• 市場觀點

Digital twins and machine vision: exciting themes of ‘smart’ production

Manufacturing as we know it is coming to an end. It is en route to become more flexible, increasingly digital and often closer to its end markets. Cyber systems and physical systems will connect, driving a trend towards ‘smart’ and more sustainable production. Within this trend, machine vision and ‘digital twins’ are becoming ever more important themes, says Robeco Industrial Innovation Equities portfolio manager Marco van Lent.

概要

- Industry 4.0 is about increasing digitization of products, value chains and business models

- Drivers of ‘smart’ production are big data, algorithms and stronger computing power

- ‘Digital twins’ and machine vision are two of this trend’s hottest themes

The main drivers of Industry 4.0 are big data, the emergence of algorithms to analyze this data, and advancements in software and hardware capabilities. Among demographic drivers, a strong push is coming from an aging workforce in countries such as China, but also in many developed countries.

Robeco Global Industrial Innovation Equities strategy, like every other Trends strategies, selects long-term growth trends driven by demographic, technological or regulatory changes. This strategy has benefited strongly from the ‘digitalizing production’ trend via investments in players that combine advanced manufacturing techniques with the Industrial Internet of Things (IIoT).

Digital manufacturing turns production into self-adapting systems with a shorter R&D cycle, raising quality and reducing costs. For example, Maserati has achieved a 50% reduction of time to market by implementing IIoT. Adidas is trialing two ‘speed factories’ that bring local production closer to local consumption through smart manufacturing and 3D printing; it has dramatically reduced time to market for a pair of sneakers from 12-18 months to only 30 days.

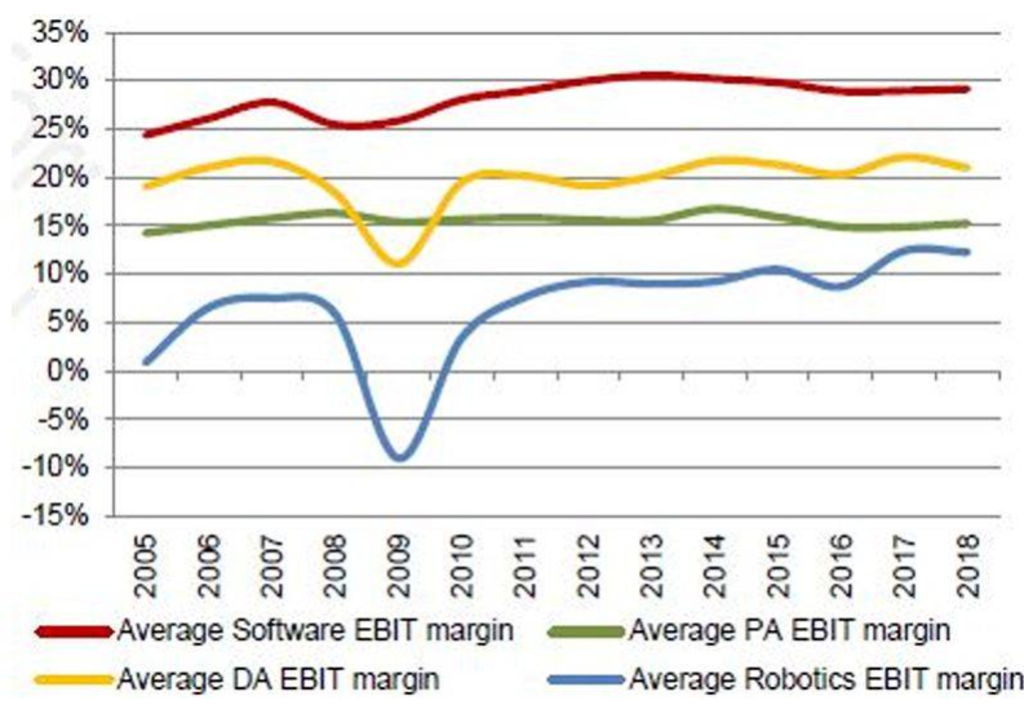

The global digital production trend is growing fast, and within it, the Industrial IoT – a network of platforms, connected devices and software – is growing the fastest. The Industrial IoT software market also has margins that are among the highest in the automated production universe.

EBIT margin by automation application

Source: Credit Suisse

Machine Vision

Being able to capture and process visual information in real time is absolutely critical for ‘smart’ manufacturing. This is called machine vision – it transfers images to a computer and enables almost instant feedback into the process. “I personally like machine vision a lot. It adds vision to machines to perform online testing and checking. This means you can have this done at all stages along the production line much earlier in the process and not just at the end, when the product is already finished,” says Van Lent.

Machine vision relies on lighting instruments, lenses, image sensors and vision processing. Used in the automotive, pharmaceutical, printing, food, and other sectors, machine vision is now able to not only work as a replacement for human vision, but also to handle information invisible to the human eye. According to Credence Research, the machine vision market is expected to reach USD 15 bln by 2022 from the current level of USD 9 bln.

Digital Twins

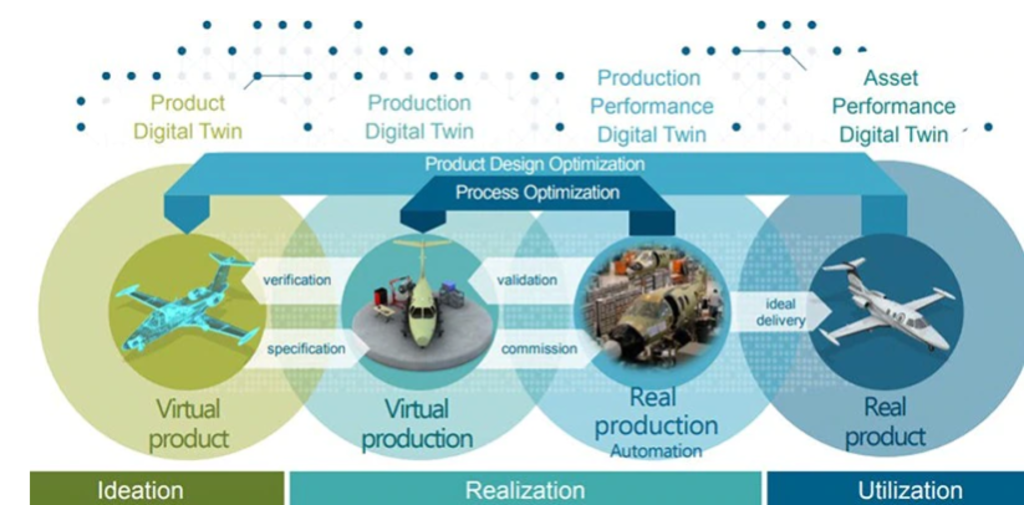

Digital twins are virtual representations of physical products or processes that can be used to understand, predict and optimize their performance. It is yet another hot application of IIoT that research firm Gartner has put on its list of top 10 strategic technology trends for 2019.

Source: Siemens eAircraft

“Digital twins map the physical production process online; for example, for jet engines,” said Van Lent. “You don’t have to build test models directly, you can design and test them on the screen. Rolls Royce, for instance, stated that before ‘digital twins’, it would typically have damaged or destroyed several test engines. Now, it produces one core engine which has been operational in tests, with none destroyed.”

But you can also use digital twins in operation. “You can collect information from the jet engine when flying and feed it into the computer on the ground. This can run tests to see how the engine will react to, for example, an energy-saving solution. Then you send the data back to the airplane, and the pilot can adjust the engine’s settings,” explains Van Lent. The global digital twin market is expected to reach USD 36 bln by 2025 from the current level of USD 4 bln according to MarketsAndMarkets data.

Stages of the Gartner hype cycle

“Within the Trends Investing team we try to capture new trends early on. This has obvious risks attached to it, as, after the initial hype, technologies frequently fail to live up to people’s unrealistically high expectations,” says Van Lent. This is captured well by the so-called Gartner hype cycle. Expectations about a new technology will often lead to a ‘peak of inflated expectations’, after which a wave of ‘disillusionment’ sets in and the number of players drops. But once these technologies have overcome their teething troubles, some of them will take root and continue growing through the ‘slope-of-enlightenment’ phase on to the more stable ‘plateau of productivity’.

Various building blocks of Industry 4.0 are located at different stages of this hype cycle. Machine-learning technology is currently at the peak of expectations, while self-driving cars have entered the phase of ‘disillusionment’ already. At the same time, industrial robots have reached their plateau phase, with four manufacturers in the lead globally.

As for IIoT platforms, currently offered by around 500 companies, they are now just past the peak of the hype cycle. “The number of companies offering them will certainly drop, and it is difficult to pick the ultimate winner,” says Van Lent. “For this reason, at this stage of the hype cycle, you have to invest in a basket of names.”

It is important to note that there are no real pure-play companies offering these technologies. All companies in this market are developing and offering IIoT and other platforms on top of their existing businesses. “If they chose to stop their supply, their bread-and-butter business will continue. So the companies themselves will not disappear,” says Van Lent.

Cyclical nature of industrial automation

Digital manufacturing offers multiple opportunities for investors and this trend is currently still at an early stage. Only a handful of industries have meaningfully progressed along the digitization curve, with some, such as buildings, industrials or food and beverages, being the least digitized.

The incorporation of IIoT into factories is a growth market, yet it is cyclical in nature, cautions Van Lent. “This means that capex can drop abruptly, depending on macro developments, as the current trade dispute between the US and China demonstrates,” he said. “This makes the industrials sector very different from, say, the food industry, for which it is impossible to imagine demand dropping 10% overnight.”

獲取最新市場觀點

訂閱我們的電子報,時刻把握投資資訊和專家分析。

重要資料

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。