Portfolio Manager

• Visie

Asia’s structural tailwinds come into sharper view

Asia-Pacific has been the region most severely impacted by the energy supply shock since the Middle East conflict broke out. Nevertheless, equity markets have outperformed both the US and Europe so far in 2026, reflecting the region’s centrality to global technology and innovation.

Auteurs

Portfolio Manager

Portfolio Manager

Client Portfolio Manager

Topzoekwoorden

Samenvatting

- Asia-Pacific equities have transcended the 2026 energy supply shock so far

- AI earnings strength and attractive valuations form a powerful combination

- Middle East trade disruption means volatility is likely to continue

MSCI Asia-Pacific, up 13.2% in the year to 30 April1, has recently outpaced MSCI USA (5.5%) and MSCI Europe (4.4%), with many portfolios remaining heavily concentrated in a narrow set of US companies. A combination of more attractive relative valuations, broadening economic momentum beyond the US, and shifting supply chains is creating a window for investors to reassess their regional allocations. The recent conflict in the Middle East triggered a broad risk-off move and a reset in valuations, but from a medium-term perspective that correction became an entry point, rather than undermining the fundamental Asia-Pacific equities story.

At the heart of the opportunity is Asia’s role in the artificial intelligence and digital infrastructure build out. While headlines typically focus on US chip designers and hyperscalers, much of the essential ‘picks and shovels’ infrastructure underpinning the AI era is produced in Asia. As new data centers proliferate globally, demand is rising for advanced cooling systems, networking equipment, precision components and power management solutions. Many of the critical suppliers in these niches, particularly across memory and semiconductor supply chains, are based in Japan, Korea and Taiwan, providing exposure to AI driven capex without relying solely on the most obvious semiconductor names. Energy is becoming another defining bottleneck for AI, and Asian power equipment and energy supply companies stand to benefit as utilities and corporates upgrade grids and generation capacity to meet soaring electricity needs.

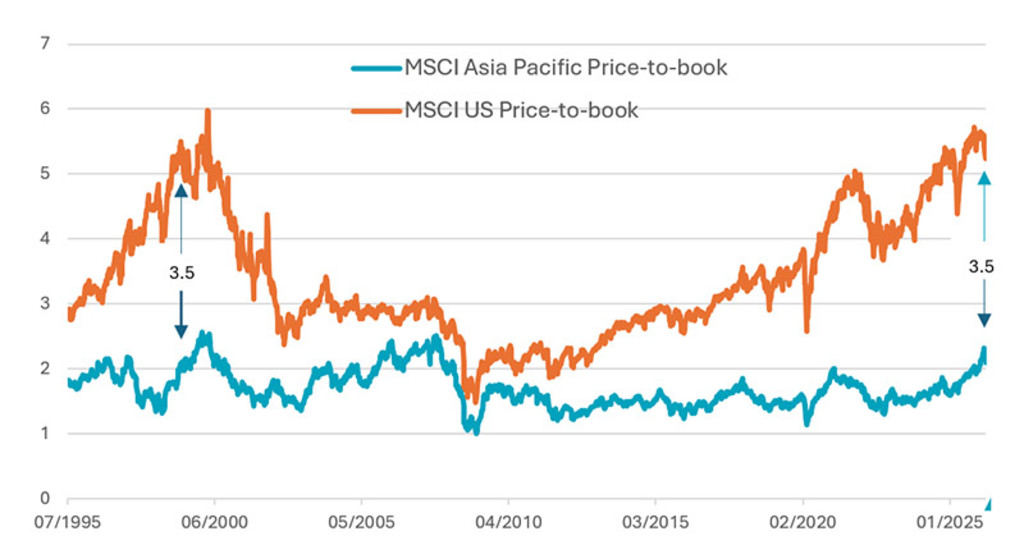

Valuations remain at a steep discount to the US

Valuations provide a second important pillar for the Asia-Pacific investment thesis (see Figure 1). With US markets having already enjoyed a long re rating, the scope for further multiple expansion appears limited, leaving future returns more dependent on earnings growth alone. By contrast, Asia still offers the potential for both earnings growth and some catch up re rating. Economic activity is picking up from a low base, and earnings revisions across Asia-Pacific are turning positive, supported by corporate reforms, strengthening domestic demand, and later cycle benefits from AI, infrastructure build outs and higher defense spending. Dividend yields also tend to be more attractive in Asia, giving investors an additional component of total return.

Asia-Pacific Equities F EUR

- performance ytd (30-6)

- 29,87%

- Performance 3y (30-6)

- 23,57%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Dividenduitkerend (30-6)

- No

In het verleden behaalde resultaten bieden geen garantie voor de toekomst. De waarde van uw beleggingen kan fluctueren.Geannualiseerd (voor periodes langer dan een jaar). De performance is gebaseerd op de koers na aftrek van kosten.

Figure 1: The valuation gap persists

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: Robeco, MSCI, 30 April 2026.

The long standing valuation gap between Asia and the US also reflects differences in market structure and perceptions of shareholder friendliness. US companies have been rewarded for higher leverage, aggressive buybacks and consistently high returns on equity. Historically, some Asian markets have lagged on corporate governance and shareholder return practices, dampening valuations despite solid business fundamentals. However, this picture is changing. Governance reforms in Japan and the ‘value up’ initiative in Korea are driving better capital allocation, higher payout ratios and more disciplined balance sheets, with buybacks and dividends becoming more entrenched. As these improvements broaden across the region and fundamentals continue to strengthen, there is clear scope for the valuation discount to narrow over time.

Ontvang de nieuwste inzichten

Meld je aan voor onze nieuwsbrief voor beleggingsupdates en deskundige analyses.

Asia represents a diverse set of opportunities

Beyond Japan, Taiwan and Korea, structural growth drivers differ markedly, with distinct sources of alpha beyond the AI theme currently dominating global markets. India and Southeast Asia benefit from favorable demographics, rising incomes and rapid urbanization that are powering a multi year upshift in domestic consumption and services demand. Financials, consumer companies and infrastructure linked sectors stand out as beneficiaries as banking penetration deepens, credit access broadens and governments invest in transport, energy and digital networks. India is also undergoing a significant infrastructure CapEx cycle, with large scale power transmission expansion, electrification and grid modernization underway to support industrialization and fast growing data center demand. These trends anchor India’s long duration growth potential and create a broad opportunity set across banks, utilities, industrials and technology hardware.

In ASEAN, structural themes such as financial inclusion, urbanization and the rise of digital infrastructure are prominent. Banks in Indonesia, the Philippines and Vietnam are benefiting from still low credit penetration and the formalization of financial systems. Domestic real estate and consumption driven businesses tap into rising incomes, housing demand and ongoing urban development. At the same time, the region is emerging as a manufacturing and digital infrastructure hub, attracting foreign direct investment as global companies diversify supply chains away from single country concentration.

China plus one is still happening

Despite falling out of focus given the Iran war and massive AI build-out, supply chain reconfiguration is itself still a major tailwind for Asia-Pacific. It is driving FDI into markets such as Indonesia, Vietnam,2 Malaysia and India, where companies are expanding manufacturing capacity, logistics networks and enabling infrastructure. The resulting capex cycle spans industrial automation, semiconductor equipment, transport and port infrastructure, and energy and power projects. These investments are generating multiplier effects across local economies and broadening the opportunity set for investors.

As the largest equity market in the region, China remains a polarizing component of the regional story, but the approach there also illustrates the importance of active management. After being viewed by many since Covid as uninvestable, MSCI China delivered strong performance in 2025 as sentiment stabilized and investors recognized a more selective, valuation driven opportunity set. Pro growth policy measures reduced perceived tariff risk, while resilient large cap technology earnings and evidence of domestic AI capability have all contributed to a more nuanced picture.

Active strategies have an edge

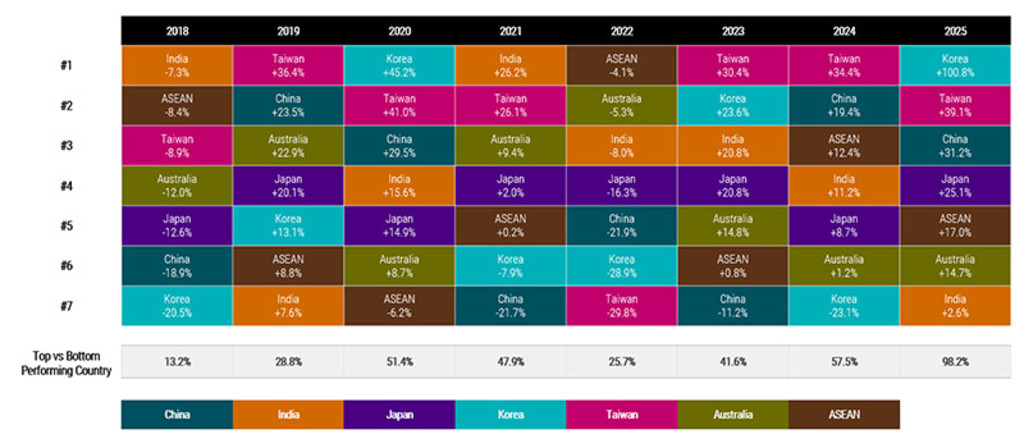

In such a diverse and heterogeneous region, we believe active management is advantageous. Asia-Pacific encompasses economies at very different stages of development, with varied growth rates, income levels, industry structures, cultures and currencies, creating a complex landscape rich in potential alpha. As Figure 2 shows, performance dispersion between countries is high and performance leadership changes fast, giving an edge to active investment strategies for the region as a whole.

Figure 2: Performance dispersion across countries is significant

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: MSCI China, MSCI India, MSCI Japan, MSCI Korea, MSCI Taiwan, MSCI Australia, and MSCI AC ASEAN factsheets. Calendar year total returns in USD.

Asia-Pacific well positioned but Middle East trade crunch remains a key risk

Asia Pacific equities continue to demonstrate resilience, underpinned by strong AI-driven earnings and attractive valuations, even amid geopolitical uncertainty and rising energy prices. However, the recent rally, largely concentrated in a narrow group of AI beneficiaries, highlights increasing concentration risk and a narrowing margin for error as higher oil prices may begin to weigh on broader demand and earnings.

While we remain constructive given compelling valuations, improving earnings momentum and the region’s diverse structural growth drivers, the current environment calls for greater discipline. Investors should remain vigilant, closely monitoring earnings delivery, managing concentration risk, and actively diversifying sources of alpha to navigate a more complex and uneven market backdrop. Given its strategic pre-eminence in key industries and the region’s structural tailwinds we believe allocation to Asia-Pacific, with its blend of developed and emerging markets, should be a core element of a global portfolio for long-term equity investors. In the shorter term, after the neutral result of the May Trump-Xi summit, any confirmed resolution to the US-Iran conflict could be the next catalyst for Asia-Pacific equities.

Footnotes

1 MSCI AC Asia Pacific Index, US Index, Europe Index factsheets to 30 April in USD.

2China’s Pivot to Vietnam Blows Hole in Trump’s Made-in-USA Plan – Bloomberg – 31 March 2026