûts de financement et à l’évolution de la demande intérieure.

Les valeurs défensives peuvent offrir une certaine résilience dans les contextes d’aversion au risque.

Les titres « value » pourraient tirer parti d’une hausse des taux, qui exercerait une pression sur les multiples des titres « growth ».

C’est là tout l’intérêt de la diversification. La question n’est pas de savoir quel segment sera le prochain à surperformer. Dans la pratique, cela est extrêmement difficile à prédire. Le fait est que différents régimes de marché favorisent différents segments, tandis que le moment de ces transitions demeure par nature incertain. Le véritable risque est de ne pas être positionné au moment où le leadership change.

QI Emerging Markets 3D Active Equities D EUR

- performance ytd (30-6)

- 36,28%

- Performance 3y (30-6)

- 26,25%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Paiement de dividendes (30-6)

- No

Les performances passées ne préjugent pas des performances futures et ne sont pas constantes dans le temps.Annualisé (pour les périodes supérieures à un an). Les performances s'entendent nettes de frais et en fonction des prix de transaction.

La diversification exige de la rigueur

La diversification est certes nécessaire, mais elle ne suffit pas à elle seule. Elle élargit l’éventail des possibilités, mais ne garantit pas de meilleurs résultats. La mise en œuvre est essentielle. Dans les périodes d’incertitude, les investisseurs adoptent souvent un comportement procyclique : ils se tournent vers les valeurs qui ont récemment bien performé, délaissent celles qui sous-performent et opèrent une rotation trop tardivement. Paradoxalement, les segments qui contribuent le plus à la diversification sont souvent ceux que les investisseurs ont le plus de mal à conserver pendant les phases de sous-performance.

C’est là que l’investissement quantitatif peut être utile. Un processus rigoureux, fondé sur des règles, permet de limiter les biais comportementaux susceptibles de nuire aux performances à long terme. Plutôt que de chercher à anticiper les fluctuations du marché ou de s’appuyer sur des convictions à court terme, une approche systématique applique une discipline d’investissement cohérente à l’ensemble des régions, styles et segments de marché. Cela permet aux investisseurs de rester exposés à un large éventail d’opportunités, même lorsque les performances récentes compliquent cette approche.

L’approche quantitative de Robeco s’appuie sur des décennies de recherche consacrées aux facteurs de performance dont l’efficacité a été démontrée empiriquement, tels que la valorisation, la qualité, le momentum, les révisions des analystes et les signaux à court terme. Ces facteurs ont été optimisés au fil du temps et s’inscrivent dans un cadre cohérent de construction de portefeuille qui vise à trouver un équilibre entre potentiel de rendement, maîtrise du risque et diversification.

La gamme de stratégies quantitatives de Robeco

Les stratégies d’indexation optimisée (Enhanced indexing) sont conçues comme des alternatives intelligentes aux stratégies passives ; elles visent à générer des écarts de performance réguliers tout en restant relativement proches de l’indice de référence. Les stratégies quantitatives actives visent à générer un alpha supérieur dans un cadre de risque maîtrisé, ce qui en fait une solution adaptée aux investisseurs souhaitant améliorer la performance de leur portefeuille. Les stratégies défensives, ou conservatrices, privilégient une exposition aux actions à moindre risque et visent à améliorer la trajectoire de performance en limitant les baisses. Les stratégies « value » ciblent une prime de rendement éprouvée sur le long terme, alors que les stratégies petites capitalisations « next-gen » tirent parti de données avancées, de signaux affinés et des techniques de machine learning pour générer de l’alpha dans un segment de marché vaste et moins bien couvert par la recherche.

Constituer des portefeuilles pour un monde plus incertain

Si les marchés évoluent d’un régime de concentration vers un régime plus dispersé, les portefeuilles doivent s’adapter en conséquence. L’objectif n’est pas de réduire l’exposition aux États-Unis, mais de limiter la dépendance à une seule source de rendement. Dans un monde où l’exceptionnalisme n’est plus une évidence, la résilience devient l’atout décisif. Cette résilience ne repose pas sur la capacité à anticiper le prochain leadership, mais sur une diversification réfléchie et une mise en œuvre disciplinée.

Investing beyond the US

Opportunities in global equities, emerging markets and Europe