Head of Multi Asset & Equity Solutions, Co-Head Investment Solutions

• Monthly outlook

Energy self-sufficiency in the age of shocks

The Iran war has again raised the issue of not relying on resources from war zones, but electrification is not keeping up with geopolitical events, says multi-asset investor Colin Graham.

Authors

Summary

- Gulf conflict highlights the importance of national energy self-sufficiency

- Big regional differences in investment levels as China leads sovereignty push

- Electrification is the long-term answer to move wholly away from fossil fuels

The closure of the Strait of Hormuz led to oil and gas prices again soaring, following prior spikes during the Ukraine war and Covid pandemic. While electrification is gathering pace, and renewable energy is growing fast, the world still relies on petrol and jet fuel, along with fossil fuels used in fertilizers, plastics and clothing. It also relies on the critical minerals needed for electrification.

“The energy landscape is being reshaped by recurring shocks – geopolitical disruption, volatile fuel prices, and accelerating electrification demand from transport, buildings and data infrastructure,” says Graham, Head of Robeco’s Multi-Asset Solutions team.

“This environment has precipitated a fundamental reconsideration of what energy self-sufficiency looks like in a modern, interconnected economy. Historically, energy security was defined by access to physical reserves of oil and gas. Today, this has morphed into the ability to generate, store and manage power using domestic infrastructure, sources and technology.”

“As a consequence, energy security through electrification also relies on a wider range of critical minerals, which are not always in the most accessible locations, geographically or politically.”

“Wind and solar power require rare earth metals, while electric vehicles need lithium and cobalt for their batteries, and grid capacity expansion relies on copper cables. Self-sufficiency encompasses much broader requirements than just fossil fuels.”

Smart Energy I GBP

- performance ytd (30-6)

- 53.16%

- Performance 3y (30-6)

- 26.61%

- morningstar (30-6)

- SFDR (30-6)

- Article 9

- Dividend Paying (30-6)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

Achieving such self-reliance is now a priority in the world’s three main economic powerhouses – China, the EU and the US – but is taking place at differing paces, as shown in Table 1.

In 2025, China invested USD 800 billion in domestic renewable energy, including building a solar farm the size of Paris. In the past five years, its total outlay exceeded USD 3 trillion. For the EU and US, the money invested has been only about half that.

Table 1: Investments in renewables and energy sovereignty (in USD billions)

Sources: BloombergNEF Energy Transition Investment Trends (2024/2025), IEA World Energy Investment Reports, and the Clean Investment Monitor, May 2026.

“China’s approach to energy sovereignty is closely linked to industrial capacity in the electrification value chain,” Graham says. “Beyond rapid renewable deployment, China’s strategic edge comes from control over manufacturing ecosystems and the ability to scale grid equipment, such as the development of high voltage transmission, power management components and energy storage.”

“The scale and speed of this transformation has been aided by the availability of critical minerals, with a deliberate policy of vertical integration of supply chains and refining. However, China is still reliant on importing raw materials such as cobalt (95%), nickel (90%) and iron ore (80%).”

“These processes have built domestic resilience while exporting critical components to the EU and US, and while remaining embedded in global supply chains.”

All hail shale in the US

The US has moved more toward developing its own fossil fuels while also developing clean energy technology. “In the late 2000s, the US implemented a deliberate industrial policy to increase its energy self-sufficiency, leading to the boom in extracting shale oil and gas,” Graham says.

“Subsequently, US policy has increasingly targeted the electrification stack: domestic manufacturing of clean-energy components, grid modernization and supply chain resilience for storage and power electronics.”

“However, much of the critical minerals required are predominately imported from China, including refined rare earths, manganese and natural graphite, and so US policy has focused on domestically producing and mining these minerals themselves.”

“With the advent of energy-hungry data centers to keep the US ahead in the AI race, mineral and energy self-sufficiency is increasingly essential.”

Mixed bag in the EU

Meanwhile, the EU presents a mixed bag of opportunities, partly due to aversion to further developing fossil fuels, and scaling back nuclear power. “While the EU can claim that its energy efficiency has increased much more than the US and China, the economy remains stuck in the middle, and its investment levels reflect that position,” Graham says.

“This is a result of not developing shale resources due to bureaucratic headwinds, but instead building an economy reliant on imported gas that was once cheap, rather than providing capital for renewable technologies, and creating a eurozone-wide grid.”

In 2024, just under 50% of electricity production in the EU came from renewable sources, though much of the equipment needed for it was manufactured abroad; 90% of solar panels are sourced from China.

‘Dangerously dependent’

“The EU remains dangerously dependent on China for raw and refined critical minerals, with the lion’s share of rare earths, magnesium, cobalt and lithium being imported from the Peoples’ Republic,” Graham warns.

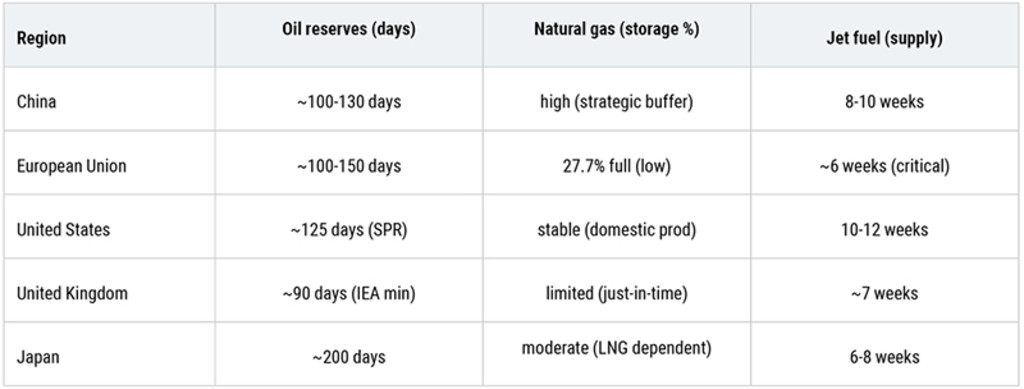

“In essence though, the EU economy is more resilient to energy shocks, but is more vulnerable to natural gas shortages and refined oil products.” This is shown in Table 2, where the EU’s capacity to store natural gas is low, while its vulnerability to jet fuel shortages is high.

Table 2: Levels of reserves for oil, natural gas and jet fuel

Source: International Energy Agency, April 2026.

Decarbonization can help

Graham says the longer-term answer lies in becoming more energy-efficient to require less power, be that from electricity or fossil fuels.

“Demand-side efficiency is one of the most direct sources of energy self-sufficiency, and we can highlight that electrification technologies such as EVs and heat pumps can be roughly two to four times more energy-efficient than their fossil alternatives in end-use terms,” he says.

“For energy-importing economies, this efficiency gain matters strategically: reducing the quantity of primary energy required increases economies’ resilience to imported energy shocks.”

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Transition is no longer optional

“In all, the shocks of recent years reinforce a central conclusion that economies need to reduce reliance on external energy and critical mineral sources,” Graham says.

“The energy transition is no longer an optional environmental project but a system redesign that affects national security, affordability and competitiveness,” he says.

“As electrification accelerates, the binding constraints shift toward grids, power management, storage and efficiency – areas that are both strategically sensitive and capital intensive. This is perhaps the biggest investment opportunity of our times; you don’t need the Strait of Hormuz if your own economy’s demand for energy and minerals is self-sourced.”