Head of Multi Asset & Equity Solutions, Co-Head Investment Solutions

• Monthly outlook

Private credit: The good, the bad, and the illiquid

It’s a USD 2.1 trillion market that sits quietly behind the scenes. Private credit by non-bank lenders has been a reliable source of higher yield when rates were low – but this giant asset class may now be poised to unsettle investors.

概括

- Private credit market is largely sub-investment grade, non-bank loans

- Higher inflation implies higher rates, threatening stability and refinancing

- A market that has been ‘good’ may become partly ‘bad’ and then possibly ‘illiquid’

The potential for higher interest rates amid geopolitical instability risks turning this largely sub-investment grade market into the kind of Wild West last seen with the Great Financial Crisis (GFC) and the sub-prime debacle that lay behind it, says multi-asset investor Colin Graham.

“Private credit encompasses direct and middle market lending, where the capital is provided by non-bank lenders, and therefore it does not appear on bank balance sheets which were more heavily regulated after the 2008 Great Financial Crisis,” says Graham, Head of Robeco Investment Solutions’ Multi-Asset team.

“The business of lending outside of banks’ balance sheets grew after the GFC and the subsequent US Dodd-Frank act to protect banks’ depositors. The issue for investors is – does the USD 2.1 trillion private credit market now pose a threat, as interest rates have risen, and geopolitical concerns such as the Iran conflict threaten financial stability?”

The majority of private credit loans are sub-investment grade, due to its bespoke nature of lending to companies with lower credit ratings and less ability to access public debt markets, giving them a channel to borrow money.

“This provides lenders and investors with higher yields and lower volatility (a better Sharpe ratio),” Graham says.

“The downside for private credit investors is that valuations can be opaque, and during financial or economic shocks, the diversification benefits evaporate, as the correlation with mainstream credit markets reverts to one. The primary concern is then on the return of capital rather than return on capital, trying to avoid defaults at all costs.”

“The credit markets were rock solid in 2025, but toward the end of the year, a divergence between listed (public) and unlisted (private) markets began to show. While public investment grade markets remain resilient, the USD 2.1 trillion private credit market began to undergo a structural stress test.”

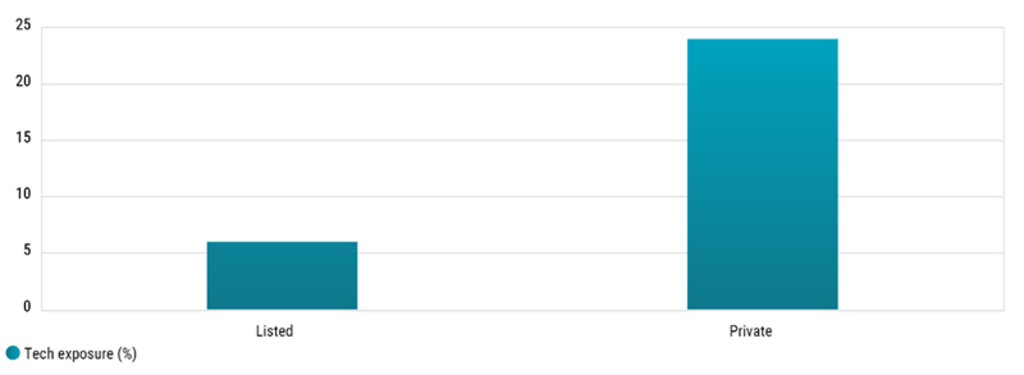

Higher Tech exposure

One issue is that private credit has a much higher exposure to the tech sector – which is vulnerable to AI disruption – than public debt. While private credit does not price as regularly as listed credit or equity, the significant commonality in exposure to tech means the benefits of lower volatility can disperse.

Figure 1: Tech exposures of the global public and private credit markets

Source: Absolute Strategy Research, April 2026

“Now this giant market is running into headwinds,” Graham warns. “The confluence of a higher rate environment, the geopolitical shock of the Gulf conflict and tariffs, and AI-driven business model disruption in software has created a period of additional scrutiny.”

“We believe headline default rates (currently at about 2.1%) are a lagging indicator. When adjusted for liability management exercises (LMEs) and ‘shadow distress’, the ‘true’ rate approaches 5.4%.”

“In this environment, the performance divergence between hard assets, low obsolescence (HALO) businesses anchored in physical infrastructure and the highly leveraged, AI-exposed software portfolios becomes obvious.”

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Inflation = higher rates

And now, the outbreak of the war in Iran has caused another oil price shock and supply chain disruptions, bringing the inevitable inflationary pressures last seen during the Covid pandemic. Higher inflation will make it more likely that interest rates will rise to counter it, posing a direct threat to highly leveraged businesses.

“Our 2026 core investment scenario outlined a positive macro backdrop, though the downside scenario probability has since risen due to Gulf supply chain impediments,” Graham says. “The headwinds have been growing, with significant implications for corporate borrowers and private credit investors.”

“Firstly, the escalation of conflict in the Middle East has closed the Strait of Hormuz, with the potential for a global supply shock not seen since the Covid lockdowns. Secondly, interest rates expectations have flipped from cuts to hikes, as inflationary pressures are anticipated to rise. Finally, AI is touted as a business-model destroyer in industries such as software and IT services, complicating the ‘exit’ pricing for businesses.”

Haven’t we been here before?

So, are we looking at a repeat of the GFC, when defaults on sub-investment grade loans almost brought down the banking system? “The growth of private credit has been driven by loose monetary policy (leverage) and investors’ search for yield, which meant demand drove the supply and lowered credit standards,” Graham says.

“The US SEC noted in 2024 that ‘advisers have a conflict of interest with private funds and their investors when they value the funds’ assets and use those valuations as a basis for the calculation of the adviser’s fees and fund performance.”

“This is reminiscent of the compensation structure for mortgage appraisers and rating agencies for collateralized loan obligations (CLOs) before the GFC exposed the dangers of this business model.”

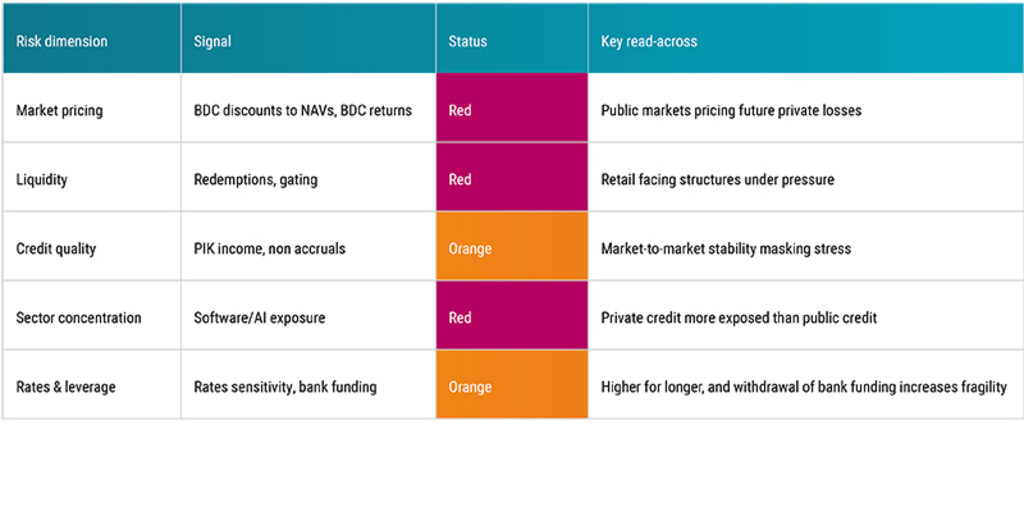

Figure 2: The risk dimensions of the private credit market

Source: Robeco, April 2026

A Mexican standoff…

The real test of stability will come over the next 18 months, when nearly USD 480 billion in private debt matures and sponsors, investors and borrowers decide who is on the hook for either repayment or refinancing.

“Much of this private credit was originated at the start of the decade at valuations and low interest rates that no longer exist,” Graham says. “Without a robust IPO or M&A market, these ‘capital gaps’ must be filled by aggressive equity injections from sponsors or debt-for-equity swaps that will redefine the recovery landscape.”

“While the banking system may be shielded, there are other larger financial sector holders of private credit, such as life insurers, who may be more vulnerable to the write-downs.”

…or a smoking gun?

“The private credit market is not facing an imminent collapse, but rather a maturing and more fragile part of the cycle. The new cohorts of private credit investors should be able to avoid the headwinds discussed, as interest rates have normalized and the economy is in turmoil, so lenders will be less likely to overpay for a business. Existing debt holders may have a rockier ride.”

“Looking forward, institutional investors with longer time horizons should avoid the gating issues, while benefiting from an illiquidity premium and opportunities that arise from the forced liquidations, restructuring and refinancing.”

“We expect that 2026 and 2027 will become the years where performance is generated through restructuring expertise and rigorous manager selection by sponsors with deep pockets, at expense of the retails and minority lenders. We continue to monitor the outlook for private credit.”