Strategist

Discover emerging opportunities

For investors focused on long-term investing with real diversification, EM exposure is critical.

It’s the world’s largest currency that underpins much of the world’s trade, and its recent demise has been great for markets outside the US. The dollar’s recent comeback has had many investors thinking it’s the Achilles’ heel for emerging markets and commodities, and the rally may have legs, says strategist Peter van der Welle.

A declining dollar is great for non-US stock markets, as seen in the renaissance of European and Asian equities during 2025. And since commodities are sold in dollars, any nation selling anything from oil to soybeans gets a bigger payday in its local currency if the greenback falls in value.

“Since the start of the US military action against Iran on 28 February, we have seen the dollar stage a comeback, up 1.5% as of 5 March,” says Van der Welle, strategist with Robeco Investment Solutions and its multi-asset portfolios.

“Does this dollar bounce have legs? The answer to this is critical, as correlations show that a sustained reversal in the trajectory of the greenback could challenge continued outperformance of non-US markets and a broad segment of the multi-asset universe.”

The world’s most traded currency is still overvalued by 12% on our favorite valuation metric.

“The world’s most traded currency is still overvalued by 12% on our favorite valuation metric, its deviation from trend in relative purchasing power parity (PPP). While we believe the dollar remains in a secular bear market (which it entered in 2022), countertrend rallies are common.”

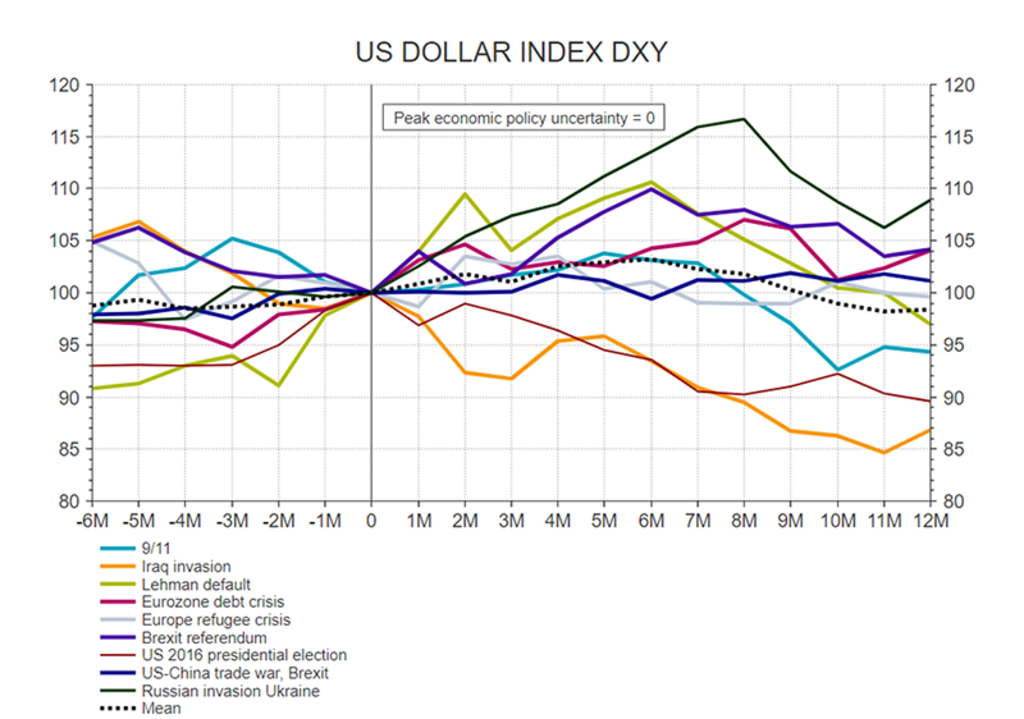

Van der Welle says that three such countertrend rallies have occurred in previous dollar bear markets, where the greenback rose at least 5% versus other currencies for an average of three months, returning an average 8.2% each time.

For investors focused on long-term investing with real diversification, EM exposure is critical.

He says the military action against Iran could set the stage for another countertrend rally, which would upend the ‘everywhere rallies’ seen in Europe, Asia and in commodities.

“First, positioning and flow dynamics favor a dollar bounce against the backdrop of elevated tensions in the Middle East,” he says. “Asset managers went into the conflict with a historically large underweight position in the dollar; the flip side of this is that they had historically overweight positions in emerging market equities.”

“This makes investors more vulnerable to be on the wrong side of the trade. The longer Middle East tensions last, the larger the scramble for liquidity becomes, favoring the dollar, as it is involved in 89% of global FX transactions. We find that the trade-weighted dollar tends to strengthen in the 3-6-month window after big geopolitical events.”

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: LSEG Datastream, Robeco, March 2026.

“Second, as bombs flew over Iran in a show of US hegemony, the dollar turned positive. Its positive correlation with the VIX volatility index, which was notably absent in the immediate aftermath of President Trump’s so-called ‘Liberation Day’ last year, returned. As such, the dollar is dusting off some of its lost appeal as a safe haven.”

The third reason is more technical as it relates to interest rate differentials against the euro, the world’s second-largest traded currency. Currently the US base rate set by the Fed is 3.5%-3.75%, with the likelihood of further rate cuts in 2026, while the ECB rate is 2.15%-2.40%, and is not seen falling further. This favors inflows into the dollar, particularly if the Middle East war raises energy prices, and therefore inflation, making the ECB even less likely to cut rates.

“On our metric, the dollar is around 3 cents too cheap versus the euro when looking at two-year rate differentials between the US and the Eurozone,” Van der Welle says. “Also, risks to an ongoing expansion of the Eurozone (to the former Yugoslav states) have become more skewed to the downside in the wake of the Iran war. A recognition of the ECB’s unwillingness to hike could therefore contribute to dollar strength.”

Subscribe to our newsletter for investment updates and expert analysis.

With Europe being more susceptible to an oil price shock, growth differentials could further favor the dollar.

Then there are GDP growth differentials between the US and Eurozone. “The dollar has recently significantly undershot the difference between US and German industrial production data,” Van der Welle says. “With Europe being more susceptible to an oil price shock, as it is a net importer whereas the US is a net energy exporter, growth differentials could further favor the dollar.”

And finally, there is good old-fashioned political motivation, with the midterm Congressional elections due in November – polls which are always seen as a referendum on the incumbent president’s popularity.

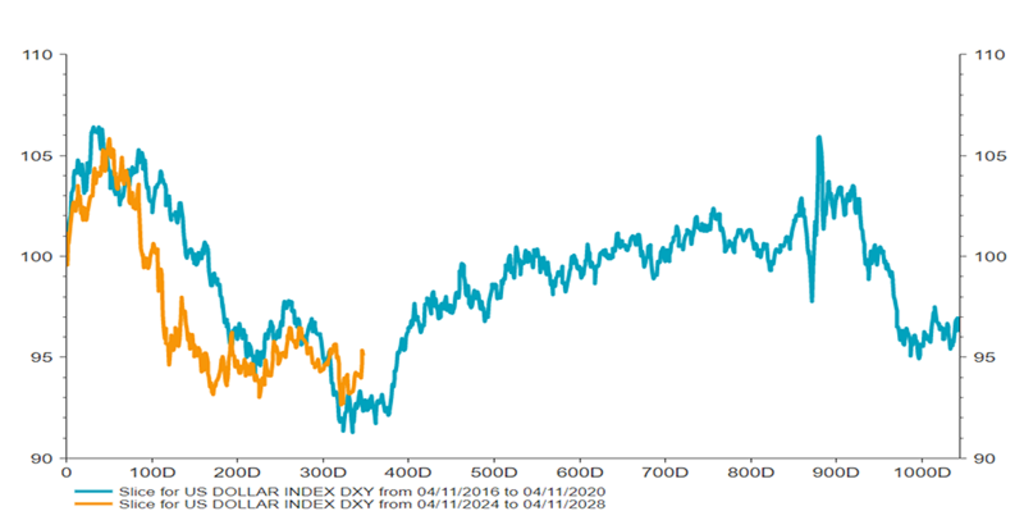

“During the second Trump presidency, we have so far seen a remarkable alignment of the dollar with its evolution during the first from 2017-2021,” Van der Welle says. “If the future were to rhyme again with the playbook of the first Trump administration from here onwards, we could be very close to a strengthening dollar, as seen in the chart below.

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: LSEG Datastream, Robeco, March 2026

“A temporarily stronger dollar could be welcomed as the November midterm elections draw closer. A stronger dollar – while exerting a tightening effect on US export growth – would lower import inflation and therefore potentially mitigate the affordability crisis through real disposable income growth, appeasing part of the Republican electorate.”

So, can it last? “While we think that turmoil in the Middle East as things stand will not derail the prospect of a synchronized global cyclical upswing, the risks to our base case of the Synchronized Shift that we predicted in our 2026 outlook have become more asymmetrical,” Van der Welle says.

“We expect the market to become more perceptive to the asymmetries surrounding the dollar. If the Iran war has indeed kickstarted a temporary revival of the dollar, we have only digested some 20% of a typical countertrend rally. More may be yet to come.”