The Investment Engineers

• Insight

Europe: a compelling alternative to US markets

Over the past 12 months, it has become increasingly evident that a rebalancing is underway among large asset allocators as they reassess the regional diversification of their portfolios.

Summary

- While the US faces headwinds, European credit markets remain resilient

- High valuations and concentration in the US make Europe’s equities attractive

- Europe’s broad opportunity set favors systematic, multi-factor stock selection

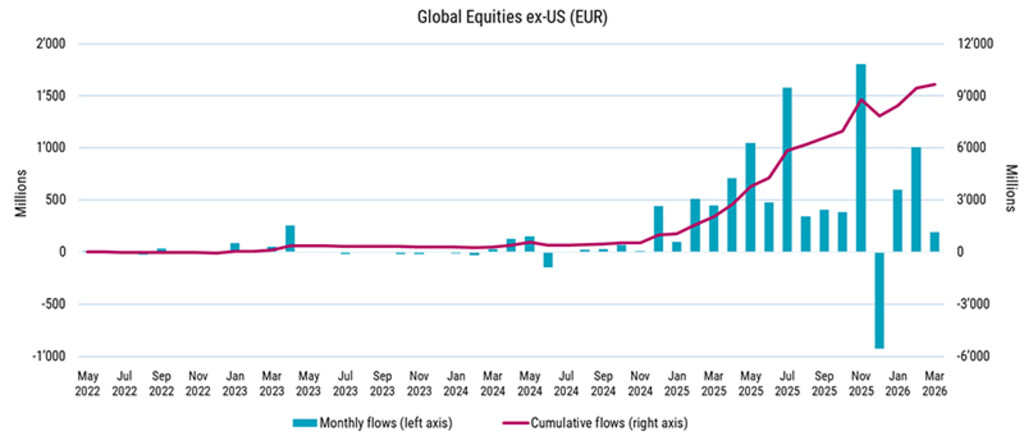

After more than a decade of US equity outperformance, capital flow data indicates a shift away from the US. This is not due to a collapse in the US economy or a lack of long-term appeal, but because relative opportunities elsewhere are becoming more compelling. Rising geopolitical uncertainty, alongside questions around how AI investment will be funded and how it will reshape industries, is strengthening the case for broader diversification. Combined with high valuations and mega-cap concentration risk, this is prompting investors to reinterpret the global risk and opportunity set for 2026.

Figure 1 – Equity flows are moving out of the US and across the globe

Source: Broadridge, Robeco, May 2026

At the same time, the growing dominance of US asset managers means a significant share of global capital allocation is increasingly influenced by US-based institutions. This can reinforce home bias and crowding, leaving opportunities in other regions underexplored.1

Europe, in this context, acts as a complementary allocation, offering a different sector mix and, in many cases, a less crowded and more defensive opportunity set. Here we offer some diverse strategies which Robeco has on offer, including credits, ‘green’ sovereigns, quantitative, and fundamental equities, that capture the advantages that now characterize European assets.

Despite a more volatile macro backdrop, credit markets have remained relatively resilient. Liquidity conditions have stayed supportive, with strong demand helping to absorb issuance and underpin market stability. At the same time, yield-driven inflows, higher starting yields and solid technicals continue to support the asset class. Within this context, regional dynamics are becoming more differentiated. Europe may face some sensitivity to energy dynamics, but US credit markets are contending with their own headwinds, including private credit stress and AI-related disruption. This reinforces the case for a more balanced regional approach.

Robeco Euro Credit Bonds is an actively managed strategy providing diversified exposure to euro investment grade credits. The strategy combines top-down positioning with fundamental issuer selection, with increasing dispersion across sectors and issuers creating a richer opportunity set for active management. European banks remain a key area of strength, supported by solid balance sheets and improved profitability in a more normalized rate environment. Alongside this, select infrastructure and industrial-related sectors are benefiting from increased fiscal spending across Europe, particularly in areas such as defense and infrastructure.

The strategy maintains a consistent quality bias, focusing on issuers with resilient cash flows and strong balance sheets. The shorter duration profile of euro credit, with an average duration of around five years, provides an additional source of resilience in the current environment.

Euro sovereigns with a climate tilt

In Europe, climate policy and sustainability are more deeply embedded in the investment landscape than in the US. Robeco’s Climate Euro Government Bond ETF invests in euro-denominated sovereign bonds while tilting toward countries that are making stronger progress on the climate transition and increasing their exposure to green bonds. The strategy is designed to closely match the yield and duration profile of the broader euro government bond market, allowing investors to align with climate objectives while maintaining the defensive role of sovereign bonds in portfolios.

European equities: From underowned to reconsidered

The outlook for European equities, while clouded by the rise in energy prices and the ECB inflation forecast, still offers a fertile environment for stock pickers. European companies offer more balanced sector exposure compared to the US market, which remains heavily concentrated in technology.

Valuations also remain supportive. European equities continue to trade at a discount to their US counterparts, both on a relative and historical basis. At the same time, global benchmarks have become increasingly concentrated: today, the US accounts for more than 60% of the MSCI ACWI, compared to a much smaller allocation to Europe. For equity investors seeking to rebalance portfolios and reduce concentration risk, this creates a strong case for reconsidering regional allocations.

Positioning further reinforces this argument. After years of outflows and underperformance, recent inflows suggest that sentiment may be starting to shift. In recent years, between 2022 and 2024, European equity funds experienced persistent outflows, even as global and US-focused strategies attracted capital. More recently, however, this trend has begun to evolve, with flows into US equities moderating and broader global allocations gaining traction. As geopolitical pressures ease or stabilize, the relative appeal of Europe becomes more visible, reinforcing its role as a diversification tool within global portfolios.

Against this backdrop, investors are increasingly looking for ways to capture these opportunities. Robeco European Stars Equities is an actively managed strategy investing in high-quality European companies with attractive valuations. This results in a concentrated portfolio designed to capture market inefficiencies and deliver long-term outperformance across both financial and sustainability dimensions.

Why a quant approach fits European equities

Europe’s opportunity set is broad and diverse, with less dominance from a narrow group of mega-cap stocks than in the US. As a result, returns are more evenly distributed, and the ability to differentiate between companies becomes more valuable. A quantitative approach is well suited to this environment, as it can consistently evaluate a large universe of stocks using multiple enhanced signals, including value, quality, momentum, analyst revisions and shorter-term indicators.

Importantly, this approach does not rely on a single market view or a binary call on regional rotation. Instead, it is designed to capture opportunities wherever they emerge, adapting to changing market conditions while maintaining a diversified set of return drivers.

At the same time, portfolio construction plays a critical role. In European equities, country, sector and currency exposures can meaningfully influence outcomes. A benchmark-aware quant process helps manage these risks by controlling unintended deviations, limiting concentration, and incorporating transaction costs and liquidity considerations directly into the investment process.

The result is a disciplined approach that seeks to deliver consistent, risk-controlled outperformance in a more complex and evolving market environment. Within this framework, Enhanced Indexing offers a disciplined alternative to passive investing, while Active Quant strategies aim to deliver higher excess returns with a strong focus on risk control.

Looking beyond the US

Europe is unlikely to replace the US at the core of global portfolios. However, as investors seek to rebalance exposures and broaden their opportunity set, it is increasingly being viewed as a complementary allocation. Across credit, government bonds and equities, Europe offers a combination of diversification, resilience and selectivity that is becoming harder to ignore.

For active managers with deep roots in European markets, this creates opportunities to identify the companies, sectors and themes best positioned to navigate a changing environment. With decades of experience investing across European asset classes, Robeco combines local market insight with global perspective to help investors access these opportunities in a disciplined and selective way.

Footnote

1See: https://www.bruegel.org/policy-brief/risks-europe-us-dominance-global-asset-management

Is it time to diversify beyond the US?

This article is part of a three-part investment series aimed at exploring regional alternatives to US-centric growth.

Climate Euro Government Bond UCITS ETF EUR Acc

- SFDR (30-6)

- Article 8

- Dividend Paying (30-6)

- No

- Current Price (22-7)

- 5.06

- Inception date (30-6)

Past performance is no guarantee of future results. The value of the investments may fluctuate.

Euro Credit Bonds D EUR

- performance ytd (30-6)

- 0.97%

- Performance 3y (30-6)

- 4.47%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Dividend Paying (30-6)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

European Stars Equities D EUR

- performance ytd (30-6)

- 7.55%

- Performance 3y (30-6)

- 9.55%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Dividend Paying (30-6)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

QI European Active Equities D EUR

- performance ytd (30-6)

- 13.93%

- Performance 3y (30-6)

- 17.52%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Dividend Paying (30-6)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

3D European Equity UCITS ETF EUR Acc

- performance ytd (30-6)

- 12.88%

- SFDR (30-6)

- Article 8

- Dividend Paying (30-6)

- No

- Current Price (22-7)

- 6.70

- Inception date (30-6)

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.