Head of Sustainability Integration

• 市場觀點

SFDR – what asset managers need to know

The EU’s Sustainable Finance Disclosure Regulations (SFDR) are a set of disclosure rules designed to enhance the transparency and maintain the credibility of sustainable investing. We unpack what it means for asset managers in theory and how it’s evolving in practice.

概要

- SFDR is part of the EU’s ambitions to build a sustainable economy

- Deeper scrutiny of Articles 6, 8, and 9 reveals surprises

- Progress in practice is incremental and currently on pause

Regulation is a dirty word in many corners of business and politics, but sustainability regulations are desperately needed to accelerate the transition to cleaner, greener and more equitable economies. The EU has wasted no time in drafting legislative frameworks to steer its companies, industries, and trading partners toward sustainable profits and growth.

The EU Sustainable Finance Action Plan is just one part of the grand plan. Its overarching goal is to channel capital to sustainable investments and development across the 27-nation bloc. It does so through several underlying initiatives including the Sustainable Finance Disclosure Regulations (SFDR).

The SFDR is designed to ensure that capital intended for sustainable investments flows into bona fide sustainable products. To accomplish this, the SFDR requires asset managers to thoughtfully consider sustainability risks in their investment products, substantiate any sustainability claims based on objective criteria, and disclose those results publicly.

In addition to protecting investors from ‘greenwashing’, more data and disclosure should also arm them with more information to compare the merits and trade-offs of competing investment products.

Common misconceptions

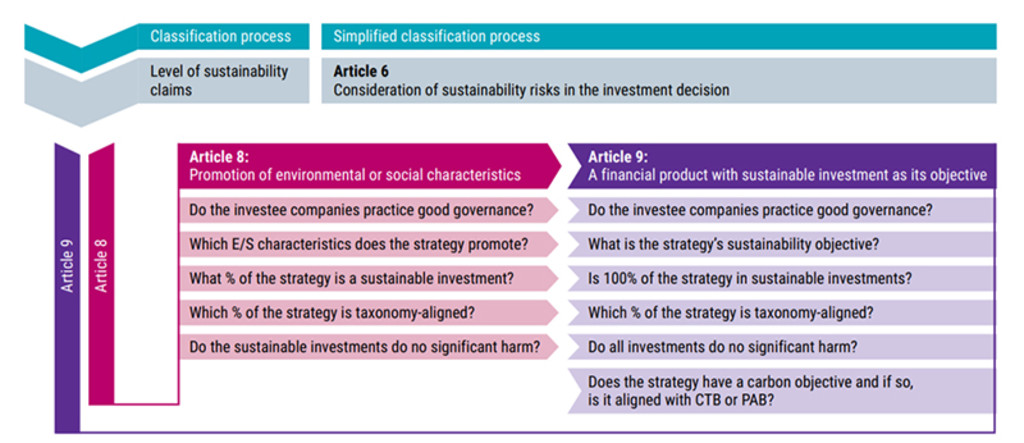

By now, the SFDR’s most famous feature is its classification system. Asset managers are required to classify all investment products as Article 6, 8, or 9.

Article 6 products have no sustainability goal but must disclose why that’s the case.

Article 8 products must demonstrate they promote environmental or social characteristics.

Article 9 products must pursue a clear sustainable investment objective.

Investment managers may be tempted to use these new classifications as a marketing label to increase their attractiveness. However, labels imply that products have been assessed using a strict set of standardized metrics and that’s not the case with SFDR. Though it requires reporting across common subject areas, there is still a wide range of variability between the sustainability features. At its core, the SFDR is a transparency measure that lets investors peer inside a product so they can understand what features make it sustainable.

The SFDR is a transparency measure that lets investors peer inside a product so they can understand what features make it sustainable

Another common error is assuming that Article 6 products are exempt from sustainability disclosures. SFDR requires all financial market participants to assess and disclose whether they integrate sustainability policies into their products, the likely impact of sustainability risk on returns, as well as if they consider the negative impacts their products may have on a special set of EU-defined indicators known as Principal Adverse Impacts (PAIs).1

Comparing Articles 8 and 9

Relative to Article 6, Articles 8 and 9 require more measurement and reporting across a broad range of sustainability metrics. Article 8 products must demonstrate they promote sustainability while Article 9 products must demonstrate they directly contribute to them. In addition, both classes must show they adhere to good governance and report to what extent they are using the ‘sustainable activities’ definitions of the EU Taxonomy.

Beyond these requirements, Article 9 portfolios are mandated to report on any negative effects their underlying securities may have on 18 (of 64) PAIs that include areas such as carbon emissions, waste disposal, human rights, and gender diversity. In contrast, Article 8 products need only to explain whether they consider PAIs in their investments.

Another distinction is that Article 9 must be fully invested in companies that are deemed sustainable, while Article 8 products need only state the share of sustainable investments they intend to make.

Figure 1 – How Robeco determines a product’s SFDR classification

Source: Robeco, April 2023

More clarity is critical

What constitutes a ‘sustainable investment’ however is not strictly defined. A wind farm investment may be sustainable for a clean energy strategy, but its poor worker-safety record may make it unacceptable for a portfolio focused on high performance on socially oriented factors. That lack of clarity is causing kinks and slowing SFDR’s progress.

Amendments have been proposed which include stricter technical standards and more rigor on PAI

assessments (i.e., not just whether but how PAIs are applied to investments). However, it may take years before these are vetted, approved, and implemented (if approved at all).

The EU Taxonomy’s classification system could provide a speedier solution, given both Article 8 and 9 classes require managers to already report how much their products align with the Taxonomy2. But that can’t be measured until investee companies themselves classify and report their sustainable activities. The CSRD, a separate sustainable finance directed aimed at corporate sustainability disclosure, requires larger companies (more than 500 employees) to report the Taxonomy alignment of their operations beginning already this year.

But given the costs involved, smaller companies still have years to comply. Moreover, the social part of the EU Taxonomy that defines which activities contribute positively to social impact, is still in development. Given these gaps in reporting, using the Taxonomy as an accelerated solution by year’s end is unlikely.

Where we are and where we’re going

For the time being, uncertainty over how rules will evolve has caused many managers to put a pause on further SFDR action plans. Despite the pause, rules are creating lots of dialogue and engagement. Moreover, progress at such scale and with so much impact is better done in increments.

Over time, we believe external pressure from stakeholders combined with technological advances in data capture and processing should push companies and the investment industry toward more integration and disclosure of sustainability risks and impact.

Read more on how sustainability is impacting finance and investments in our SI Big Book 2.0.

Footnotes

1PAIs are a specific set of impact indicators defined by the EU as “negative, material, or likely to be material effects on sustainability factors that are caused, compounded by, or directly linked to investment decisions and advice performed by the legal entity.”

2EU Taxonomy alignment is measured by % share of total portfolio holdings whose underlying business operations count as ‘sustainable activities’ based on EU Taxonomy technical criteria.

Important information

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.