Head of SI Thought Leadership and Climate & Biodiversity Strategist

• Insight

Investors prefer active equities and green bonds for climate transition

Growing demand for climate investments are being led by a preference for transition-focused equities and green bonds, along with thematic strategies.

Authors

Top keywords

Summary

- Preference for investing in active equity strategies and green bonds

- Seven in 10 investors are committing to net zero, or are looking into it

- Stable interest in Europe but backlash against ESG in North America

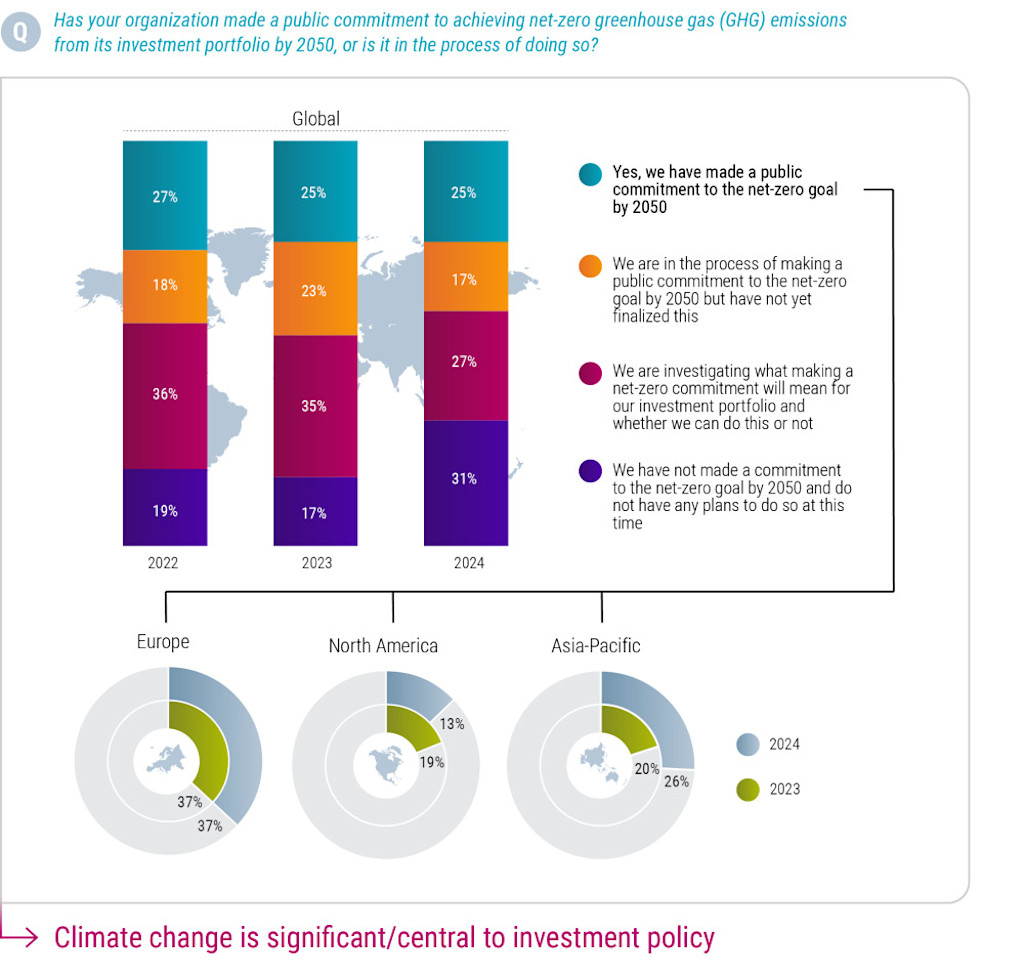

Seven out of 10 investors are either making a firm commitment to achieving net zero in portfolios by 2050, are in the process of doing so, or are investigating how it could work out for them, the Robeco Global Climate Investing 2024 survey shows.

Allocations to low-carbon and climate solutions strategies are widespread, with two-thirds (66%) of all investors saying they already allocate to investment funds with a low-carbon approach, or are planning to do so in the next one to two years. Some 63% also said they were allocating to funds that invest in climate solutions (such as decarbonization funds) of varying kinds.

And transition investing is gaining a higher focus among investors, as they focus on companies such as those in renewable energy that are leading the march towards net zero emissions, to try to meet the Paris Agreement targets to tackle global warming. Some 37% are currently allocating to strategies specifically targeting companies with credible transition plans, while 63% plan to do so within the next one to two years.

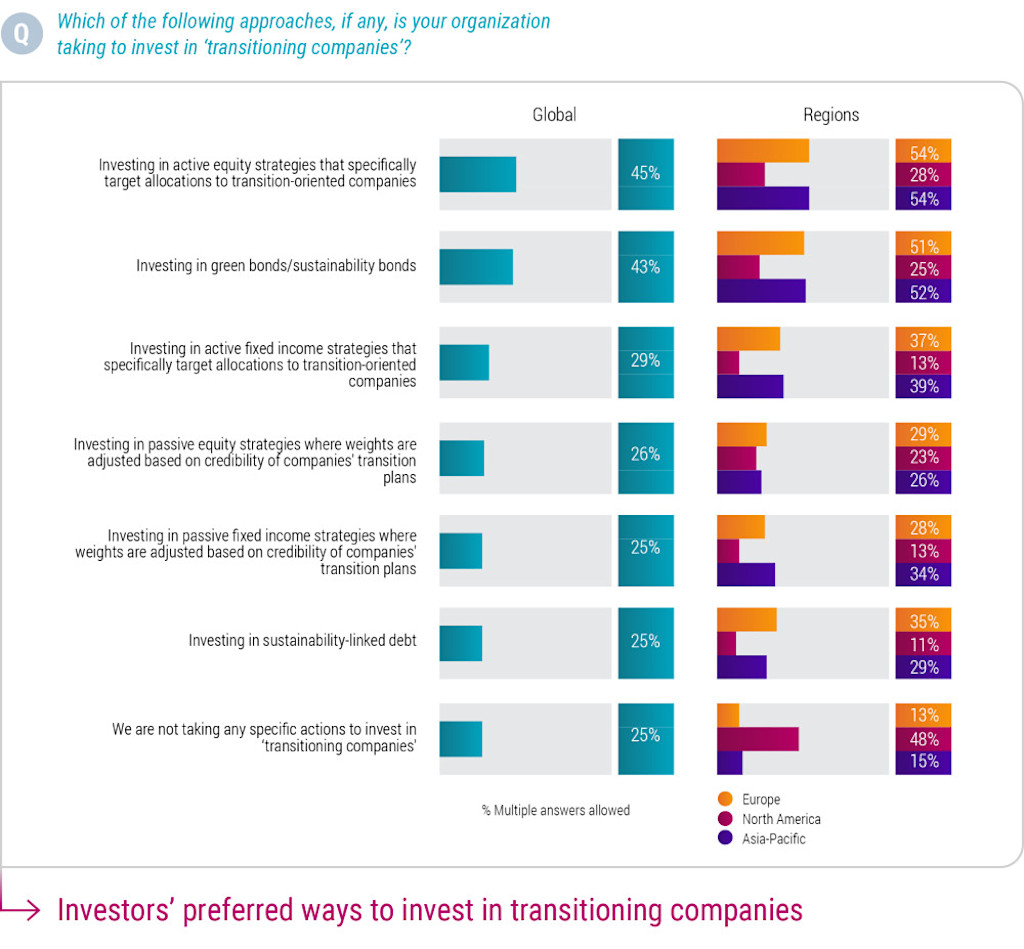

The transition issue has a bearing on the investment styles preferred. Some 45% globally are using active equity strategies that specifically target allocations to transition-oriented companies, while 43% are investing in green bonds or sustainability-focused bonds. This approach is again more popular in Europe and APAC (54% each) than in North America, where almost half of investors (48%) are not taking specific actions to target transitioning companies.

Part of the reason for this is because active strategies can enable more rigorous assessment of companies’ transition plans, while green bonds offer ring-fencing for the use of the proceeds. These approaches can help counter the key challenges facing the financing of transitioning companies: inconsistent disclosures on transition plans by companies (a headwind cited by 43% of investors) and inadequate guidelines from regulators around what actually constitutes ‘transition activities’ (36%).

Source (for all charts): Robeco Global Climate Investing Survey 2024.

Opportunities in transition

“This year’s survey highlights the focus on investment in climate solutions and in transitioning companies,” says Lucian Peppelenbos, Climate and Biodiversity Strategist at Robeco. “Both topics are fundamental for investors making a net-zero commitment. Investors can see great opportunities in climate solutions, so it is not surprising to see many poised to increase their allocations in this area.”

“And the transition among corporates and others from brown to green, as they decarbonize, cannot take place without the active involvement of investors, rewarding those making the change and withdrawing support from the unwilling or reluctant.”

“One interesting facet of this year’s findings is how investors in the Asia-Pacific (APAC) region are now forging ahead on sustainability, as they increase their support for the climate transition.” The number of APAC investors making a public commitment to net zero rose from 20% to 26% as the region moved ahead of Europe in making climate change central to policy for the first time.

Stay informed on Climate investing

Stable net zero commitments

The number of investors with firm public commitments to net zero has remained stable at 25% compared to last year’s survey, while those in the process of doing so dropped slightly to 17%. Those investigating whether it was feasible also fell to 27%, and those saying they have no plans to do so has almost doubled since 2023 to 31%.

Globally, the results were adversely affected by a fall-off in interest in North America, where a backlash in ESG investing generally has put climate change on the back burner for many. Regionally, the outlook is more positive in Europe, where those making a firm commitment is stable at 37%, and in Asia-Pacific, where the figure rose from 20% in 2023 to 26% today.

Insurance companies stand out for making a net-zero commitment compared to other institutional and wholesale investors, perhaps driven by their unique exposure to climate change from both sides of the balance sheet. Some 39% of insurers have made a public commitment, and another 20% are in the process of doing so.

A focused and diligent approach

“Climate investing is starting to mature” Peppelenbos says. “When we look at the survey findings, we can see that many investors are adopting a focused and diligent approach to the work of decarbonizing investment portfolios and moving toward the low-carbon economy of the future.”

“As investors get to grips with the hard work involved in the climate transition, there is less naivety, and more careful deliberation and scrutiny over what is needed to embed sustainability into the many aspects of running investment portfolios.”

“This ranges from gaining expertise and experience in measuring their carbon footprint, to understanding forward-looking metrics and data, to ensuring it is fully integrated into strategic planning and investment in different asset classes when working with external organizations.”

A roadmap for decarbonizing

But it’s still a long road to achieving net zero. While a majority of investors have set policies for how they will decarbonize some segments of their equity (62%), fixed income (53%), and real estate (51%) portfolios, very few have a clear roadmap for decarbonizing all segments of them.

As they do decarbonize more concentrated portfolio segments, such as domestic equities, bigger deviations from the benchmark may be required, compared with international equities, for example, where the overall universe is much larger.

There remain some good reasons why investors are not decarbonizing on the scale necessary to achieve net zero, though the headwinds are declining in strength. The number of investors citing a lack of suitable investment data, research and ratings has fallen from 52% to 42% last year. Those citing a lack of clear reporting standards and disclosures also dropped from 46% to 39%. The fear of being seen to be greenwashing fell slightly from 36% to 34%.

Download the Global Climate Survey report here