Strategist

獲取最新市場觀點

訂閱我們的電子報,時刻把握投資資訊和專家分析。

Despite all the focus on the inflation outlook and ongoing Fed hikes, the recent sell-off in US Treasuries was actually driven to a large extent by a reawaking of the term premium. Investors should be prepared for more of the same as the trend is set to continue. But be aware that quantitative tightening (QT) does not necessarily mean quantitative easing (QE) in reverse.

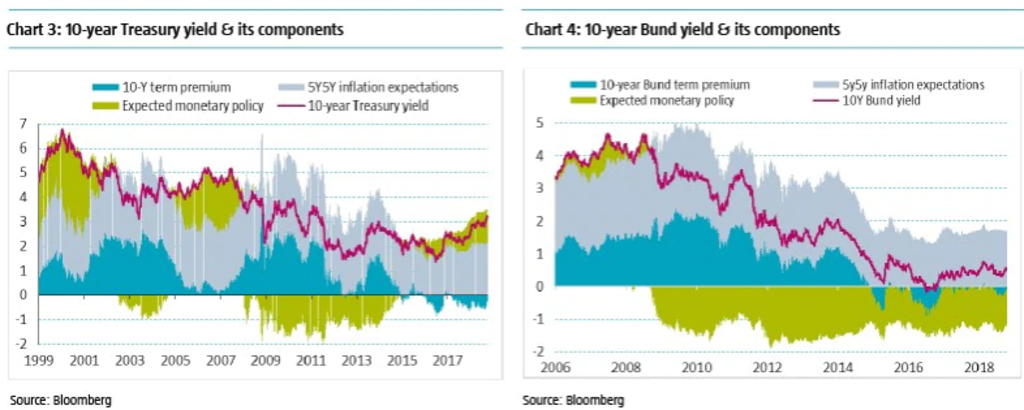

We can split long-term interest rates into three components: expected monetary policy, inflation expectations and the term premium. As the below Treasury and Bund charts show, term premium was by far the biggest driver of the upturn in yields.

Hawkish comments from the ECB affected bond markets too – albeit to a lesser extent – with President Draghi confidently concluding that wage growth would lead to “relatively vigorous underlying inflation”. The same cannot be said of inflation expectations. What is striking here is the sluggishness of inflation expectations in both the US and the Eurozone (grey areas in Charts 3 and 4); they did not react at all to the strong recovery in oil prices and wage growth in 2018.

Even following the modest recent upturn, term premiums (as shown by the blue areas in Charts 3 and 4) remain far below their pre-QE levels. But with global monetary policy normalizing, term premiums look set to turn positive and reassert themselves as the main driver of long-term yields. To understand the pace and impact on long-term yields, let’s examine the drivers of term premium in more detail.

訂閱我們的電子報,時刻把握投資資訊和專家分析。

The economy’s point in the business cycle is a powerful domestic driver of term premiums. In the US, with the exception of the 1973/74 oil crisis, the term premium expanded very quickly during all recessions since 1962, usually beginning just before recessions set in. That said, despite the recent term premium upturn, we do not see any imminent risk of recession over the next six to nine months. A number of Fed models assess the risk of a US recession in the next year at around 15%.

The present near-inverted yield curve – often interpreted as an indicator of a looming recession – is itself being distorted by the compression of the term premium (discussion further below). Other domestic drivers of term premiums, such as expected bond market volatility due to monetary policy uncertainty and changes to the inflation risk premium, have become less relevant since the advent of QE. That said, inflation surprises may still exert some upward pressures on term premiums and on yields. But the effect will probably only be temporary.

Global central bank liquidity and international portfolio rebalancing are major drivers of term premiums. This is visible in a remarkable synchronicity in term premiums in the US, the Eurozone and Japan, especially in the aftermath of QE policies by the main central banks. A key channel through which QE operated was via portfolio shifts by international bond investors.

In addition to the massive liquidity injections by the official sector (about USD 9 trillion), which extracted duration risk from the market, portfolio shifts in the private sector have also played a critical role. For example, over the summer of 2014, the market began to expect the ECB to launch a program of asset purchases. Investors ‘frontloaded’ the yield impact of this program by buying huge quantities of government bonds.

But in recent months global central bank liquidity has started to decline as the Fed has been shrinking its balance sheet more quickly. Against this backdrop, a gradual re-pricing of risk will likely occur and term premiums worldwide will normalize.

Global central bank liquidity will begin to shrink more quickly from Q1’19 on, as the ECB’s QE activity becomes limited to reinvesting maturity proceeds. In Japan the Bank of Japan has prepared the ground to end QE, with the likely extra flexibility in the 10-year yield target requiring fewer asset purchases.

QT will not have a reverse symmetrical impact to QE for two main reasons. First, it is clear that central banks are not aiming to bring their balance sheets back to pre-QE levels. It is quite probable they will stop before this, especially if a new recession would impact their economies. Hence a significant amount of duration risk will still be extracted from the market. Second, the normalization of unconventional monetary policy should lead to a global re-pricing of risk, reversing somehow the impact of QE that compressed risk premiums and triggered a search for higher returns in a very low yield environment. Tighter credit conditions may well encourage such portfolio rebalancing, given the very stretched valuations of IG securities. But for now, bank credit standards in the US are still easing and credit to the corporate sector appears quite resilient.

With QE buying and investor portfolio shifts concentrated in longer-dated bonds, 10-year yields have compressed relative to five-year yields, working counter to the principle that, given the greater exposure to interest rate risk, holders of longer-dated bonds should be compensated with higher term premiums. While the inversion was only temporary for Bunds and JGBs (in 2015 when the ECB launched its QE and in 2016 when the BoJ announced its policy of negative interest rates), for the US it has persisted throughout 2018.

As the inversion in the US term premium curve has been predominantly driven by global QE-related factors, the near-inverted yield curve has thus lost the power to predict domestic economic conditions that it had in previous economic cycles. Given that the US’s low 10-year term premium compared to Japan and the Eurozone is unrelated to the US economy’s more advanced position in the business cycle, we expect this anomaly to normalize, something that should tend to steepen the US curve.

Historically low – and still negative - Treasury and Bund term premiums mean that investors are effectively paying to hold duration risk, suggesting that many allocations are actually for regulatory or diversification reasons. Against a backdrop of normalizing global monetary policy and declining global liquidity, term premiums have to rise gradually. This is especially true in the US, where, in addition to these factors, a rising supply of Treasuries resulting from Trump’s fiscal measures will meet fading international demand.

Central bank liquidity will shrink only progressively and this has been carefully communicated by the Fed and the ECB. The lower demand for bonds from private international investors will intensify as a response to the rate hikes by the Fed throughout 2019, but will probably still have a limited impact in the coming months. All these factors must already be, at least partly, priced into current US term premiums and Treasury yields. So only surprises – geopolitical shocks, unexpected changes in monetary stance or on the inflation front – should trigger abrupt movements in term premiums.

Looking further ahead, possible shifts from credit to sovereign bonds could also serve to mitigate the term premium upturn. Hence, while recognizing the likely direction of travel and gradual pace of term premium moves, there is no reason to panic for now.

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.