Investment Writer

• Intervista

Quality in the lead: Positioning for high yield alpha in 2026

Our high yield portfolio managers discuss how positioning, sector selection and issuer quality are shaping their outlook for 2026.

Relatori

Jessica Monkivitch

CIO High Yield, Portfolio Manager

Portfolio Manager

Top keywords

Sommario

- High yield fundamentals remain solid, supported by growth and supportive policy

- Opportunities are emerging selectively across financials, chemicals and parts of the energy sector

- AI matters less for issuance, but increasingly shapes issuer selection and sector disruption

Despite persistent geopolitical tensions, high yield delivered steady returns in 2025,1 supported by resilient growth and stable policy conditions. Within this environment, Robeco’s high yield strategy achieved modest outperformance,2 reflecting an ‘up-in-quality’ positioning. This contributed positively amid rising dispersion between higher- and lower-quality credits, and an overweight allocation to European issuers.

Looking ahead to 2026, we remain constructive on the asset class and expect opportunities to continue to emerge in sectors such as financials, chemicals and select energy names. High yield continues to offer an attractive yield pick-up versus investment grade, while elevated dispersion between stronger and weaker issuers reinforces the importance of being selective.

In our latest quarterly Q&A, high yield portfolio managers Sander Bus (SB) and Christiaan Lever (CL) reflect on these dynamics and discuss what they mean for the year ahead.

SB: “From a top-down perspective, company fundamentals look solid. Leverage and cash flow metrics show no major problems, while fiscal policy in both the US and Europe remains very supportive, typically helping to underpin economic growth.”

“The other side of the coin is geopolitical risk. The environment remains unpredictable, yet markets seem not to care that much. Last year, spreads widened sharply in April, only to snap back very quickly. Since then, the market appears conditioned to view every spread widening as a buying opportunity.”

“Technicals have also been very strong. Last year and into the first weeks of this year, new issues have been absorbed easily. New issue premiums are low and sometimes deals even price through secondary market levels, allowing riskier names to access the market. That said, this could change. Low funding costs and high confidence may lead to increased M&A activity, which is often debt-financed and would increase supply across both high yield and investment grade markets. On top of that, large-scale CapEx related to AI and data center build-outs could add significant supply to investment grade markets, with spillover effects for high yield.”

The pickup versus investment grade remains around 200 bps in yield terms, which still makes the asset class attractive

“Against this backdrop, we are staying close to benchmark beta and remaining selective. Typically, each year brings episodes where spreads widen by 100 basis points or more. Those moments can offer better opportunities to increase risk, but it depends on the underlying cause.”

CL: “I agree. Markets tend to react briefly to headlines or tweets, especially from Trump, but those reactions fade quickly. Short periods of weakness are often immediately treated as buying opportunities. While it’s hard to predict the trigger, the market may be too optimistic right now. Strong technicals reinforce that optimism, as there is capital that still needs to be deployed.”

“Toward the end of last year, dispersion in high yield increased, with lower-quality credits such as CCCs underperforming higher-quality BBs. Given our quality bias, this dynamic contributed positively to performance. Then, as January started and returns reset, spreads compressed again as investors reached for yield, often quite indiscriminately, including in weaker names.”

SB: “Early this year, we saw some compression return, but over time, dispersion typically re-emerges.”

What are your expectations for returns this year?

CL: “Historically, when benchmark spreads start below 350 basis points, the probability of achieving positive excess returns over the year is lower. Last year was an exception, and we are starting again at similar levels. The bigger risk may be inflation reaccelerating and influencing rate policy, particularly in the US. At the same time, political pressure on central banks could keep rates lower than inflation alone would suggest, which could stimulate certain end markets such as housing and consumer finance.”

“Investment grade is also dealing with tight valuations, equities look expensive, and emerging markets are also trading at compressed levels. Against this backdrop high yield stands out as a relative source of value. In fact, we’ve seen some institutional investors increase their strategic allocations to high yield. These strong inflows provide continued support for the asset class.”

AI was a major theme in your December 2025 outlook. How does AI affect high yield specifically?

SB: “AI has less impact on the supply side of high yield than in investment grade. There are only a handful of data center-related issuers in the high yield universe. However, AI is highly relevant from a bottom-up perspective, with the potential to disrupt entire sectors. For some companies, AI is an opportunity to improve efficiency and cut costs, for others, especially in certain service or software-related areas, it poses a serious threat. In our issuer selection, we explicitly assess whether AI is an opportunity or a risk for each company. In that sense AI is very relevant for high yield, just not primarily as a source of new issuance.”

Climate Global High Yield Bonds ZH EUR

- performance ytd (30-6)

- 1,24%

- SFDR (30-6)

- Article 9

- Pagamento del dividendo (30-6)

- No

- Prezzo corrente (21-7)

- 107,36

- Inception date (30-6)

I rendimenti passati non sono indicativi dei possibili risultati futuri. Il valore degli investimenti può subire oscillazioni.Annualizzati (per periodi superiori ad un anno). Le performance si intendono al netto delle commissioni e sulla base dei prezzi delle operazioni.

Outside of AI, what specific sectors or trends are you looking at?

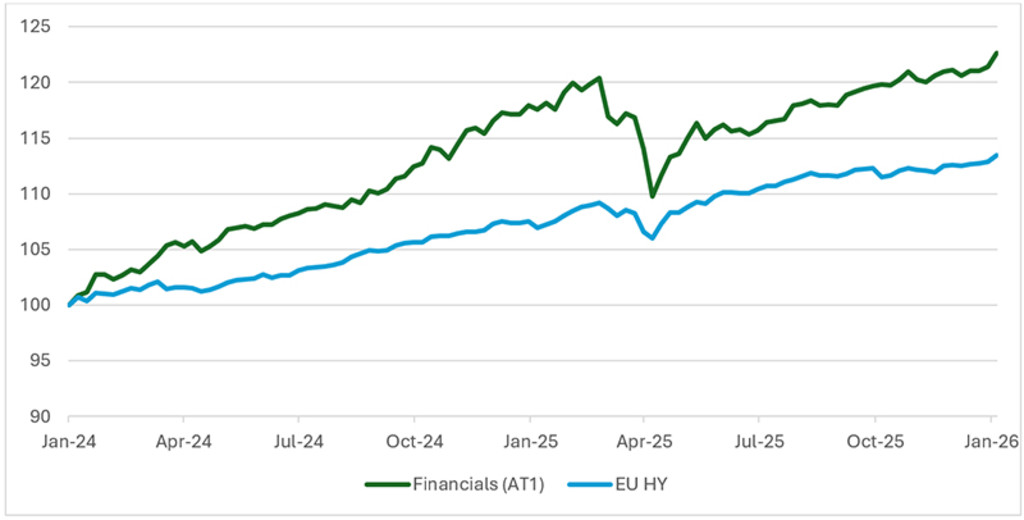

CL: “We remain positive on the financial sector, even though it is an off-benchmark position. Subordinated financials still offer attractive spreads relative to their quality, particularly compared with BB-rated high yield. We view the off-benchmark allocation as a crossover opportunity between high yield and investment grade, where relative value can be assessed across the full capital structure. Having analysts who cover both investment grade and high yield allows us to identify these opportunities.”

“Within European high yield, we see selective opportunities in sectors such as chemicals and packaging. European issuers are generally better positioned than their global peers, supported by stronger balance sheets and more conservative capital structures.”

“Pressure on these sectors has been driven by higher feedstock costs and, in some cases, increased competition from Chinese imports. These dynamics have weighed on spreads but also created attractive entry points. While the trough in this cycle has been longer than usual, it has sharpened dispersion within sectors. Against this backdrop our positioning in chemicals could benefit from potential EU tariffs or other anti-dumping measures discussed in early January.3”

“This makes issuer selection critical. Some companies are facing cyclical headwinds but retain the balance-sheet strength to navigate the environment, while others face more structural challenges. Our focus is on identifying the former and being highly selective within each sector.”

Figure 1: Financials remain a high-conviction position with compelling spreads

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: Bloomberg, Total Returns of the Bloomberg Europe CoCo Tier 1 Index vs Bloomberg Euro High Yield Index, January 2026.

What about housing-related sectors?

CL: “In the US, homebuilders themselves have continued to trade relatively tight, supported by strong land banks that underpin their balance sheets. That has limited volatility and opportunity there. However, suppliers to the housing market – such as building materials, roofing, or doors – have seen more spread widening. These companies typically have higher leverage and less asset backing, which explains the weakness. If housing activity recovers, those areas could benefit.”

SB: “That’s an area we are scrutinizing closely, particularly in the US, but always with a focus on issuer quality and balance sheet strength.”

Leggi gli ultimi approfondimenti

Iscriviti alla nostra newsletter per ricevere aggiornamenti sugli investimenti e le analisi dei nostri esperti.

Yield has been a key attraction of high yield. How does that argument look today?

SB: “Yields have come down meaningfully compared to 2022.4 Government yields are lower, and spreads have compressed. It is harder to argue that high yield is outright cheap from a yield perspective. High yield also has an internal stabilizing mechanism: when yields rise due to stronger growth, spreads often compress; when spreads widen due to economic weakness, government yields typically fall. That combination can help smooth returns over time.”

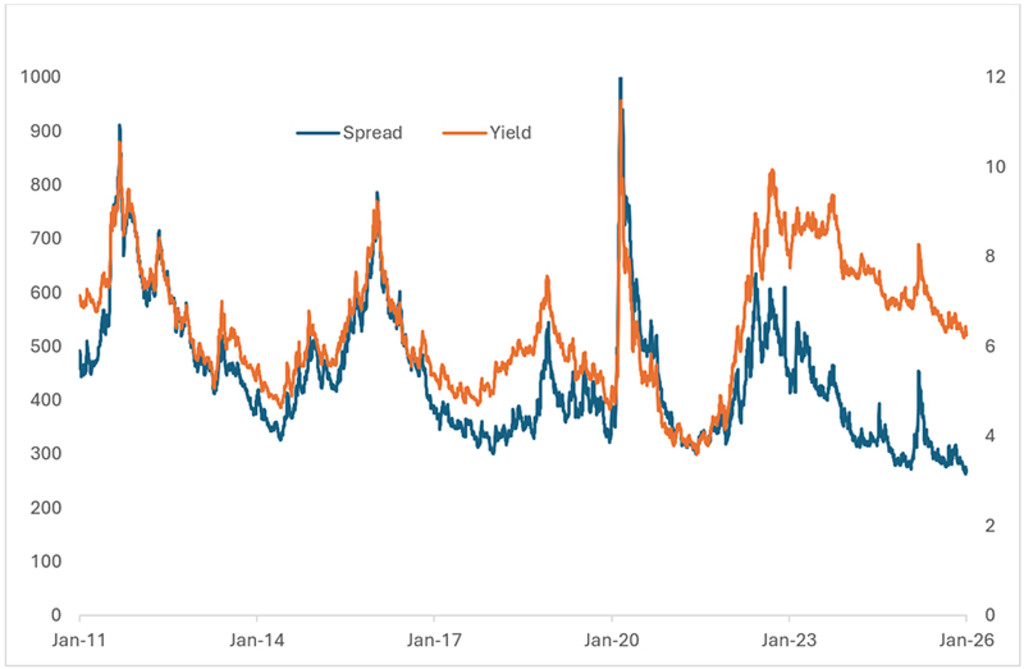

CL: “Currently, US high yield trades around the high sixes in yield-to-worst, while Europe is closer to the high fives. The pickup versus investment grade remains around 200 basis points in yield terms, which still makes the asset class attractive in a relative sense.”

Figure 2: Global high yield market conditions: spreads and yields

Past performance is no guarantee of future results. The value of the investments may fluctuate.

Source: Bloomberg Global High Yield Corporate Total Return Index Unhedged USD, January 2026

Finally, a quality tilt is a core feature of your strategy. Why does it matter in this environment?

SB: “The quality tilt is a long-term conviction for us. Historically, higher-quality bonds have outperformed lower-quality bonds not only on a risk-adjusted basis, but often also in excess return terms. Even when the broader economy looks stable, there are always winners and losers. With volatility driven by geopolitics and ongoing AI-related disruption, dispersion can increase. Our investment process focuses on avoiding the losers, as this is where much long-term outperformance is created.”

CL: “If we see a year characterized by strong fundamentals but elevated noise and tail risks, a quality-biased high yield approach can be a sweet spot. It offers attractive income with controlled downside, especially compared to equities trading at all-time highs and pockets of excess elsewhere in markets.”

Footnotes

1Past performance is no guarantee of future results. The value of the investments may fluctuate.

2The fund outperformed by 14 bps (6.08% vs. the benchmark of 5.94%).

3On January 2026, the European Union implemented significant anti-dumping measures, tariffs, and new regulations to protect its chemical industry from unfair competition, particularly from China, Russia, and other non-EU countries. See https://policy.trade.ec.europa.eu/enforcement-and-protection/trade-defence/anti-dumping-measures_en

4Past performance is no guarantee of future results. The value of the investments may fluctuate.