The Investment Engineers

• Insight

Emerging markets: opportunities beyond the US

Over the past 12 months, a shift has begun to take shape among large asset allocators, with exposure to emerging markets assets seen as increasingly attractive for long-term investors.

Authors

Robeco

Summary

- Emerging markets are central to global growth

- EM equities remain at a discount to global markets

- EM bond yields are attractive given robust macro backdrop

After more than a decade of US equity outperformance, investor flows are gradually rotating toward a broader opportunity set. This is not driven by a loss of confidence in the US, but the increasing attractiveness of opportunities elsewhere. Valuation gaps, rising concentration risk, and uncertainty around the sustainability of current market leadership are prompting investors to look beyond a narrow set of dominant stocks.

Global markets are becoming more diverse in their drivers of returns, with differences in policy, economic structure and sector composition creating a wider dispersion of outcomes. In this environment, where leadership is less predictable and more fragmented, alongside questions around how AI investment will be funded and how it will reshape industries, accessing a broader universe is becoming increasingly important.

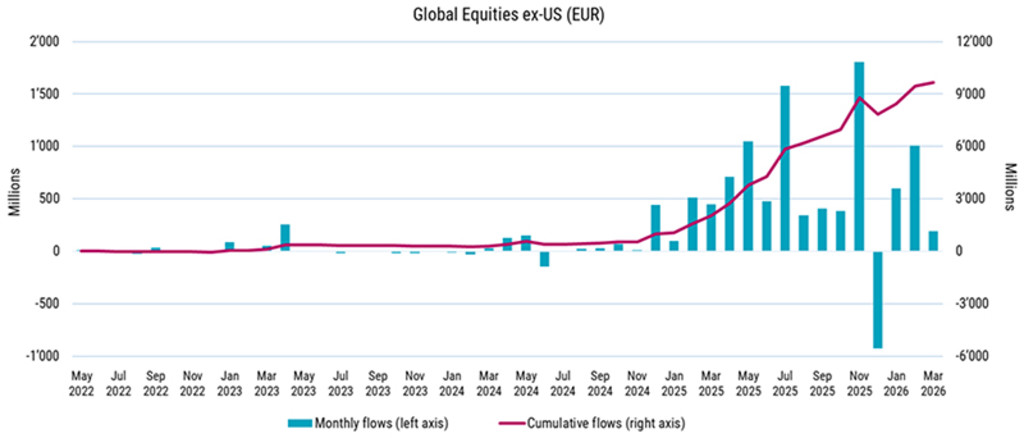

Figure 1 – Equity flows are moving out of the US and across the globe

Source: Broadridge, Robeco, May 2026.

Moreover, the growing dominance of US asset managers means a significant share of global capital allocation is increasingly influenced by US-based institutions. This can reinforce home bias and crowding, leaving opportunities in other regions underexplored.1 At the same time, the architecture of the global economy is changing with emerging markets becoming central to global growth, innovation and wealth creation. Here we spotlight just a few of Robeco’s emerging market strategies which are capturing these seismic shifts on the global landscape.

Robeco Emerging Markets Equities strategy

For investors seeking to diversify beyond the US, emerging markets offer a broad set of growth drivers at a significant valuation discount. In many cases, investors in equities are being paid EM type risk premiums for balance sheets and cash flow profiles that increasingly resemble those of developed markets. Robeco’s Emerging Markets Equities team believes emerging economies offer superior long-term investment opportunities compared to developed peers.

Figure 2 – EM Equities have historically enjoyed long periods of outperformance

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: MSCI. All figures in EUR. Data end of December 2025. The ratio in the chart above divides the MSCI Emerging Markets Price Index by the MSCI World Price Index in USD. When the ratio rises, emerging markets outperform developed markets - and when it falls, developed markets outperform emerging markets. If the currency in which the past performance is displayed differs from the currency of the country in which you reside, then you should be aware that due to exchange rate fluctuations the performance shown may increase or decrease if converted into your local currency. Performance since inception is as of the first full month. Periods shorter than one year are not annualized. Returns gross of fees, based on gross asset value. Values and returns indicated here are before cost; the performance data does not take account of the commissions and costs incurred on the issue and redemption of units. These have a negative effect on the returns shown.

We offer a comprehensive range of emerging markets equities solutions including the high-conviction Emerging Stars Equities strategy, country-specific strategies and an ex-China strategy.

Robeco’s fundamental EM team focuses on selective stock picking and deep local insight to uncover long-term opportunities across this complex universe. Our disciplined investment process starts with top-down country selection and targets what we call ‘value with a future’. It enables us to harness the inefficiencies resulting from market biases in emerging markets where investors are prone to overpaying for perceived high-quality growth. Our fundamental stock selection analysis focuses on attractively valued companies with an underappreciated earnings outlook. We overlay our fundamental analysis with a quantitative model as a tool to exploit the behavioral biases of market participants such as overconfidence and herd behavior.

Robeco Emerging Markets Quant Equities strategy

For quantitative investors, we see factor premiums in EM tend to be strong and persistent and this has underpinned our long-term investment in quantitative EM strategies. This is especially the case using our proprietary definitions, making EM a fertile ground for our disciplined, risk-managed quant strategies. Our range of strategies includes QI EM 3D Active Equities strategy, QI EM Conservative Equities strategy, and our new 3D Emerging Markets ETF.

EM markets tend to be less correlated with one another, offering natural diversification benefits across regions. While developed markets often move in sync, EM economies like India, Brazil, and Taiwan each respond to distinct local dynamics. Our quant strategies thrive on this dispersion, applying many small, deliberate tilts rather than large macro bets, creating opportunities for relative outperformance and cushioning volatility.

EM markets tend to be less correlated with one another… and our quant strategies thrive on this dispersion

All portfolios are carefully managed for risk, are regionally diversified, and use data-driven insights including machine learning and natural language processing tools. This enables dynamic and cost-efficient exposure to EM alpha.

Our 3D strategies integrate sustainability alongside risk and return using a proprietary framework. Portfolios dynamically seek the best trade-offs between these dimensions based on real-time conditions and set targets. This enhances long-term potential by managing ESG risks while capturing opportunities in companies driving the transition to a more sustainable future, without locking in a fixed sustainability outcome.

Robeco Emerging Markets Debt strategy

Emerging markets are evolving into more resilient, competitive economies, shaped by financial inclusion, rising domestic wealth, and stronger intra-EM trade. Higher trend economic growth means the creditworthiness of many emerging markets2 is converging on the levels enjoyed by developed countries, while yields often remain higher, making EM bonds a compelling opportunity for investors seeking diversification.

The creditworthiness of many emerging markets is converging on the levels enjoyed by developed countries

Robeco combines a high-conviction, active investment style with in-depth, proprietary research that balances top-down macro insights with bottom-up sovereign and currency selection with both hard and local currency products. Sustainability and transition risks are fully integrated into the framework to mitigate downside risk and enhance resilience.

Top-down positioning sets the portfolio’s risk allocation across market cycles. We analyze global financial and risk conditions next to valuation and technical factors specific to EM hard currency and EM local currency debt.

This is complemented by bottom-up issuer and country selection, which assesses sovereign creditworthiness trends using our proprietary Sovereign Ratings Model, driven by both quantitative and qualitative inputs. The model evaluates key indicators of liquidity and solvency, helping us anticipate improvements or deteriorations in credit quality and in extreme cases, identify signs of severe distress or potential default.

Conclusion

Shifting part of an asset allocation from the US to emerging markets is about recognizing how the global opportunity set has evolved. EM offers a combination of higher structural growth, improved policy frameworks, attractive valuations and underowned status that is difficult to replicate elsewhere. At the same time, the risks are better understood and more appropriately priced than in past cycles, and can be managed through diversified, research-driven approaches. For long-term investors prepared to look beyond the recent past, rebalancing from the US into emerging markets is a pragmatic step toward a more forward-looking portfolio.

Footnotes

1Schoenmaker, D. (2026) Risks for Europe of US dominance of global asset management, Policy Brief 07/2026, Bruegel.

2Emerging markets face Iran shocks with more debt, and less danger – Financial Times – 15 May 2026

Is it time to diversify beyond the US?

This article is part of a three-part investment series aimed at exploring regional alternatives to US-centric growth.

QI Emerging Markets 3D Active Equities D EUR

- performance ytd (30-6)

- 36.28%

- Performance 3y (30-6)

- 26.25%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Dividend Paying (30-6)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

QI Emerging Markets Active Equities D EUR

- performance ytd (30-6)

- 33.29%

- Performance 3y (30-6)

- 25.19%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Dividend Paying (30-6)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

QI Emerging Markets Enhanced Index Equities D EUR

- performance ytd (30-6)

- 29.67%

- Performance 3y (30-6)

- 24.73%

- morningstar (30-6)

- SFDR (30-6)

- Article 8

- Dividend Paying (30-6)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

Emerging Markets Bonds FH EUR

- performance ytd (30-6)

- 4.01%

- SFDR (30-6)

- Article 8

- Dividend Paying (30-6)

- No

- Current Price (24-7)

- 111.22

- Inception date (30-6)

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.